Not Nvidia. Not Micron. This Underrated Artificial Intelligence (AI) Infrastructure Stock Will Be the Biggest Winner of 2026

Key Points

Dell Technologies has stepped on the gas, driven by the terrific demand for its AI servers.

The stock is trading at an extremely cheap valuation given its phenomenal growth.

Dell stock could become a multibagger and outperform AI infrastructure stocks such as Micron and Nvidia this year.

- 10 stocks we like better than Dell Technologies ›

Nvidia (NASDAQ: NVDA) and Micron Technology (NASDAQ: MU) have been at the center of the artificial intelligence (AI) infrastructure boom in recent years, as they design and manufacture mission-critical chips that help run AI applications.

Not surprisingly, shares of both companies have delivered stellar returns. Nvidia stock has shot up 492% over the past three years. Micron, on the other hand, has jumped by a stunning 1,420% over the same period. The good part is that both companies can continue to deliver healthy gains, primarily due to the massive investments in AI data centers.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Nvidia has a huge revenue backlog of over $1 trillion for 2026 and 2027 for its Blackwell and Vera Rubin graphics processing units (GPUs). What's more, the semiconductor giant is making terrific progress in new areas such as server processors and physical AI, which should ensure its red-hot growth continues over the long run.

Meanwhile, Micron's memory chips help the AI accelerators designed by Nvidia and other chipmakers to perform up to their full potential. As a result, Micron has been overwhelmed by strong memory demand, leading to red-hot revenue and earnings growth. However, I believe another stock has the potential to outperform both Nvidia and Micron, given its key role in the AI infrastructure ecosystem -- Dell Technologies (NYSE: DELL).

Let's look at the reasons why this tech giant could be the biggest winner of the AI data center boom this year.

Image source: The Motley Fool.

Dell Technologies' latest results mark its arrival on the AI infrastructure scene

Dell released fiscal 2027 first-quarter results (for the three months ended May 1) on May 28. The stock shot up by 33% the following day. Dell's revenue rose by a whopping 88% year over year to a record $43.8 billion, significantly above the $35.5 billion consensus estimate.

Its non-GAAP earnings also rose to a record $4.86 per share, up by 214% from the year-ago period. Analysts would have settled for just $2.99 in earnings per share. It is worth noting that Dell's revenue and earnings outpaced Nvidia's growth last quarter. The AI chip giant had reported an 85% year-over-year increase in revenue and a 140% jump in earnings in the first quarter of fiscal 2027 (which ended on April 26).

The booming demand for AI-optimized servers anchored Dell's remarkable performance. The company has been designing and manufacturing AI server factories for multiple partners, including Nvidia, Google Cloud, SpaceX, OpenAI, Palantir Technologies, CrowdStrike, and others. Dell noted on its latest earnings call that it now builds AI servers for more than 5,000 customers, including sovereign clients, neocloud providers, and enterprises. Its AI customer base has increased by over 50% in just six months.

This explains why Dell has been witnessing terrific growth in AI server orders. Specifically, Dell booked $24.4 billion in new AI server orders last quarter, while it shipped $16.6 billion worth of AI servers. So, Dell received more orders than it fulfilled. This explains why the company ended the quarter with a massive AI server backlog of $51.3 billion.

Dell management notes that AI server demand has been exceeding supply. As a result, it expects to end the year with "meaningful backlog," suggesting that the remarkable growth that it is clocking is here to stay. Importantly, Dell has substantially increased its fiscal 2027 revenue guidance to $167 billion, well above the prior estimate of $140 billion.

The company anticipates $60 billion in AI server revenue this year, significantly higher than the $25 billion it generated in fiscal 2026. What's worth noting is that the AI server market is anticipated to clock a 35% annual growth rate between 2026 and 2034, according to Fortune Business Insights. It is expected to generate a whopping $2.85 trillion in revenue at the end of the forecast period, as compared to $262 billion this year.

Dell is clearly growing faster than the end market, which means it is gaining a larger share of this lucrative space. This should pave the way for terrific long-term growth at Dell, which is why investors should consider buying this AI stock before it soars higher.

The stock's cheap right now, and that sets it up for terrific gains

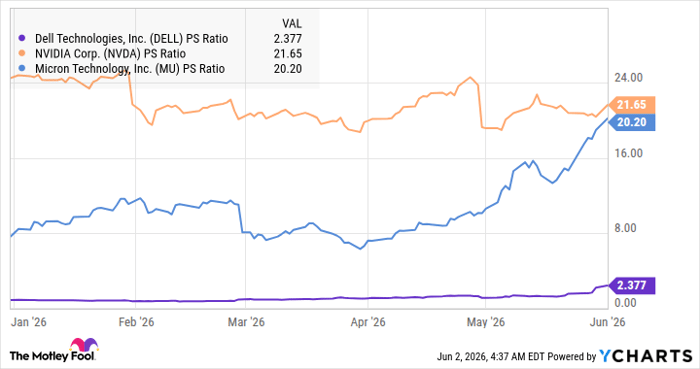

Dell is trading at just 2.3 times sales. That's well below the Nasdaq Composite index's sales multiple of 5.6. What's more, Dell is significantly cheaper than both Micron and Nvidia as well.

Data by YCharts

As Dell is forecasting an impressive 47% jump in revenue this year, it should ideally trade at a premium to the Nasdaq Composite. But even if it trades at the index's average sales multiple at the end of the current fiscal year, its market cap could surge to $935 billion. That's more than 3x ts current market cap, suggesting it isn't too late for investors to buy this potential multibagger.

Should you buy stock in Dell Technologies right now?

Before you buy stock in Dell Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dell Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $449,393!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,366,006!*

Now, it’s worth noting Stock Advisor’s total average return is 983% — a market-crushing outperformance compared to 212% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 3, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike, Micron Technology, Nvidia, and Palantir Technologies. The Motley Fool has a disclosure policy.

Recommended Articles