Shutdown Creates Jobs 'Puzzle': ADP Plunges Twice, September NFP Recovers Swiftly, But October NFP Turns Negative

TradingKey - The record-long US government shutdown is nearing its end, potentially allowing the "data-blind" Federal Reserve to access September's non-farm payrolls report as early as this week, though October's data may be permanently lost. Meanwhile, unofficial employment reports, such as those from ADP and Challenger, have already highlighted a deteriorating US labor market during the shutdown.

Although the U.S. Bureau of Labor Statistics managed to release September's CPI inflation report in late October, the Federal Reserve has endured a challenging period, lacking official employment data guidance for over 40 days during the government's halt.

Monetary policymakers have grappled with resurgent inflation alongside more concerning signs of decelerating job growth. Furthermore, Fed Chair Jerome Powell conveyed a rare hawkish stance directly addressing the prospects of a December rate cut.

Some observers suggest that the government shutdown has exacerbated internal divisions within the Federal Reserve. The necessity of relying on private surveys to assess the balance of policy risks has driven the Fed's hawkish and dovish factions to more extreme positions, while the centrist group has become more indecisive.

Hawkish officials worry that tariff-driven price increases will persist, while the dovish camp is more concerned with the evident cooling of the U.S. job market. Both sides have ample reasons to support their positions; for instance, the year-over-year CPI in September climbed to its highest level since January, while unofficial employment surveys indicate job growth has ceased, and widespread layoffs are underway.

With the U.S. government shutdown expected to conclude as early as this week, the resumption of official statistical reports may offer the Federal Reserve some relief.

Goldman Sachs anticipates the U.S. government could release the September non-farm payrolls report this Friday, November 14. Morgan Stanley, however, believes it might take until the third business day after the shutdown ends, around November 19.

Analysts believe that the Fed will ultimately receive September's employment, PCE, and retail sales data, but October's data may be "lost forever."

Kevin Hassett, Director of the White House National Economic Council, admitted that some surveys were not completed during the October government shutdown, implying that what happened in October might never be fully known.

Regardless of whether October's economic reports eventually become available, the consensus view regarding increased downside risks to U.S. employment appears to have been widely accepted.

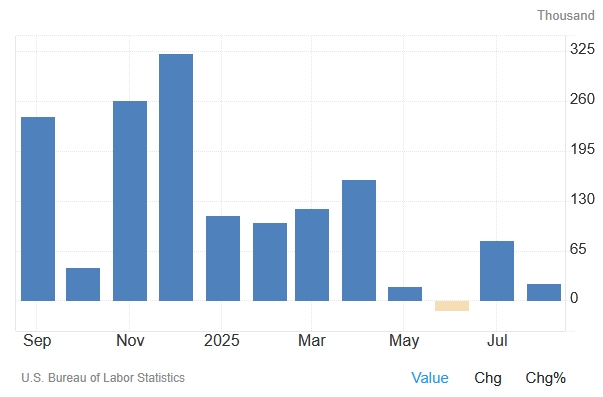

Analysts project that September's non-farm payrolls will rise to 50,000 new jobs, up from 22,000 in August. However, given that August's actual non-farm figures were significantly below the 75,000 forecast, investors should remain cautious about the reliability of the September non-farm payroll forecast.

【U.S. Non-Farm Payrolls, Source: TradingEconomics】

October, with its even murkier employment situation, is the market's primary concern. Data from ADP showed that the private sector unexpectedly shed 32,000 jobs in September, marking the largest decline since March 2023. Furthermore, the private sector issued another employment warning in October, with an additional 45,000 jobs lost that month.

According to Challenger, Gray & Christmas data, U.S. employers announced a 175% surge in layoffs in October to 153,074 people, an 183% month-over-month increase, marking the "worst October" since 2003. Cost-cutting measures and the widespread adoption of AI technology were cited as key factors driving these corporate layoffs.

Andrew Chamberlain, Chief Economist at Gusto, stated that while this is not a crisis, it is a clear signal that sustained high interest rates, tariff uncertainties, and rising costs are finally forcing even the most resilient corners of the economy to hit the brakes. The fact that small businesses, which mostly added jobs earlier this year, are now cutting staff indicates that economic headwinds are no longer theoretical but are genuinely impacting corporate hiring.

With the groundwork laid by unofficial employment data, analysts have lowered their psychological expectations for "resilient job growth." Goldman Sachs now anticipates that U.S. non-farm payrolls for October could turn negative, shrinking by 50,000 jobs, similar to what occurred in June this year.

Goldman Sachs explained that this forecast considers two factors: on one hand, the bank expects job additions to slow from 85,000 in September to 50,000 in October; on the other hand, the government's delayed exit plan could lead to the elimination of 100,000 positions.

Morgan Stanley projects that September non-farm payrolls will increase by 50,000, with the unemployment rate holding at 4.3%.

However, the firm expects the unemployment rate to rise to 4.5% in October and November, suggesting that a cooling labor market will prompt the Federal Reserve to cut rates by 25 basis points in December, despite the Fed's current wavering stance.

Recommended Articles