Is Palantir Stock Overvalued or Dirt Cheap? The Answer Might Blow Your Mind.

Key Points

Palantir has become a major winner of artificial intelligence (AI)-driven tailwinds over the last few years.

Palantir's valuation profile is in another league when compared to other software companies.

One billionaire Silicon Valley legend thinks most investors are overlooking a key detail when it comes to Palantir and its valuation.

- 10 stocks we like better than Palantir Technologies ›

One of the most polarizing stocks that's emerged out of the artificial intelligence (AI) revolution is data analytics darling Palantir Technologies (NASDAQ: PLTR). If you invested just a modest sum of $1,000 in Palantir on the same day that OpenAI commercially launched ChatGPT, you'd have nearly $17,400 today.

To say returns of this magnitude are abnormal would be an understatement. Palantir has ushered in a new wave of AI millionaires over the last three years. And in doing so, many who were late to the party are now parroting the same bearish talking point: Palantir is overvalued. But is that really the case?

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Let's dive into a couple of different ways to measure Palantir's valuation. From there, investors should come away with some interesting observations as they consider doubling down, selling, or finally initiating a position in the data-mining juggernaut.

Image source: Getty Images.

The traditional approach: Palantir trades at historically high valuation multiples

One of the most common ways to assess a company's valuation is to look at multiples such as price-to-sales (P/S) and price-to-earnings (P/E) and then benchmark these ratios against a set of peers as well as historical norms.

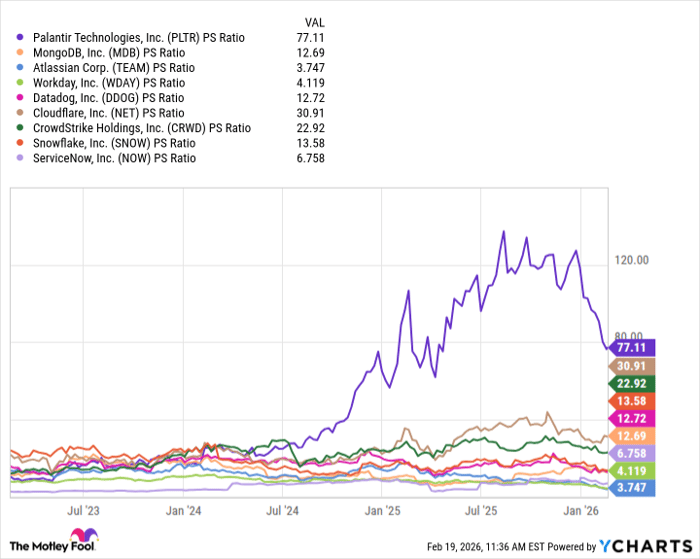

PLTR PS Ratio data by YCharts

Throughout the AI revolution, Palantir has experienced more pronounced valuation expansion than many other leading software-as-a-service (SaaS) businesses. While Palantir's revenue acceleration and profitability profile have proven more robust than many of its peers', the disparity in its valuation relative to a comprehensive set of peers in the SaaS ecosystem is nonetheless dramatic.

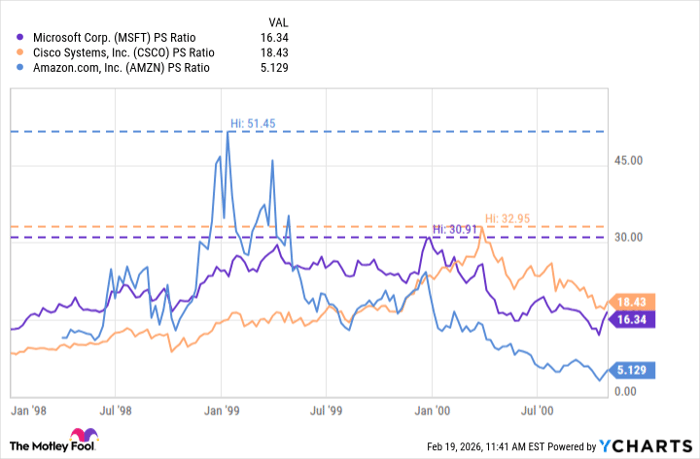

Taking this one step further, many of the internet's earliest winners experienced pronounced run-ups akin to Palantir's. During the height of the dot-com boom, Amazon, Cisco, and Microsoft witnessed peak P/S multiples in the range of roughly 30 to 50.

MSFT PS Ratio data by YCharts

Given this analysis, Palantir appears to be valued at a premium within the software market. In addition, its valuation is historically high compared to other tech-fueled rallies. Indeed, the aftermath of the dot-com bubble underscores what could be in store for Palantir's valuation profile should the AI trade come to a screeching halt.

The contrarian take: Palantir stock is dirt cheap for one key reason

If you aren't familiar, Silicon Valley legends Chamath Palihapitiya and Jason Calacanis host a weekly business podcast called All-In. Palihapitiya earned his stripes leading growth at AOL and Facebook (now Meta Platforms) in their early days, while Calacanis has long been a decorated venture capital investor.

During a recent episode, the hosts discussed Palantir and its valuation. And to my surprise, one of my prior Motley Fool articles was featured. While dissecting my analysis, Palihapitiya made an interesting, albeit quite contrarian, take: Palantir is not valued at a premium at all.

In his mind, many of the SaaS businesses in the cohort above are not true competitors to Palantir. In reality, many of these companies build basic products across customer relationship management (CRM), enterprise resource planning (ERP), people operations, or cybersecurity.

Translation: Most SaaS businesses are commoditized. As a result, many of these companies suffer from ongoing customer churn as clients migrate to similar, often cheaper, platforms upon contract renewal.

By contrast, Palantir's Artificial Intelligence Platform (AIP) -- which features its core products Foundry, Gotham, and Apollo -- are unique. Given Palantir's lack of direct competition, the company can both win important business and retain it.

Against this backdrop, Palantir boasts a higher customer lifetime value relative to a generic SaaS business. For this reason, Palantir's predictability of future revenue and durability of ongoing cash flow generation are more robust when compared to most software businesses.

In a way, Palihapitiya implies that Palantir is a monopoly. Therefore, valuing the company appropriately is almost impossible given its lack of legitimate competitive forces. When viewed through this lens, an investor could argue that Palantir's valuation is entirely justified and could continue to expand.

My opinion: Both analyses can be true at the same time

While I understand Palihapitiya's thesis, my biggest pushback is that sell-side analysts don't necessarily adopt this way of thinking. This isn't to say that Wall Street is always right, but in a way, this is probably why Palantir has such a split view -- with 40% of analysts who cover the stock giving it a "Hold" rating.

Even though Palantir is undeniably expensive by traditional standards, the stock currently trades at its steepest discount since last April amid the software bear market.

While it may appear to be trading at an unsustainable valuation, Palihapitiya's point about Palantir's lack of competition and, therefore, churn should temper fears that the company's growth could begin to slow.

With that in mind, now may be a good time to buy the dip in Palantir stock with the intention of holding for the long term.

Should you buy stock in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $409,970!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,174,241!*

Now, it’s worth noting Stock Advisor’s total average return is 889% — a market-crushing outperformance compared to 192% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 24, 2026.

Adam Spatacco has positions in Amazon, Meta Platforms, Microsoft, and Palantir Technologies. The Motley Fool has positions in and recommends Amazon, Atlassian, Cisco Systems, Cloudflare, CrowdStrike, Datadog, Meta Platforms, Microsoft, MongoDB, Palantir Technologies, ServiceNow, Snowflake, and Workday. The Motley Fool has a disclosure policy.

Recommended Articles