Why ASML is a buy After Terafab Deal?

$55 Billion That Might Later Reach $115 billion, A Vote Of Confidence

TradingKey - The CEO of Tesla and SpaceX, Elon Musk, has revealed his intent to work with ASML Holdings NV (NASDAQ: ASML) in the production of chips for Tesla and SpaceX ahead of SpaceX’s IPO (CNBC). To me, I interpret this as a vote of confidence. The facility is estimated to spend around $55 billion and later reach $119 billon. That said, this already gives me an early optimism on ASML, and when I dig deeper, this comes out better. For example, let’s take a pragmatic view. Intel has already joined Terafab and will be offering 14A process technology, which also drives the facility to produce around 100-200 billion custom AI and memory chips per year.

Already, the target custom AI chips output is 100,000 wafers per month, towards a million, which is around 70% of what TSMC is producing currently per year. It seems overly ambitious, but the hack is here. The collaboration with ASML, the producer of High Extreme Ultraviolet (EUV) lithography systems, is what matters. When I consider that varied reports state that production of this capacity requires between 50 and 100 EUV lithography machines, then it means Terafab might require around this number to deliver this capacity.

Terafab volume production is projected for 2027 according to Fintech Weekly, and this gives an impression of possible revenue upside to ASML. One machine costs around $400 million, and if ASML makes a sale of 50 EUV machines to Tesla and SpaceX Terafab, that would mean a minimum of $20 billion from one customer in the near future. To achieve 70% of TSMC’s output, it would need more than 100 EUV machines, which tells me that ASML has a solid revenue growth potential.

Why It’s Still Early To Enter After The Pullback

So far, ASML’s stock price has gained by over 80.01% YTD. However, it is worth noting that, as usual, investors sometimes cash in some profits earned after a long uptrend. I believe this is what resulted in a 5% bearish move. This pullback is now overridden by the current bullish trend, which I believe is now driven by potential cash flows from Tesla, SpaceX, Terafab, and other semiconductor manufacturers. For example, in the Q1’26 Investor transcript, the company indicates its 2026 expansion plans, such as executing more than 60 Low-NA EUV systems to around 80 systems in 2027.

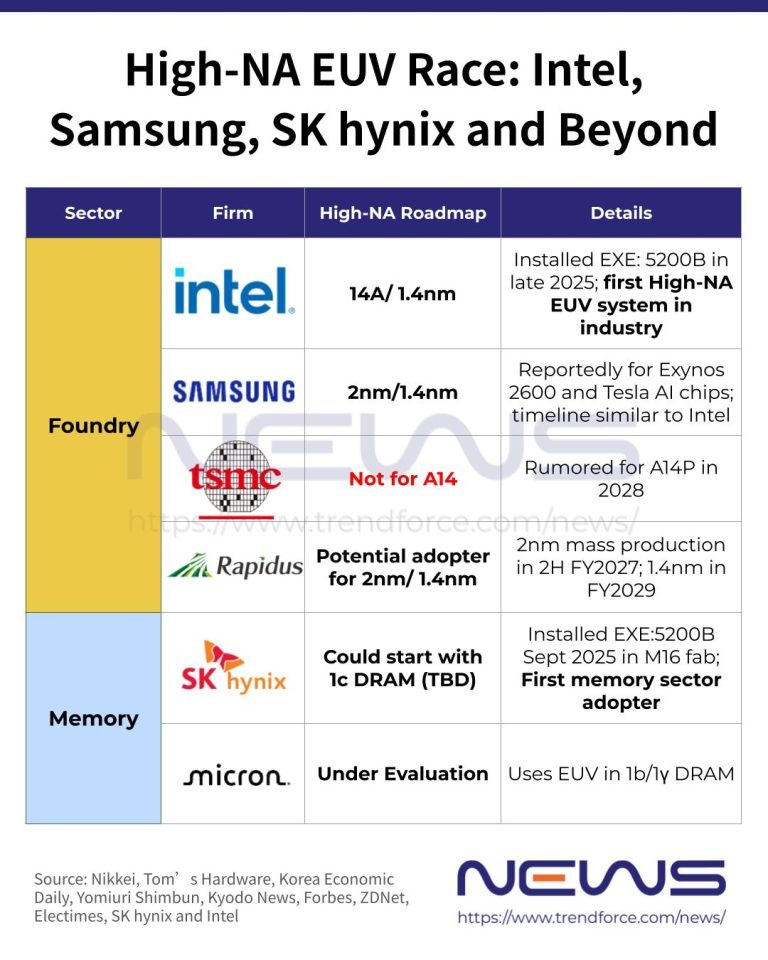

One EUV costs a minimum of 400 million, meaning ASML is likely to record a revenue of 24 billion from these EUV sales. Recall, Terafab’s backers have the capital to fund their equipment orders. For example, Samsung, TSMC, Intel, and SK Hynix. According to TrendForce, these legacy customers had kicked off production of 2nm mass production in 2025. Still, they are planning to kick off 1.4 nm mass production by 2027-28, which positions ASML’s market for its next-generation EUV lithography.

To me, investors who are still weighing on whether to buy here, I think it is not too late to enter at the current position, because the current top-line performance and estimated future top-line might drive an upward price momentum.

Beyond Numbers, Will ASML Keep Up With a Double-Digit Climb In 2026?

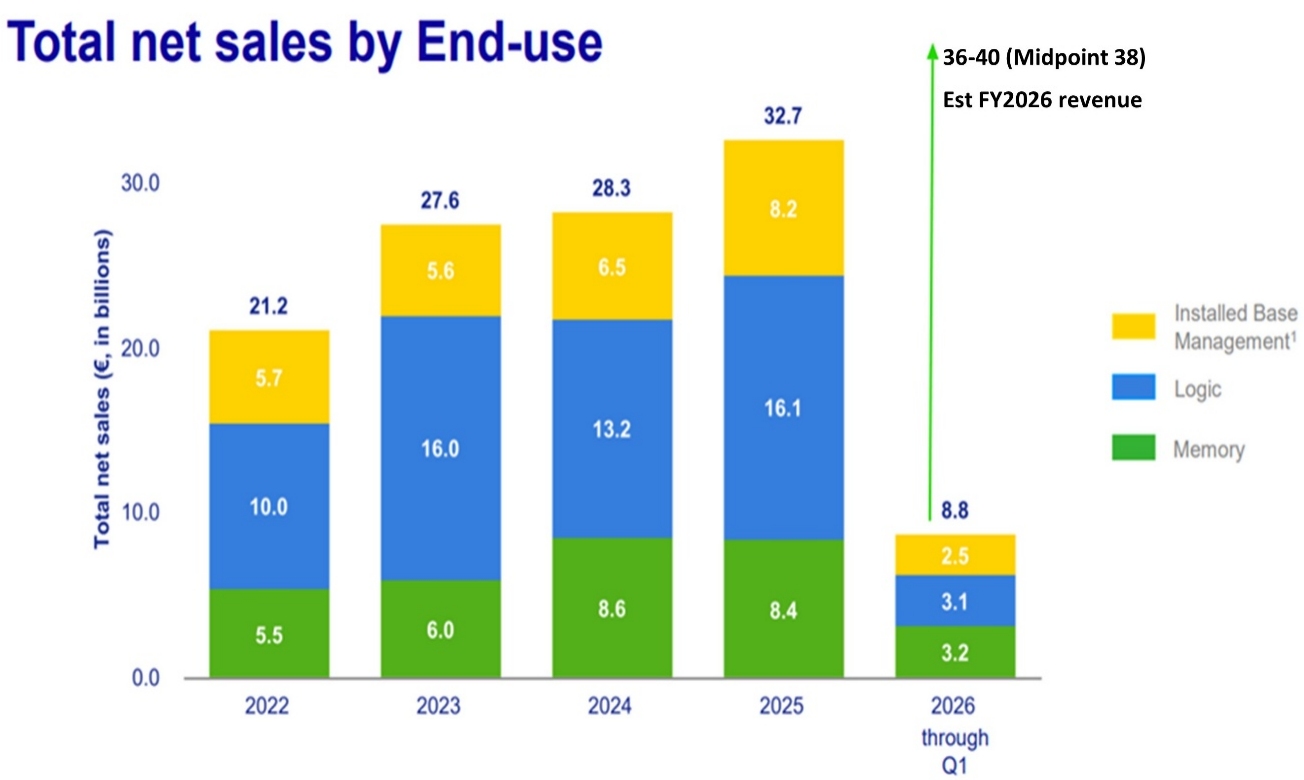

ASML fundamentals align with its top line because the latest fiscal quarter, Q1’26, reported a revenue of €8.8 billion and expects a revenue of €8.4 billion to €8.9 billion in Q2’26. Going by the fundamentals discussed above, particularly the sale of EUV machines, estimated to reach 80 shipments from 60 shipments, this is likely to be a revenue driver this year. Additionally, contracts that ASML is entering into, such as with Tesla and SpaceX, are some of the long-term revenue growth drivers. The near future delivery of around 100 EUV machines for SpaceX’s state-of-the-art Terafab to commence its own production of AI chips and space data centers, this positions ASML for more revenue gain.

That said, I believe ASML is capable of beating management’s FY2026 revenue estimate of €36 billion to €40 billion. At the midpoint of €38 billion, ASML could record 12.79% revenue growth YoY in FY202, which is a double-digit. When I annualize Q2’26 revenue midpoint of €8.65 billion, it gives an estimated revenue of €34.6 billion, meaning the estimated EUV sales are expected to drive the sales for the revenues to hit €36 billion to €40 billion. The margins have also improved, as FY2025 gross margin stood at 52.8%, and now the management forecasts a margin of 53%.

Source: ASML (Q1’26)

Source: ASML (Q1’26)

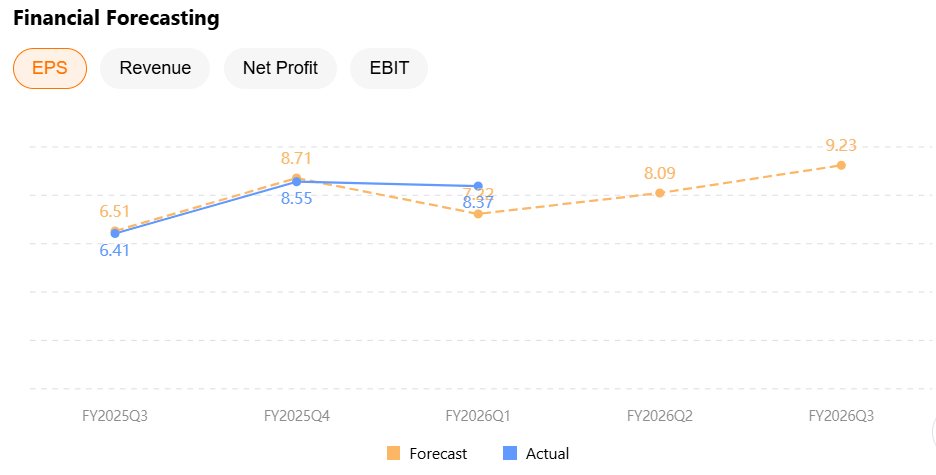

Moving to earnings, the way revenues have been on an uptrend, the same has been happening to the earnings trend. In Q1’26, the earnings reached $7.15, up from $5.99, representing 19.45% YoY growth. Following the management revenue outlook of around €38 billion, the earnings guidance also stands at around €8.09 in Q2’26 and €9.23 in Q3’26. So far, ASML earnings have been beating analysts’ estimates. For example, the company beat analysts’ earnings estimates in Q1’26 to €8.07, representing 15.9% earnings beat, and I believe that with the impressive fundamentals above, the company is likely to beat earnings estimates in FY2026.

Source: TradingKey

Source: TradingKey

I will now value this company driven by the fundamentals above, using the P/E multiple. I will use my assumptions alongside Wall Street and Seeking Alpha analysts’ estimates to come up with my valuation. I will begin with the projected earnings in Q2’26, which is around €8.09, and then I will annualize it, which came in at €32.36 annual EPS estimate for the FY2026 on the bear side. Given the fundamentals discussed above, I will assume the company has the potential to deliver a fair EPS beat of around 8% per quarter, below Q1’26 15% earnings beat. This means potential EPS of €9.04 in Q2’26, €9.76, and €10.54. Altogether, FY2026 has the potential to deliver an EPS of €37.71, which is not far from Wall Street and Seeking Alpha Analysts’ EPS estimates (Image below) at around €36.28.

For the Forward P/E, I will take the analyst’s estimate of 57.125x from Macrotrends, which matches my optimistic view above, to value this company within analysts’ estimates. This gives a possible price estimate of $2,157.6 or a 12% upside potential by the end of 2026.

Takeaway: Why I Am Staying Bullish

I am reiterating my bullish stance driven by the Terafab’s which are coming up and creating the demand for ASML’s EUV and High-NA EUV orders from new and legacy customers. Already, the company is recording double-digit top line, which indicates the momentum has kicked off. The backside of this bullish perspective is that if AI-capex stumbles, this may hit ASML’s sales, which may limit my earnings projections.

Recommended Articles