Oracle Corp Stock (ORCL) Moved Down by 3.11% on Apr 9: A Full Analysis

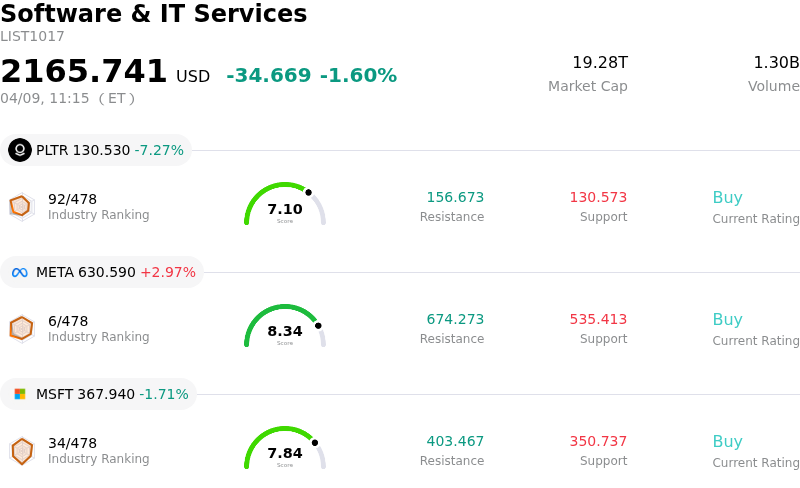

Oracle Corp (ORCL) moved down by 3.11%. The Software & IT Services sector is down by 1.60%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Palantir Technologies Inc (PLTR) down 7.27%; Meta Platforms Inc (META) up 2.97%; Microsoft Corp (MSFT) down 1.71%.

What is driving Oracle Corp (ORCL)’s stock price down today?

Oracle (ORCL) experienced a downward movement today, reflecting ongoing investor concerns despite strong underlying business performance. The primary drivers for this volatility stem from the company's aggressive capital expenditure plans related to its artificial intelligence (AI) infrastructure build-out and associated financial strategies.

Oracle has outlined plans to raise between $45 billion and $50 billion in 2026 through a combination of debt and equity to expand its cloud infrastructure capacity, essential for meeting the demand from large customers like AMD, Meta, NVIDIA, OpenAI, and xAI. This substantial capital allocation has led to investor apprehension regarding the potential pressure on free cash flow and an increased risk profile due to a rising debt load. Reports suggest that heavy spending on AI-focused data centers has pushed Oracle's free cash flow into negative territory, a condition that could persist until around 2030.

Adding to market sentiment, Oracle recently undertook a significant workforce optimization initiative, with estimates suggesting cuts could affect up to 30,000 employees globally. While management frames these layoffs as a move towards a more agile and focused organizational structure, they are largely seen as a measure to free up cash and streamline operations to fund the aggressive AI infrastructure build-out. This decision to trade human payroll for AI infrastructure, though potentially improving margins long-term, introduces short-term disruption and investor wariness.

Despite these concerns, Oracle's financial results for Q3 FY2026 showed robust growth, with total revenue rising 22% year over year to $17.2 billion, driven by a 44% jump in cloud revenue and an 84% surge in cloud infrastructure (IaaS) revenue. The company's remaining performance obligations (RPO), a measure of contracted sales not yet recognized, skyrocketed 325% year over year to a record $553 billion, primarily due to large-scale AI contracts. This impressive backlog suggests a strong pipeline for future revenue generation.

Analysts generally hold a bullish long-term outlook for Oracle, with a consensus "Buy" rating and an average price target significantly above current levels. They view Oracle as a compelling AI infrastructure play, noting the potential for sustainable gross margin expansion as these large contracts scale. Furthermore, Oracle recently announced Fusion Agentic Applications for Customer Experience, Finance, and Supply Chain, showcasing its continued innovation in embedding AI into its cloud applications. The company also announced a new Chief Financial Officer, Hilary Maxson, a move viewed favorably by some analysts who believe she is well-suited to manage Oracle's large capital expenditure programs.

However, the disconnect between strong financial results and the stock's year-to-date performance, including today's movement, highlights that market concerns over the capital-intensive nature of Oracle's AI pivot and its impact on free cash flow are currently outweighing the positive operational momentum. Some analysts suggest waiting for a pullback before deploying capital, indicating lingering valuation concerns despite the strong growth catalysts.

Technical Analysis of Oracle Corp (ORCL)

Technically, Oracle Corp (ORCL) shows a MACD (12,26,9) value of [-3.30], indicating a neutral signal. The RSI at 43.09 suggests neutral condition and the Williams %R at -66.40 suggests oversold condition. Please monitor closely.

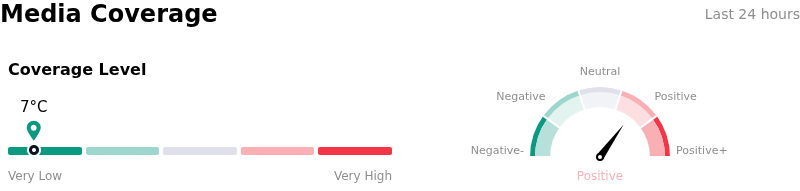

Media Coverage of Oracle Corp (ORCL)

In terms of media coverage, Oracle Corp (ORCL) shows a coverage score of 7, indicating a very low level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Oracle Corp (ORCL)

Oracle Corp (ORCL) is in the Software & IT Services industry. Its latest annual revenue is $57.40B, ranking 9 in the industry. The net profit is $12.44B, ranking 9 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $249.04, a high of $400.00, and a low of $155.00.

More details about Oracle Corp (ORCL)

Company Specific Risks:

- Oracle's aggressive $50 billion capital expenditure plan for fiscal 2026 to expand AI data center infrastructure raises concerns regarding potential margin pressure if demand growth does not match the pace of investment, and is linked to worries about increased debt and negative free cash flow.

- Analyst skepticism persists regarding the conversion of Oracle's substantial $553 billion remaining performance obligations (RPO) backlog into actual revenue and sustainable profit, suggesting it may represent customer intentions rather than guaranteed future income.

- Oracle has initiated global workforce reductions, with reports indicating thousands to potentially tens of thousands of layoffs, aimed at managing costs associated with its aggressive AI expansion, which could impact operational stability and raise questions about management's strategic judgment.

- The company continues to exhibit negative free cash flow (FCF) and experienced contracted profit margins in Q3 2026, as the capital-intensive nature of its Oracle Cloud Infrastructure (OCI) growth necessitates significant investments in hardware like GPUs.

Recommended Articles