Can Broadcom (AVGO) Ever Reach the Status of Nvidia (NVDA)

The Two AI Champions

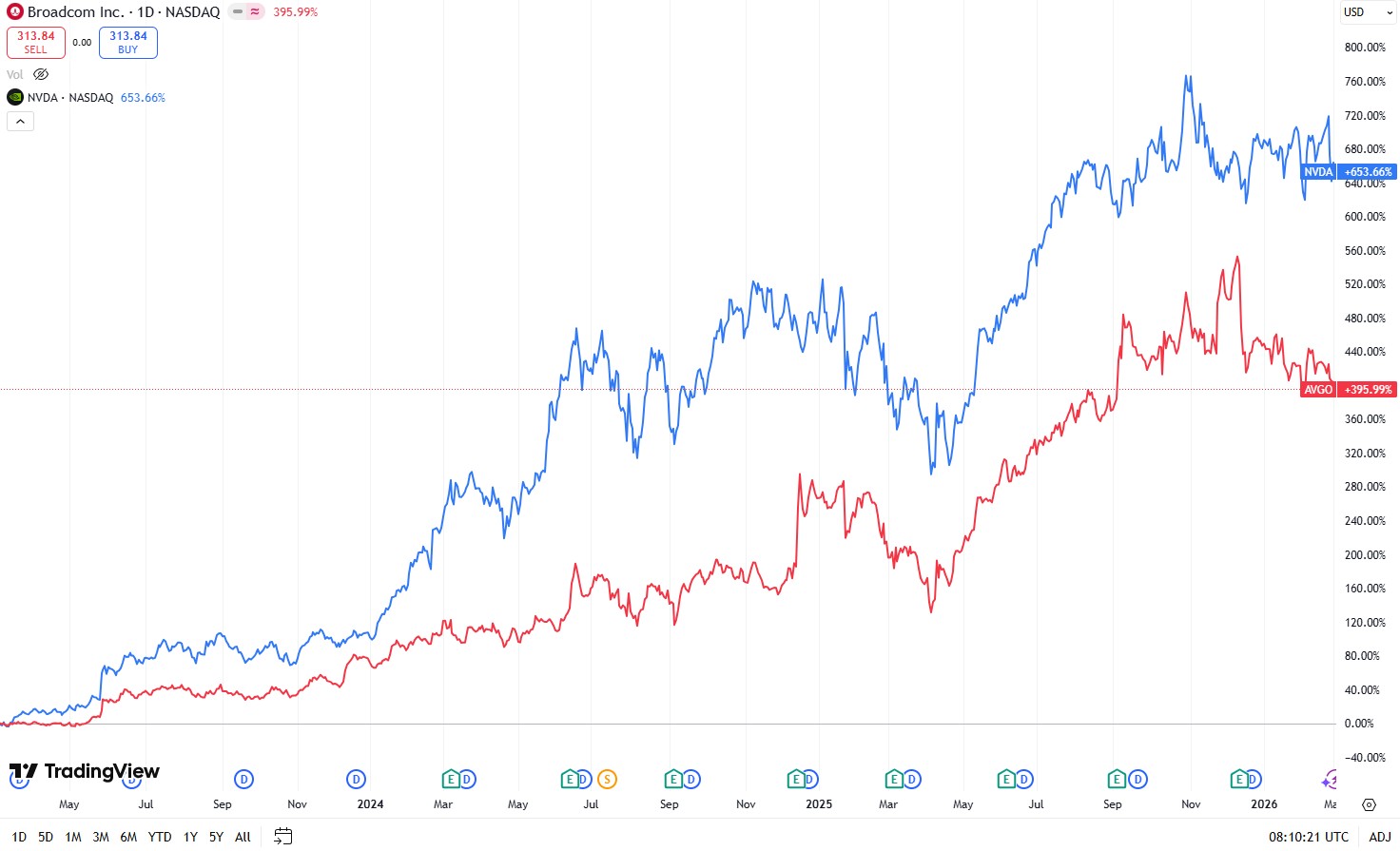

Broadcom (AVGO) and Nvidia (NVDA) frequently draw comparisons from investors due to their prominent roles in the artificial intelligence boom. This, of course, it is reflected in their stock prices, both returning hefty returns since the beginning of the AI boom in 2023.

Source: TradingView

Both companies derive substantial growth from AI-related demand, with Nvidia's GPUs serving as the cornerstone for AI training and inference computations, while Broadcom supplies custom application-specific integrated circuits (ASICs) for hyperscalers' in-house chip designs and high-performance networking equipment essential to AI data centers.

They exhibit apparent similarities in market dominance, customer bases, supply chains, business models combining hardware with software moats, and exceptionally high gross margins.

Nvidia commands over 90% of the GPU market, while Broadcom holds leading positions in custom ASICs (around 60% or more), AI data center connectivity (over 80%), and virtualization through VMware (approximately 75% market share).

In terms of supply chains, their customer lists overlap significantly, including major players such as Google, Meta, Amazon, OpenAI, and Anthropic. Both rely on the same key suppliers, too, like TSMC, SK Hynix, and ASML.

What makes Nvidia and Broadcom successful is their business formulas, combining hardware and software. In terms of business structure, Nvidia pairs its GPUs with the proprietary CUDA software ecosystem, which creates a formidable lock-in effect for developers. Broadcom similarly combines its ASICs and networking hardware with VMware's virtualization software to strengthen its position.

Their gross margins reflect this pricing power and dominance—Nvidia typically boasts around 75% GPM, while Broadcom ranges from 65% to 70%—levels rarely seen among large-scale hardware companies.

Due to these parallels, many investors view Broadcom as "the next Nvidia," anticipating similar explosive upside.

As Broadcom is about to report its Q1 earnings and judging from the impressive growth numbers, many believe this is the “Next Nvidia”.

Metric | Q1 2025 (Actual) | Q1 2026 (Consensus) | YoY Growth |

Total Revenue | $14.92 Billion | $19.27 Billion | +29.2% |

Adj. EPS | $1.60 | $2.03 | +26.9% |

AI Revenue | $4.10 Billion | $8.20 Billion | +100.0% |

Gross Margin | ~79.1% | ~77.0% | -210 bps |

However, a closer examination reveals that Broadcom represents a less compelling long-term opportunity compared to Nvidia.

Same, Same, but Different

While both maintain robust competitive moats, Nvidia's defenses face pressure primarily from one direction in its core GPU domain, whereas Broadcom's advantages encounter multifaceted challenges across its key segments.

To understand Broadcom's current positioning, it helps to dissect its revenue composition. AI semiconductors account for about 31% of total revenue, experiencing explosive year-over-year growth near 65% with gross margins around 65%. This segment includes high-profile designs such as Google's TPUs, Meta's MTIA, and OpenAI's Titan chips.

Networking and switches contribute 17%, with strong growth around 30% and margins near 70%, featuring products like Tomahawk 6 and Jericho 4. VMware represents 33% of revenue but shows only flat growth of about 3%, albeit with an impressive 93% gross margin from solutions like VCF 9.0 and vSphere. Wireless products make up 12%, displaying cyclical performance near zero growth and margins around 55%, covering Wi-Fi 7/8, Bluetooth, and RF filters. Legacy software rounds out the portfolio at 7%, stable with near-zero growth and high 90% margins from assets like CA Mainframe and Symantec.

Segment | Revenue % of Total | Growth Profile (YoY) | Gross Margin | Key Products |

AI Semiconductors | 31% | Rocketing (+65%) | ~65% | Google TPU, Meta MTIA, OpenAI "Titan" |

Networking & Switches | 17% | Strong (+30%) | ~70% | Tomahawk 6, Jericho 4 |

VMware | 33% | Flat (+3%) | 93% | VCF 9.0, vSphere |

Wireless | 12% | Cyclical (0%) | ~55% | Wi-Fi 7/8, Bluetooth, RF Filters |

Legacy Software | 7% | Stable (0%) | ~90% | CA Mainframe, Symantec |

Eroding Moat

Even with dominant market shares in its primary areas, Broadcom faces intensifying competitive threats.

In AI semiconductors, Google has historically depended heavily on Broadcom for custom TPUs. Recently, however, Google shifted to a dual-vendor strategy by awarding MediaTek design contracts for the cost-optimized TPU v7e and upcoming v8e series, focused on high-volume inference workloads rather than the training-focused high-end chips Broadcom continues to supply. MediaTek offers pricing 20% to 30% lower, appealing for inference economics. Additionally, MediaTek leverages its extensive mobile business to secure greater CoWoS advanced packaging capacity from TSMC, potentially constraining Broadcom's supply access. While Broadcom retains dominance in high-end training ASICs with partners like Google, OpenAI, and Anthropic, MediaTek is rapidly gaining ground in inference, with its ASIC market share climbing from negligible levels toward 10-15%.

The networking segment encounters direct rivalry from Nvidia. Broadcom relies on the industry-standard Ethernet protocol, whereas Nvidia promotes its proprietary InfiniBand architecture for ultra-low-latency AI clusters. Nvidia also pushes its Ethernet-based Spectrum-X platform aggressively, reporting 263% growth in 2025. Nvidia's networking expansion benefits from its GPU stronghold, enabling it to bundle solutions and capture share from Broadcom's established positions in data center switches.

VMware presents perhaps the most vulnerable front. Unlike Nvidia's CUDA ecosystem, which developers embrace enthusiastically and often adopt for free, VMware functions more as a mandatory toll for many enterprises. Customers frequently express frustration over price increases without proportional innovation, viewing it as a "hostage" situation rather than a preferred choice. Growth remains tepid at around 3%, positioning VMware as a high-margin cash cow whose momentum is fading. Increasing numbers of users migrate to alternatives like Nutanix AHV or Microsoft Azure Stack HCI, eroding VMware's once-ironclad grip on virtualization.

Balance Sheet Matters too

Compounding these competitive pressures, Nvidia maintains a significantly stronger balance sheet.

Metric | NVIDIA (NVDA) | Broadcom (AVGO) | Strategy Comparison |

Total Cash | $62.6 Billion | $16.2 Billion | Fortress vs. Fuel: NVDA keeps cash to dominate R&D; AVGO keeps just enough to run operations. |

Total Debt | $8.5 Billion | $65.1 Billion | Debt-Free vs. M&A: AVGO is still paying off the "mortgage" from the $69B VMware acquisition. |

Free Cash Flow ($) | $97.0 Billion | $26.9 Billion | The Machine: NVDA generates nearly 4x the raw cash of AVGO. |

Interest Coverage | Earnings > Expense | 9.2x | Safety: NVDA has no interest risk; AVGO is safe (9.2x is solid) but must prioritize debt payments. |

D/E Ratio | 0.05 | 0.80 | Leverage: AVGO is 16x more leveraged than Nvidia. |

Nvidia's fortress-like position provides ample resources for aggressive R&D and innovation without debt servicing constraints, while Broadcom must allocate cash toward debt reduction, limiting flexibility. Nvidia's interest coverage is effectively unlimited with negligible debt, compared to Broadcom's solid but debt-burdened 9.2x coverage. Leverage ratios highlight the disparity: Nvidia's debt-to-equity stands at 0.05, versus Broadcom's 0.80.

Valuation Further Underscore the Divergence

Metric | NVIDIA (NVDA) | Broadcom (AVGO) | Market Sentiment |

Forward P/E | 25.1x | 31.4x | The Irony: Nvidia is actually "cheaper" despite its higher fame. |

Expected Rev Growth | +52% to +73% | +28% to +52% | The Size Trap: NVDA is growing faster on a much larger base. |

Earnings Growth (EPS) | +57% | +50% | Both are doubling profits roughly every 2 years. |

Nvidia trades at a forward P/E around 25.1x (with some recent estimates even lower at 16-22x depending on updates), supported by expected revenue growth of 52% to 73% and EPS growth near 57%. Broadcom commands a higher forward P/E of 31.4x despite more moderate revenue growth projections of 28% to 52% and EPS growth around 50%.

Nvidia embodies cutting-edge disruption, while Broadcom leans more on entrenched advantages and acquisitions from prior years. In summary, although Broadcom benefits enormously from the AI infrastructure wave through custom chips, networking, and software, its moat faces broader erosion risks, supply chain vulnerabilities, customer discontent in key areas, and a leveraged balance sheet that constrains maneuverability.

Nvidia, despite its own challenges, sustains a more unified, defensible position with superior financial firepower and growth momentum. For long-term investors seeking the premier AI enabler, Nvidia appears the stronger candidate over Broadcom, even if the latter remains a high-quality participant in the ecosystem.

Recommended Articles