Should You Buy the Dip on Broadcom Stock?

Key Points

Broadcom's custom AI chip business is growing at an accelerating pace.

The stock had gotten pricey ahead of its fiscal Q2 earnings report.

- 10 stocks we like better than Broadcom ›

Broadcom (NASDAQ: AVGO) was one of the better-performing artificial intelligence (AI) stocks of 2026, up by almost 40% year to date -- until June 3, when it reported its fiscal Q2 earnings. Following that report, Broadcom's stock heavily sold off and is down nearly 20% from its all-time high. While it's still in positive territory for the year, it has suffered a major reversal.

Was what Broadcom said really that bad? Or is there another force at play here?

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Broadcom's new business unit looks like it's in solid shape

Broadcom is really a tale of two companies. Broadcom's legacy core business consisted of various software products, along with some computing hardware. However, the part of the operation most investors focus on today is its AI business.

Broadcom's AI exposure comes mostly from two product lines: connectivity switches and custom AI chips. These products are in major demand, and that demand is only continuing to grow. In its fiscal Q2, which ended May 3, AI semiconductor revenue rose 143% year over year to $10.8 billion. In Q3, management expects AI semiconductor revenue to rise 200% year over year to $16 billion. That's significant momentum, and management said expects to see this growth continue into 2027 when it expects this business unit alone to deliver $100 billion or more in annual revenue.

However, that was the same guidance it gave last quarter, and the market wanted more because the stock was priced for more.

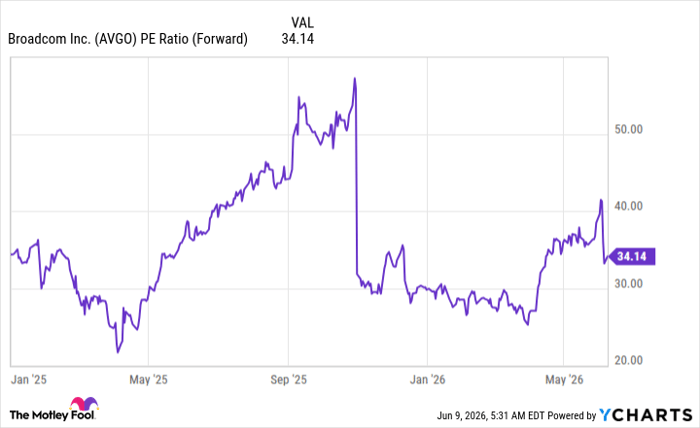

AVGO PE Ratio (Forward) data by YCharts.

Ahead of the Q2 report, Broadcom was trading at about 40 times forward expected earnings. Considering that its overall growth rate was 48% for the quarter, that's a pretty pricey valuation. After the sell-off, Broadcom trades for about 20 times 2027 earnings estimates, which isn't terribly expensive, but it's also far from cheap.

There are still a lot of expectations baked into Broadcom's stock, and if it doesn't continuously set the bar higher, it's going to sell off further following subsequent earnings reports. But I still think that the current price point offers a buying opportunity.

The reality is that there is plenty of growth ahead for Broadcom beyond 2027, as the AI data center build-out is widely projected to last through 2030. There's still plenty of time to make a ton of money selling custom AI chips between now and then. As a result, I think Broadcom is an OK buy right now, but investors will need to continue monitoring it to see if expectations pick up over the next few quarters.

Should you buy stock in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $439,038!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,277,804!*

Now, it’s worth noting Stock Advisor’s total average return is 942% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 10, 2026.

Keithen Drury has positions in Broadcom. The Motley Fool has positions in and recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles