European Stocks Open Lower Friday, Geopolitical Conflict and Economic Outlook Become Suppressing Factors

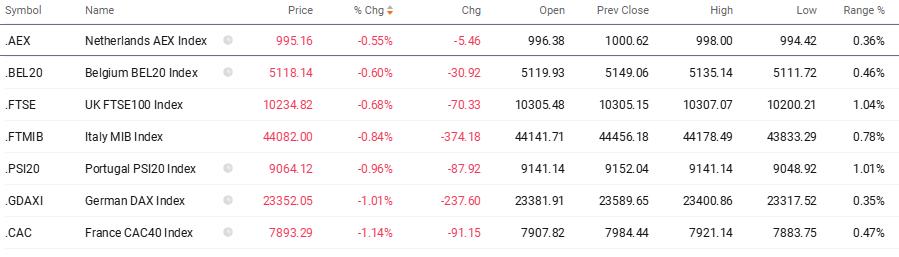

TradingKey - At 8:30 a.m. London time, the UK's FTSE 100 index opened 0.68% lower, France's CAC 40 fell 1.14%, Germany's DAX 30 dropped 1.01%, and Italy's FTSE MIB index decreased by 0.84%. During Thursday's session, the Stoxx Europe 600 index closed down about 0.7%, marking the second consecutive day of pressure for European equities.

On Friday, the final trading day of the week for European markets, major stock indices opened lower across the board as investors continued to evaluate the potential long-term impact of the escalating Middle East conflict on global economic growth.

Meanwhile, the latest UK GDP data for January revealed that the economy has entered a state of zero growth, further intensifying market concerns regarding the prospects for an economic recovery in Europe.

Driven by rising energy prices, German government bonds fell across the board, and money market bets on European Central Bank interest rate hikes next year gained further momentum.

Traders now expect the European Central Bank to increase interest rates by an additional 3 basis points by 2027, with a cumulative 52 basis points of monetary policy tightening anticipated by mid-next year; interest rate swaps show that market expectations for a 47-basis-point hike by year-end remain consistent with Thursday.

After a week of global market volatility, energy price movements remain the core focus for investors. The U.S. announced a 30-day temporary waiver on Friday, permitting sea transport of sanctioned Russian oil, intended to mitigate market panic over crude supply shortages and price spikes.

Despite the International Energy Agency (IEA) announcing on Wednesday a record release of 400 million barrels of oil from emergency reserves, and the U.S. Department of Energy's earlier plan to release 172 million barrels from the Strategic Petroleum Reserve, Brent crude prices remain above $100 per barrel.

Recommended Articles