Record Inflows Fail to Deliver Decent Gains: Are US Stocks Being Abandoned by Capital?

TradingKey - On February 25, Deutsche Bank ( DB) macro strategist Tim Baker released a report showing that although global capital is pouring into the U.S. stock market at an unprecedented pace, its relative performance has been surprisingly disappointing.

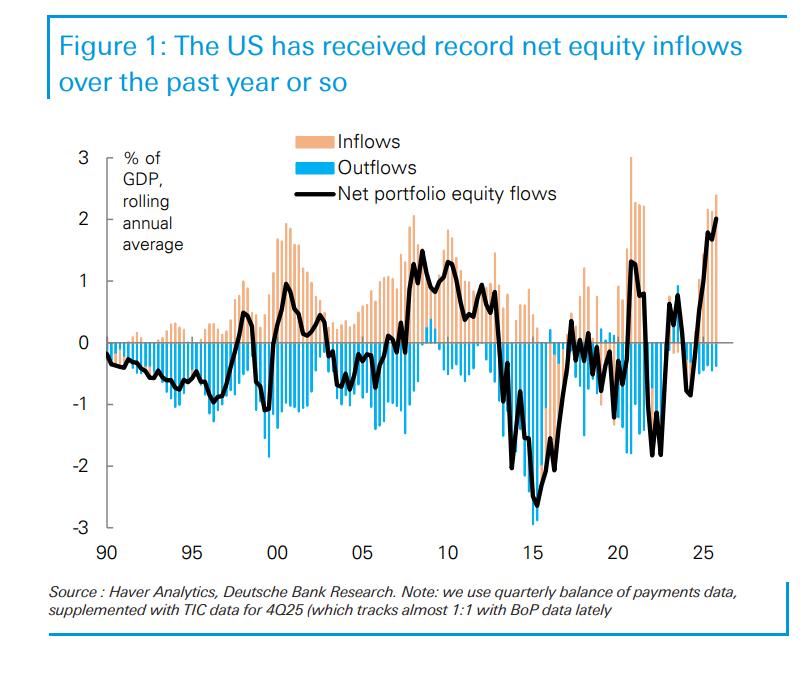

The U.S. stock market once set global records with its extraordinary ability to attract capital. Tim Baker stated in the report that the popularity of U.S. equities across the market is incredible. Net equity inflows have never been stronger. Throughout 2025, net inflows reached a staggering 2% of U.S. GDP.

This massive volume of capital provides significant support to the U.S. economy. Deutsche Bank noted that these record net equity inflows alone are sufficient to single-handedly finance two-thirds of the U.S. current account deficit.

During that capital feast, global investors focused their attention on the U.S. market: foreign capital aggressively increased holdings, while domestic U.S. investors preferred to concentrate heavily on their home market, with a persistently low appetite for international stocks.

However, the enthusiasm for U.S. asset investments ignited by Donald Trump's return to the White House is cooling at a startling rate. Currently, global capital is systematically exiting the U.S. market and flowing into European and Asian assets instead, quietly initiating a profound global portfolio rebalancing.

Worst Performance in 15 Years

While global capital rushed into U.S. equities, this fervor did not translate into proportional returns. In hindsight, the massive move to overweight U.S. stocks appears particularly ill-timed.

For over a decade, "buying the dip" in U.S. stocks was a universally recognized winning strategy, but over the past year, the rules of the game have fundamentally changed. Deutsche Bank's monitoring found that the previously dominant U.S. market is no longer the main protagonist, as cheaper, cyclical equity markets have begun to lead globally.

The U.S. market finds itself in an awkward position, lacking both a price advantage and cyclical characteristics.

"The extent to which U.S. equities have underperformed non-U.S. assets has become evident in year-over-year calculations in recent months. A relative underperformance of this magnitude has not been seen in the past 15 years," said Tim Baker. Although U.S. performance remains solid over a three-year horizon, it has currently fallen to recent lows.

Multiple factors are weighing on the attractiveness of U.S. assets: tech stocks remain under pressure, policy uncertainty persists, and economic growth has slowed to a modest annualized rate of 1.4%, collectively shaking the core competitiveness of U.S. equities.

At the same time, rising expectations for fiscal expansion in Europe and signs of a recovery in the German economy have made European assets the biggest winners in this round of global capital reallocation.

Since late December last year, U.S. stocks have been fluctuating within an unusually narrow range, failing to either drop significantly or break out to the upside. Notably, even when Trump's powers were curtailed (such as his loss in a tariff lawsuit last week), the U.S. market failed to rebound. This detail suggests that the market's coolness toward U.S. equities is not merely due to policy concerns, but rather a fundamental shift in deeper capital flows.

AI Bubble Fears and a Collective Tech Sector Stall

Last Sunday, Citrini Research released the "2028 Global Intelligence Crisis" report, detailing potential threats posed by AI to the U.S. economy and the global crisis it could trigger.

Although some experts believe the market overreacted to the report's extreme scenarios, the event undoubtedly highlights that investor alertness to an AI bubble has reached a high level.

Capital market trends directly reflect investor anxieties, with continued selling of software companies and industries vulnerable to automation. To date, the U.S. software index has fallen by a total of 24% this year. Notably, Duolingo (DUOL) has plummeted 80% from its May 2025 high, serving as a prime example of market doubts regarding AI's potential to cannibalize traditional business models.

For the past three years, investors were accustomed to interpreting AI through the lens of new growth; now, focus has shifted to the risk of AI disrupting industry profitability. In an environment highly dependent on market momentum, price fluctuations are more easily amplified.

Allocation Window Opens for Non-U.S. Assets

Given the worst relative performance of U.S. stocks in 15 years, combined with the previous widespread overweighting of U.S. positions, long-term capital now has ample reason to re-evaluate its allocation strategy.

A shift of capital from U.S. to non-U.S. markets requires a core premise: non-U.S. markets must be capable of keeping pace with or even matching the performance of U.S. equities. According to Deutsche Bank, this premise is not only now met but is also fully justified.

First, there is strong momentum for valuation recovery. Over the past year, while the valuation gap between U.S. and non-U.S. markets has narrowed, it remains high. Deutsche Bank data shows that the P/E premium for U.S. stocks once reached 70%; although it has since pulled back, it remains at an absolute high of 40%, meaning there is still significant room for valuation recovery in non-U.S. markets.

A more critical turning point comes from a reversal in earnings fundamentals—a shift with significant implications. "The earnings narrative for non-U.S. markets is finally starting to turn favorable."

"For 15 years, earnings for non-U.S. assets essentially stagnated, while U.S. earnings nearly tripled," Tim Baker emphasized in the report. "But now, non-U.S. earnings are showing a clear upward trend—growing significantly by 14% over the past six months."

However, Deutsche Bank maintained an objective stance, noting that there is a ceiling to this convergence of valuation and earnings. The profitability of U.S. companies still far exceeds that of other regions.

Simultaneously, the market needs to be wary of a potential risk: if the record capital expenditures currently being made by U.S. companies fail to translate into expected high returns, it will directly weigh on their future earnings performance.

The latest investor survey from Bank of America Merrill Lynch shows that global investors' overweight positioning in Eurozone assets has reached a record high.

In a specific European survey, more than one-third of respondents reported holding EU stock positions above their benchmarks, up from just 9% three months ago. Meanwhile, a net 22% of respondents said they were underweight U.S. stocks, compared to just 6% at the end of 2025.

French asset manager Carmignac likened this phenomenon to the awakening of "Sleeping Beauty," suggesting that structural and cyclical factors are together driving European assets back into capital favor.

Significant capital continues to flow into European equity funds as investors seek to diversify away from the concentration risks of U.S. tech stocks while also hedging against the spillover effects of U.S. domestic political risks.

Recommended Articles