Whale Research Analysis: Circle’s 3 Key Drivers in the Digital Asset Market

Beneath the revenue beat, Circle’s reserve-driven earnings remain intact and USDC scale has proven resilient to crypto price volatility, yet the emerging regulatory risk around reserve income sharing casts new uncertainty over its critical Coinbase distribution partnership.

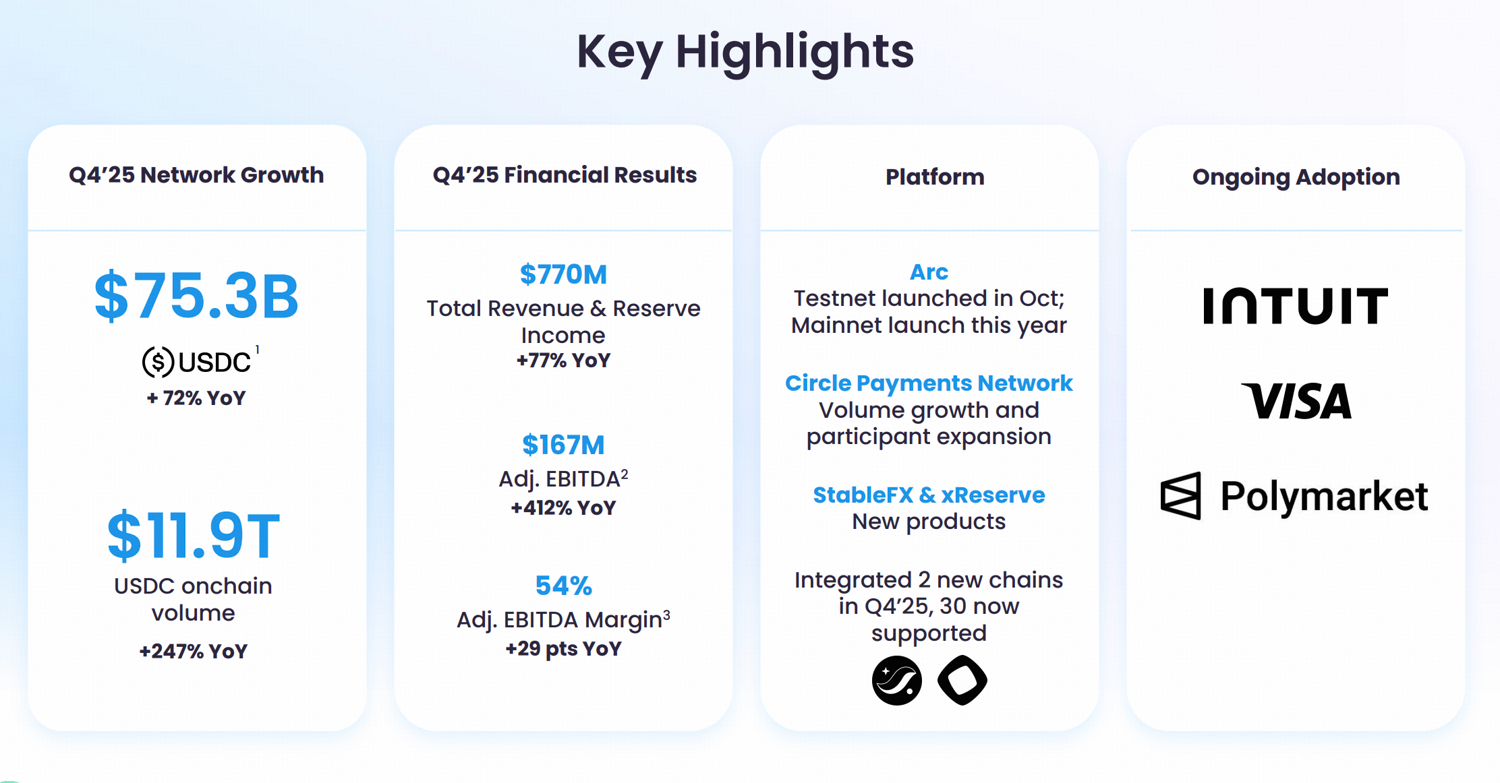

In Q4 2025, Circle reported total revenue and reserve income of $770 million and ended the year with $75.3 billion USDC in circulation, up 72% year over year. With the results beating expectations, the stock reaction was immediate.

The deeper investment takeaway sits beneath the headline revenue beat.

- Circle’s earnings model can be framed as “rate + USDC scale + distribution economics”, though the company is trying to reposition itself toward payment infrastructure and application-layer revenue streams.

- Despite an almost 50% decline in Bitcoin’s price and the broader crypto market weakness, total stablecoin supply remained stable, a dynamic not seen in prior crypto bear market. Stablecoins have decoupled from crypto market price volatility, making the “scale” component in Circle’s business model less of a concern.

- The real uncertainty now lies in distribution economics. Recent OCC interpretations tied to the GENIUS Act raise questions about whether exchange-based reward structures linked to USDC could be viewed as impermissible yield pass-through. If regulators constrain how reserve income can be shared through distribution partners, the long-standing Circle–Coinbase commercial arrangement may face pressure.

Brief Q4 Snapshot & Circle’s Earning Model

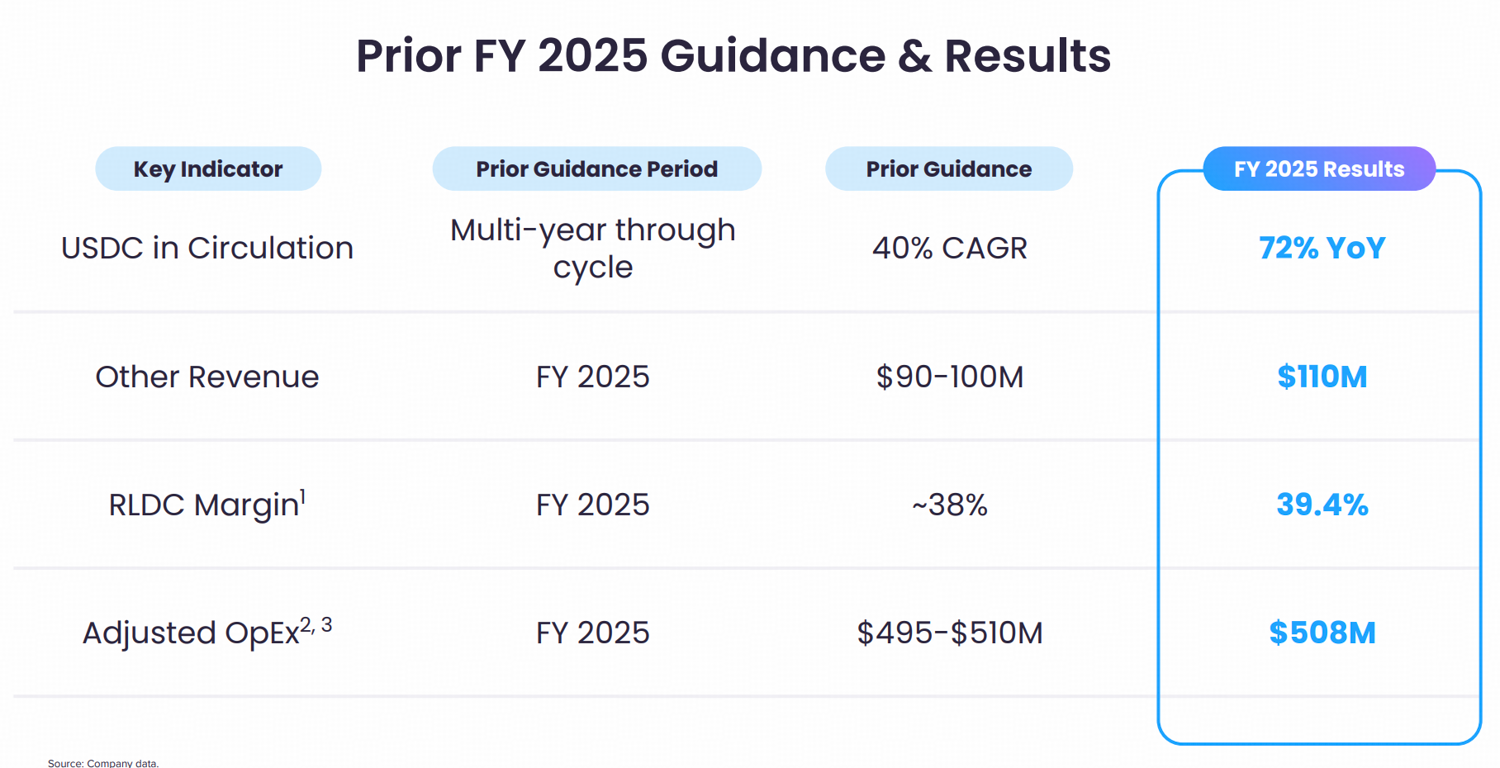

Circle’s Q4 2025 press release reported USDC in circulation of $75.3 billion at year-end and total revenue and reserve income of $770 million. Management also reiterated KPI guidance calling for a multi-year, through-cycle 40% CAGR in USDC in circulation.

Two details about Circle’s business model stand out:

First, Circle’s revenue engine remains largely reserve-income driven. The company disclosed reserve income of $733 million in Q4 (up 69% YoY), alongside a “reserve return rate” of 3.8% (down 68 bps YoY). The expansion in USDC circulation has more than offset the decline in interest rates earned on those reserves.

Second, Circle’s distribution, transaction, and other costs were $461 million in Q4 (up 52%), indicating that USDC distribution continues to rely heavily on partnerships, particularly the arrangement with Coinbase.

Circle’s core business model can be framed as “rate + USDC scale + distribution economics.” Interest rates affect reserve yield, the scale of USDC drives the reserve base, and distribution economics determine revenue-sharing arrangements with partners.

The company is expanding its product mix into payment infrastructure and blockchain applications, reducing reliance on reserve yield and exchange-driven distribution. “Other revenue” from non-reserve sources reached $110 million in 2025 (above guidance).

Core products in this category include the Circle Payment Network, a near-instant, stablecoin-powered global transfer system licensed in 55 jurisdictions (e.g., U.S. money transmitter licenses, EU MiCA compliance); Arc Blockchain, an enterprise Layer-1 chain for programmable money and real-world applications; and developer tools such as the Cross-Chain Transfer Protocol (CCTP).

While reserve income still dominates revenue, the growth of infrastructure revenue supports a business model transformation narrative for Circle.

Stablecoin Decoupled from Crypto Market Price Fluctuation

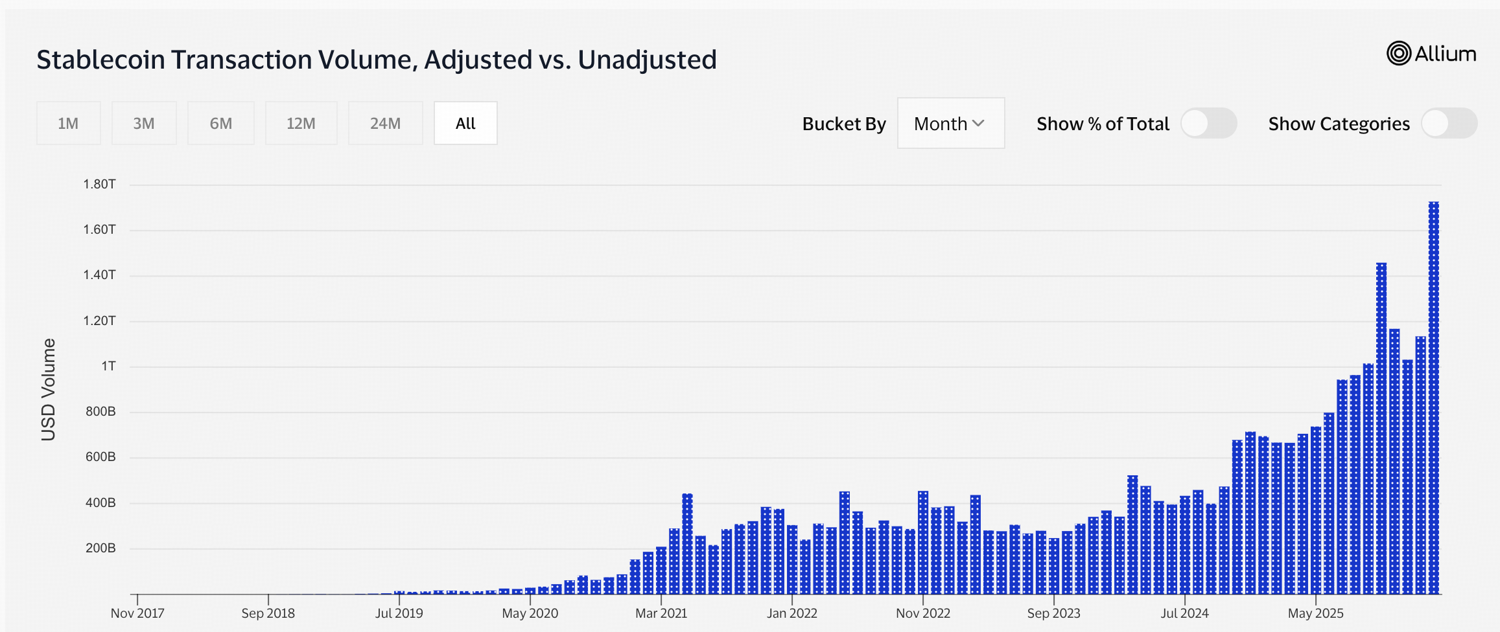

Despite Bitcoin’s almost 50% drawdown from its late-2025 peak, total stablecoin supply has remained relatively stablecoin, with almost no contraction during the sell-off. Defillama shows total stablecoins market cap of about $310 billion, which is still at a historically high level.

According to data from Visa, total stablecoin transaction volume even hit a new all time high in Feb 2026, recorded $1.73 trillion, amid a deep crypto bear market with Fear and Greed index printing extreme fear.

Source: https://visaonchainanalytics.com/transactions

Source: https://visaonchainanalytics.com/transactions

This differs from earlier cycles, where comparable drawdowns were often accompanied by significant stablecoin redemptions, depegging incidents, and observable capital outflows from the crypto ecosystem.

Several structural factors may explain this divergence.

By 2026, stablecoins serve a broader role within digital finance. Beyond functioning as trading pairs for crypto trading, they are increasingly used for cross-border settlement, on-chain payments, treasury management. This expanded utility reduces the direct link between speculative risk appetite and aggregate stablecoin supply.

Additionally, market infrastructure has matured. Improved reserve transparency, stronger issuer oversight, and greater integration with traditional financial rails have reduced the probability of disorderly redemption during volatility.

The key business linkage here is that stablecoin supply and usage resilience translate into a more stable reserve base, and reserve assets are the engine of Circle’s reserve income. As stablecoin supply decoupled from crypto market volatility, Circle’s earnings also decoupled from crypto market price volatility. However, the price of Circle’s stock continues to exhibit high-beta behavior relative to the crypto market, trading more like a speculative proxy than a reflection of its maturing fundamentals. Over time, as stablecoin adoption deepens, this mismatch could resolve, potentially leading to a re-rating of Circle’s stock.

Distribution Economics and Regulatory Risk

The most important risk factor facing Circle lies in distribution economics, specifically regulatory clarification on yield sharing.

An emerging regulatory tension centers on how reserve income linked to stablecoin can be distributed. The U.S. Office of the Comptroller of the Currency recently signaled a restrictive interpretation of the GENIUS Act’s prohibition on interest payments tied to stablecoins. If finalized in its current form, this interpretation could limit arrangements where reserve income indirectly funds user rewards programs. That directly affects the current commercial relationship between Circle and Coinbase.

The GENIUS Act prohibits stablecoin issuers from paying interest tied to stablecoins. Until now, much of the industry operated under the assumption that this prohibition applied only to issuers directly paying yield. The new OCC proposal challenges this interpretation.

It stated that close financial ties between issuers and crypto platforms handling their tokens “would make it highly likely” that yield is being passed to holders indirectly through an intermediary. In practice, if an issuer shares reserve income with a distribution partner, and that partner offers rewards tied to stablecoin balance, regulators may assume this arrangement constitutes prohibited yield pass-through.Right now, a significant portion of the reserve income of Circle is shared with Coinbase under their distribution arrangement, which incentivizes Coinbase to promote USDC and offer rewards to users. This arrangement is important to Circle, as USDC circulation benefits from Coinbase’s retail and institutional customer base.

Under the new OCC framework, such arrangements could fall under scrutiny. If regulators view exchange-based reward programs as economically linked to issuer reserve income, the current distribution structure may face challenge.

From an investor perspective, the impact flows directly into the “distribution economics” component of Circle’s earnings framework, which determines how effectively USDC is promoted through exchange channels. Exchanges remain the most important distribution channel today, even as the company works to diversify into other channels.

Bottom Line

The rate environment remains cyclical, and the USDC scale has shown greater structural resilience during the current crypto market weakness. The primary forward uncertainty now lies in distribution economics.

Until the OCC finalizes its rule and legislative negotiations clarify the treatment of third-party rewards, the Circle-Coinbase distribution structure represents the largest risk factor in Circle’s short-to-medium earning profile.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

Recommended Articles