Where Will Micron Stock Be in 3 Years?

Key Points

Micron has emerged as a category leader of high-bandwidth memory solutions for artificial intelligence (AI) hyperscalers.

The company's revenue and earnings growth are explosive, and secular tailwinds suggest the company's outlook remains strong.

Micron stock could be headed for even further gains as its valuation multiples reach more premium price levels.

- 10 stocks we like better than Micron Technology ›

Over the last year, Micron Technology (NASDAQ: MU) has emerged as one of the most compelling stories in the artificial intelligence (AI) semiconductor landscape. Following its 162% surge in just the last six months, Micron shares now hover around $440.

The question smart investors are asking is whether this rise is a byproduct of a temporary boom or the beginning of a structural growth rally. Over the next three years, I'm forecasting Micron stock to soar even higher. Read on to find out why.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Micron Technology.

What is driving Micron stock higher?

AI hyperscalers are deploying millions of clusters of graphics processing units (GPUs) across their data centers. These structures consume high-bandwidth memory (HBM) for training and inference of generative AI models.

Micron's recent ascent is fueled by explosive demand for these high-performance memory solutions -- supported by the $700 billion AI infrastructure buildout. The company's HBM3E and upcoming HBM4 products are already sold out for 2026 -- allowing the company to command premium pricing and widen the profit margins across its DRAM and NAND chip suites.

As big tech continues allocating infrastructure budgets toward additional capacity solutions across memory and storage, Micron remains in a position to accelerate both revenue and earnings over the coming years.

Does the AI memory supercycle have multiyear momentum?

In the past, memory cycles have been highly cyclical as they relied heavily on device upgrades from consumers and enterprises. Today's AI revolution is changing this narrative, though.

Trends in digitization, 5G networks, and cloud storage were not as robust during prior memory cycles. But with the introduction of next-generation services across robotics, agentic AI, and autonomous systems, AI models are scaling at an unprecedented speed.

As inference workloads evolve from pilots to production, the need for HBM becomes even more critical. Against this backdrop, it's easy to justify the HBM market's 40% annual growth rate -- estimated to reach $100 billion by 2028.

What will Micron stock be worth by the end of the decade?

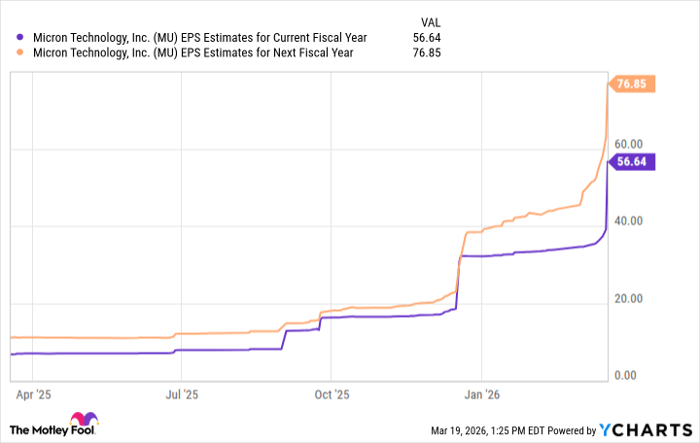

In fiscal 2025 (which ended Aug. 28), Micron generated $7.59 in earnings per share (EPS). Through the first six months of fiscal 2026, the company's EPS has already risen by more than twofold -- coming in at $16.68. What's even better is that management guided for even higher earnings of $18.90 for fiscal Q3.

MU EPS Estimates for Current Fiscal Year data by YCharts.

Assuming Micron achieves Wall Street's consensus earnings targets above, and then begins to operate at a more mature growth profile thereafter, I think it's appropriate to model EPS in the range of $95 and $115 by fiscal years 2028 and 2029.

Applying a trailing price-to-earnings (P/E) multiple between 18x and 25x -- the realistic range Micron's shares have traded historically -- to my estimated fiscal 2029 EPS target would yield an implied share price in the range of $2,070 to $2,875, about 4.7 times to 6.5 times the current share price.

While competitive forces or macroeconomic conditions represent legitimate risks, ongoing AI demand creates a strong floor for Micron in the AI infrastructure age.

In my eyes, Micron is not a participant in a fleeting cycle. Rather, the company is a critical enabler powering a new computing era -- positioning the stock for meaningful valuation expansion by decade's end.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $495,179!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,058,743!*

Now, it’s worth noting Stock Advisor’s total average return is 898% — a market-crushing outperformance compared to 183% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 22, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

Recommended Articles