U.S.-Iran Ceasefire Drives Asia-Pacific Stock Surge, South Korea Index Triggers Circuit Breaker Again.

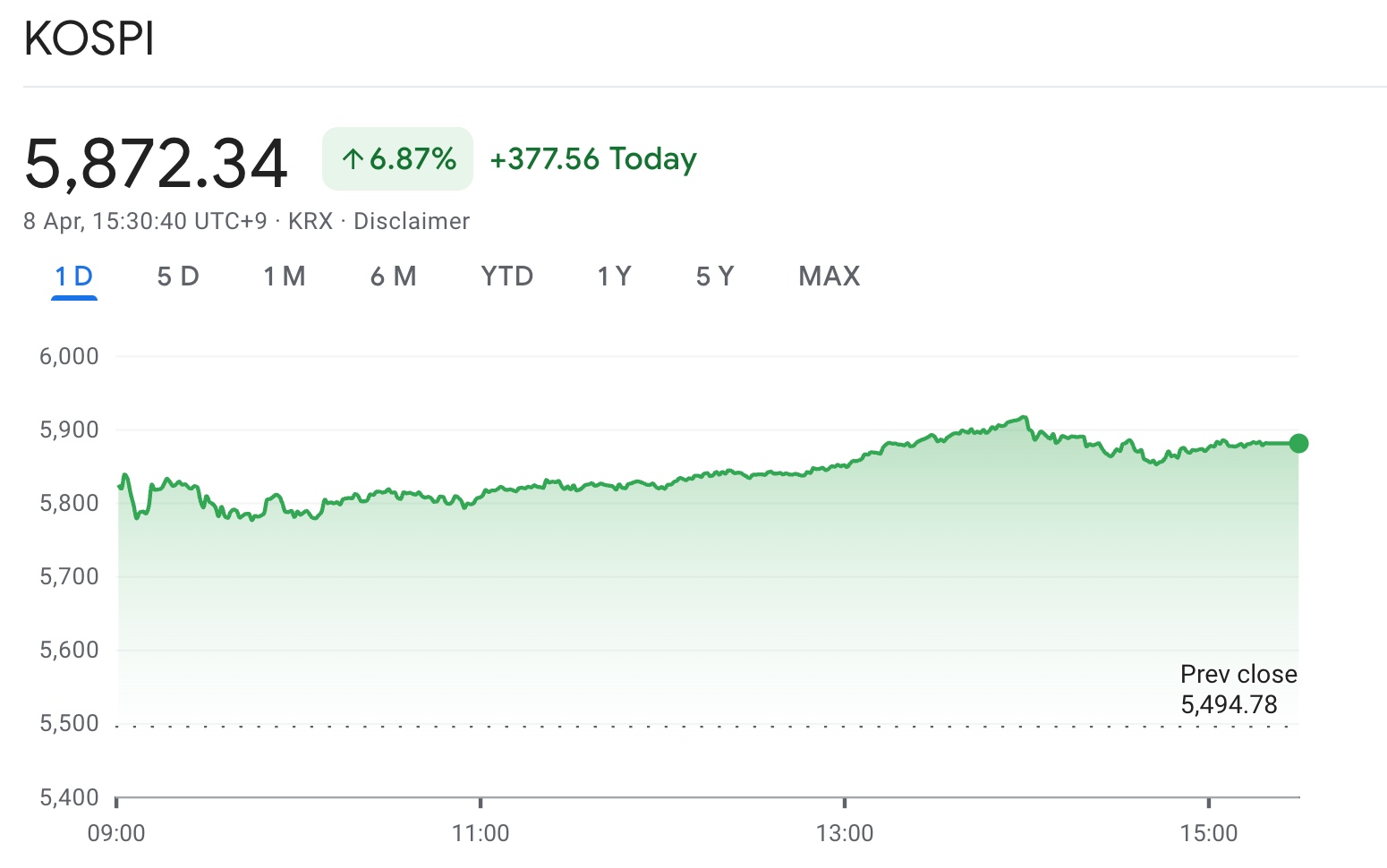

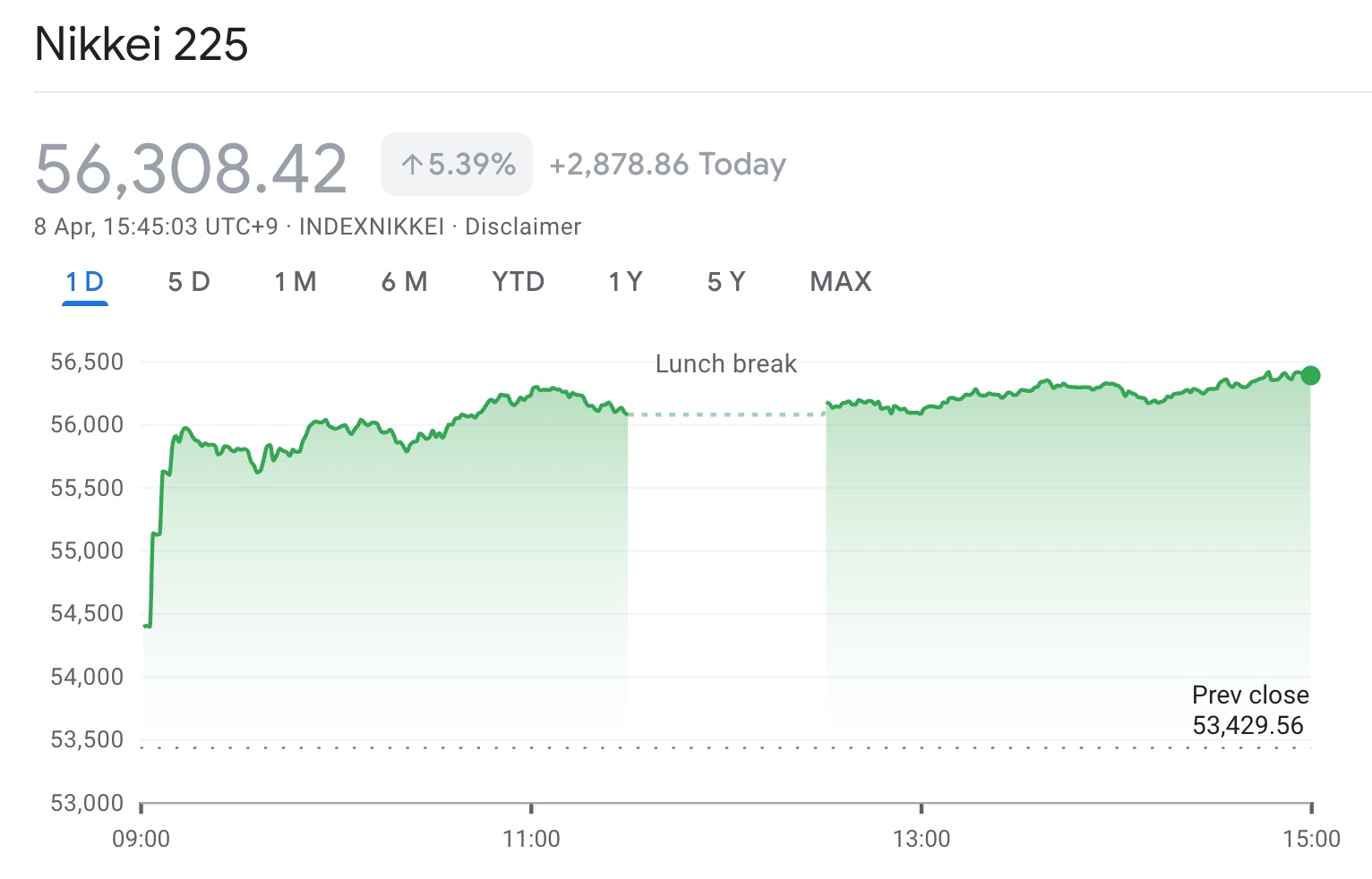

TradingKey - During the April 8 Asia-Pacific trading session, stock markets in most Asia-Pacific countries continued to rise, driven by the ceasefire in the U.S.-Iran conflict. The Nikkei 225 Index closed up 5.39% at 56,308.42 points; the KOSPI Index triggered a circuit breaker within minutes of the opening and closed up 6.87% at 5,872.34 points.

[Performance of Nikkei 225 and KOSPI Indices, Source: Google Finance]

On the news front, the United States and Iran previously declared a formal ceasefire agreement. Diplomatic statements from multiple parties indicate a decreased probability of conflict escalation, driving a collective rebound in global risk assets. The geopolitical premium that had previously suppressed market sentiment retreated rapidly, and capital flowed back into equity markets.

Structurally, this round of rebound was most prominent in export-oriented economies, particularly the technology sector. As core hubs of the global manufacturing and technology supply chains, Japan and South Korea saw significant stock index recoveries driven by improved external demand expectations and a decline in risk premiums amid easing geopolitical risks. The semiconductor, automotive, and electronics sectors, in particular, became the primary direction for capital inflows.

The easing of U.S.-Iran tensions not only signifies a decline in geopolitical conflict risk but also has a direct impact on energy markets. Expectations of rising oil prices, previously driven up by the conflict, have begun to cool, and market concerns over rising inflation have eased simultaneously. This shift further improved global liquidity expectations, providing room for valuation recovery in risk assets.

However, it is important to note that disagreements remain regarding the current so-called "ceasefire agreement." If subsequent negotiations experience setbacks or the geopolitical situation deteriorates again, market sentiment could quickly reverse. Furthermore, the global macroeconomic environment still faces uncertainties, including the path of monetary policy and economic growth prospects, which could constrain this round of rebound.

Overall, the significant rise in Japanese and South Korean stock markets is essentially a dual pricing recovery for "geopolitical risk mitigation and improved liquidity expectations." Against the backdrop of a short-term recovery in risk appetite, the market may sustain its rebound momentum, but the medium-term trend still depends on actual progress in U.S.-Iran relations and its continued impact on global macro variables.

Recommended Articles