Aluminium (ALUMINIUM) Is down 2.06% on Jun 24: Is the Market Repricing It?

Aluminium (ALUMINIUM) is down 2.06% at Jun 24 05:15(ET), now at $3167.9, with a 7-day down of 6.86%.

What is driving Aluminium (ALUMINIUM)’s stock price down today?

Aluminium prices experienced downward pressure, falling to near three-month lows, driven primarily by a significant shift in geopolitical dynamics that dramatically eased supply-side concerns in the Middle East. The primary catalyst was the progress in preliminary peace talks between the United States and Iran, accompanied by the U.S. granting a 60-day sanctions waiver to Iran. This breakthrough has fostered strong expectations for the imminent reopening of the Strait of Hormuz, a critical maritime corridor that has faced severe transit restrictions and previously disrupted global cargo flows.

The potential normalization of trade through the Persian Gulf represents a major relief for the aluminium market. The region is a vital hub for primary aluminium production, accounting for approximately nine percent of global supply. Throughout the first half of the year, shipping bottlenecks and operational curtailments in the Gulf had severely choked physical availability, driving LME cash prices to four-year highs. The prospect of these delayed cargoes and key raw materials moving freely once again has led market participants to reprice the near-term supply-demand balance, with estimates suggesting that up to 700,000 tonnes of aluminium could flow back onto the global market as logistics normalize.

The easing of physical tightness was also reflected in LME warehouse metrics. Although overall exchange inventories remained relatively low compared to historical averages, cancelled warrants declined, signaling that fewer tonnes are actively being earmarked for withdrawal. This shift in warehouse behavior, combined with the sudden unwinding of geopolitical risk premiums, shattered key psychological support levels. This technical breakdown triggered stop-loss liquidations and prompted procurement teams to defer spot purchases in anticipation of further price corrections.

Adding to the bearish momentum were broader macroeconomic headwinds and a risk-off shift in global financial markets. Expectations that the Federal Reserve will maintain a restrictive monetary policy stance to combat inflation triggered a broad sell-off in cyclical growth assets, hitting metals heavily linked to the energy transition. This risk-reduction flow coincided with a surge in the U.S. dollar, which reached its highest level in over a year. The stronger greenback has made dollar-denominated commodities more expensive for international buyers, further dampening demand expectations.

While the preliminary agreement in the Middle East has substantially reduced the upside risk for aluminium, market participants continue to monitor the physical restart of idled capacity. Rebuilding smelter output in affected areas is a slow process that typically requires months, meaning the global physical balance is expected to remain relatively tight in the near term. However, the immediate relief in transit logistics and the broader macroeconomic slowdown have successfully shifted the market narrative from supply deficit anxiety to expected normalization.

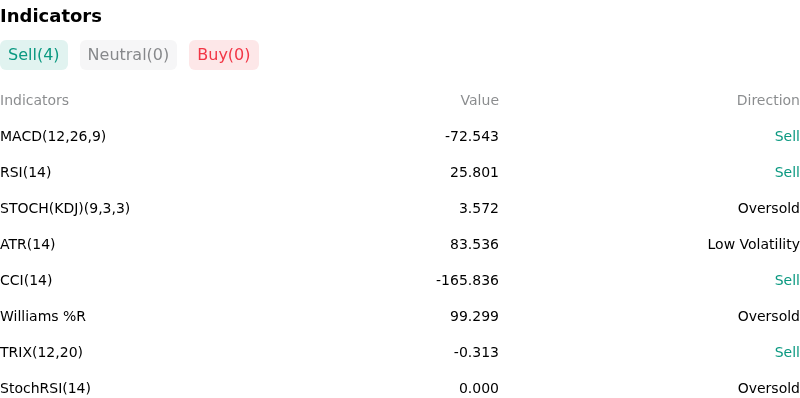

Technical Analysis of Aluminium (ALUMINIUM)

Technically, Aluminium (ALUMINIUM) shows a MACD (12,26,9) value of -72.543, indicating a sell signal. The RSI at 25.801 suggests sell condition and the Williams %R at 99.299 suggests oversold condition. Please monitor closely.

More details about Aluminium (ALUMINIUM)

Recent Events and Risks:

- Unwinding of Geopolitical Risk Premiums: The advancement of US-Iran peace negotiations—anchored by the US issuing a 60-day international oil sales license to Tehran—has sharply deflated the conflict premium previously embedded in aluminum due to Middle East smelting and shipping vulnerabilities. This easing of logistics anxiety has triggered a rapid unwinding of speculative long positions, dragging LME aluminum down by over 4% in a single session to a 12-week low near $3,179 per tonne.

- Macroeconomic Headwinds and Tech-Sector Rotation: Hawkish rhetoric from Federal Reserve officials and a broader global equity sell-off have severely dampened near-term demand sentiment. Because aluminum is heavily correlated with technology-driven trades—specifically artificial intelligence power grids, EV infrastructure, and data centers—the rotation away from growth assets has accelerated technical liquidations across the base metals complex.

- Expanding Production Capacity in China and Indonesia: Downside price pressure is mounting as global supply constraints begin to ease. High domestic smelting margins in China are driving production restarts above the country's nominal 45 million tonne national capacity cap, while rapid capacity ramp-ups in Indonesia are on track to inject substantial new tonnage into the global market, threatening to erode the metal's structural deficit quicker than anticipated.

Recommended Articles