Moody’s Puts U.S. Recession Odds at 50%, and the Signals Are Hard to Ignore

TradingKey - For a while, talk of a U.S. recession had slipped quietly into the background, replaced by a more familiar mix of inflation concerns and trump tariffs. Now, it is back at the centre of the conversation. The rise in oil prices — and the prospect that they may rise further — has become the thread tying those anxieties together.

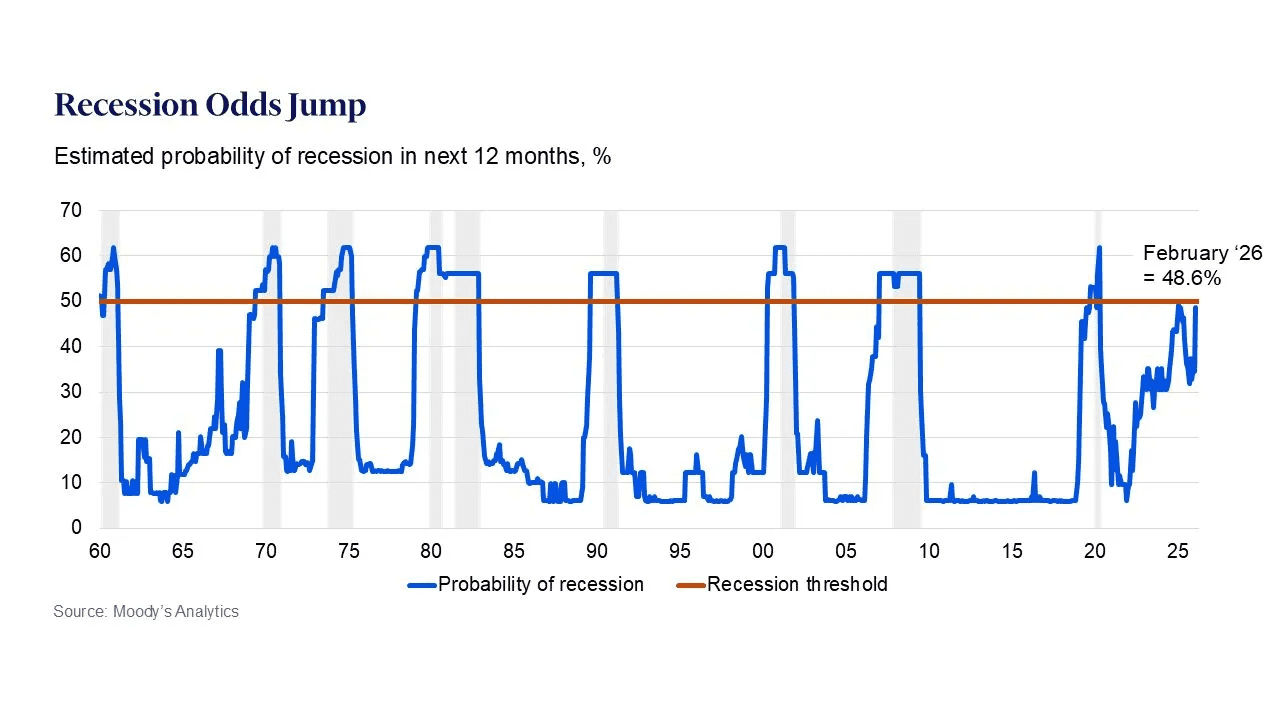

On the surface, America’s energy independence should provide some insulation. Domestic output of oil and natural gas now more or less matches domestic consumption, leaving the U.S. less exposed than many of its peers. Yet Moody’s Analytics, even before the latest escalation in Iran, was seeing warning signs in the data. Its machine‑learning recession model put the probability of a U.S. economic downturn within the next year at 49%. Chief economist Mark Zandi said the next run of numbers is likely to push that figure above 50% — a statistical coin‑flip that few will find comforting.

Irwin Stelzer of the Hudson Institute argues that any honest reading of the U.S. outlook has to pass through three lenses: history, the current numbers, and the stubborn reality underneath them. History, he writes, tells a consistent story. Before each of the four major post‑war downturns — 1973‑75, 1980, 1981‑82 and 1990‑91 — real energy prices climbed by an average of 17.5%. That pattern gave rise to a consensus of thumb in economics: when oil becomes expensive, growth rarely lasts.

The contemporary evidence is not much kinder. In February 2026, U.S. non‑farm job openings fell by 92,000, a sharp miss against expectations of a 59,000 increase. January’s figure was revised down to just 126,000 new positions, and adjustments to December and January together erased 69,000 jobs previously reported. What had been a fragile labour market is now cooling faster than most policymakers anticipated.

Inflation continues to smoulder beneath the surface. Over recent months, the consumer‑price index has been rising by an average of 2.4% month‑on‑month, while the Federal Reserve’s preferred measure — the core personal‑consumption‑expenditure index — is running at an annualised 3.1%. Both stand comfortably above the Fed’s 2% target.

Growth, too, has turned sluggish. Real GDP expanded at an annual rate of just 0.7% in the fourth quarter of 2025, a sharp slowdown from 4.4% in the previous quarter and well below expectations. Consumption is tempering; investment has pulled back.

Together these figures paint a picture that feels uncomfortably familiar: a slowing economy, only partially tamed price pressures, and energy uncertainty radiating from the Middle East. For the Federal Reserve, the trade‑off between sustaining growth and containing inflation has rarely looked more fragile.

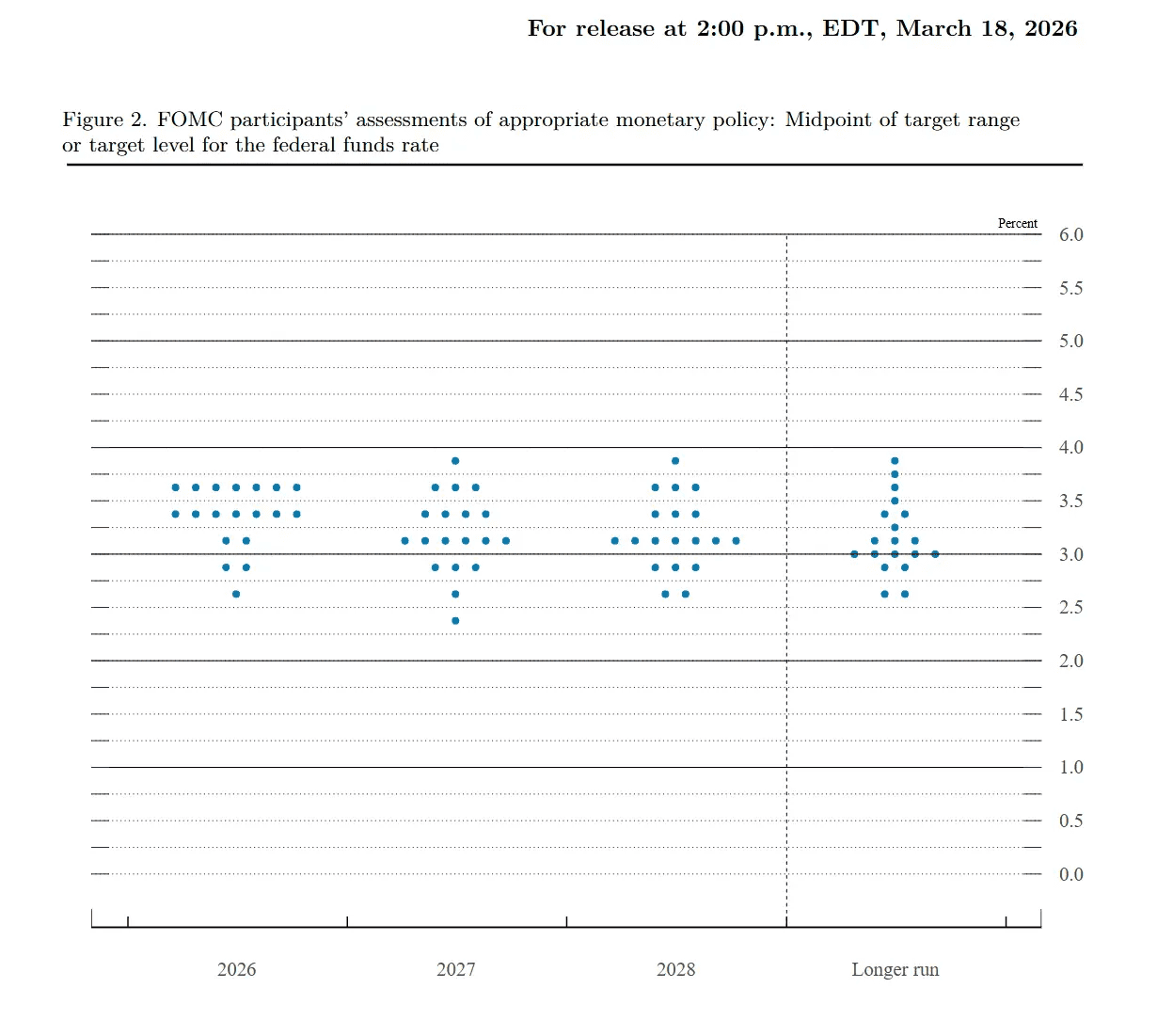

At its meeting on Wednesday, the Federal Open Market Committee voted 11–1 to leave the target for the federal funds rate unchanged at 3.5–3.75%. The “dot plot” of members’ forecasts hints at just one rate cut this year and another in 2027, though the timing remains vague.

Fed chair Jerome Powell also found himself fielding political questions — not least over President Trump’s order for the Justice Department to investigate a multibillion‑dollar renovation of the Fed’s headquarters. Powell said he had no intention of stepping down until the inquiry was concluded “openly, transparently and decisively.” For markets, his persistence complicates the earlier assumption that a successor might align more readily with Trump’s preference for lower rates.

Yet to many economists, the greater risk lies not in the numbers themselves but in how policymakers respond to them. Peter Schiff, a long‑time critic of ultra‑easy money, argues that higher oil prices are already recessionary, and that the standard prescription of looser fiscal and monetary policy could fan inflation again. When governments sense contraction, he says, their instinct is to flood markets with liquidity and increase leverage. But with supply — especially in energy — tightened by war and under‑investment, such stimulus only fuels demand, setting off a new round of price rises.

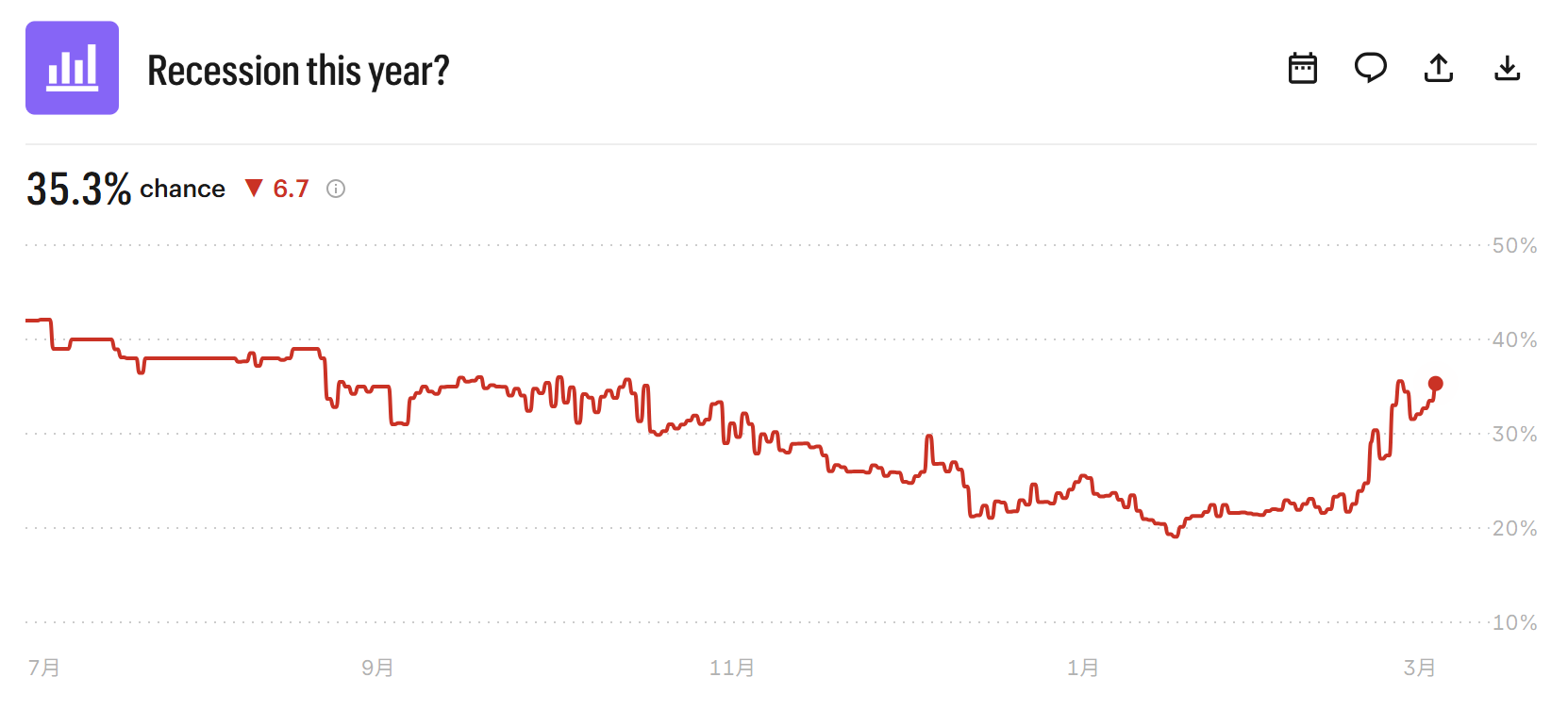

In an economy where jobs, energy and markets are all flashing red at once, it is hard to dismiss the gloom as mere pessimism. Analysts are quietly adjusting their numbers. Goldman Sachs now places the probability of recession at 25%, while trading on the prediction platform Kalshi shows collective odds rising from 22% to 35.3%.

Recommended Articles