Nvidia Q1 Revenue Surges 85%, Data Center Business Accounts for 90%, Blowout Results Fail to Stop Stock Volatility

- Iran Situation Rekindles Threat of War. Bitcoin Price Decline Accelerates, $75,000 Geopolitical Defense Line Faces Test

- WTI declines below $102.00 after Trump says he called off Iran attacks

- Gold falls below $4,500 on rising global rate hike bets

- Gold edges higher to near $4,700 as Trump-Xi summit looms

- Nvidia Earnings Approach: Can It Drive a Nasdaq Rebound? What Should Investors Watch Most?

- Euro softens to near 1.1600 on US–Iran tensions

TradingKey - As the absolute leader in the global AI industry chain, NVIDIA ( NVDA) delivered a quarterly earnings report that surpassed Wall Street's general expectations as anticipated.

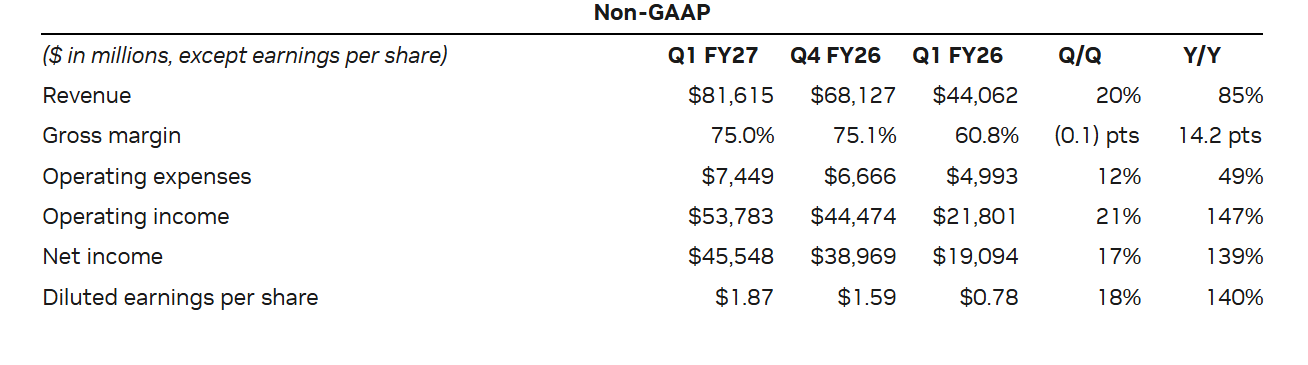

After the market close on Wednesday, May 20, Eastern Time, NVIDIA disclosed its first-quarter results for fiscal year 2027, ending April 26, 2026. Total revenue increased 85% year-over-year to $81.62 billion, exceeding analyst expectations by nearly 3.1%. Revenue from the core data center business reached $75.2 billion, contributing over 90% of the company's revenue. Both metrics set new single-quarter records, further confirming that demand for AI computing power remains its core growth engine.

Profitability was equally strong, with non-GAAP adjusted earnings per share (EPS) surging 140% year-over-year to $1.87, representing a significant acceleration in sequential growth and beating analyst expectations by approximately 6.3%. On the same basis, the gross margin for the quarter was 75.0%, which, although slightly lower than the 18-month high set in the previous quarter, remained above the market expectation of 74.5%.

Following the release of the earnings report, NVIDIA's stock price experienced significant volatility in after-hours trading, initially rising over 1% before plunging more than 3%, and finally ending down 1.28%.

In fact, this situation where 'earnings exceed expectations yet the stock price retreats' is not a first for NVIDIA. Looking back at the first trading day after the last five earnings reports, the company's stock price has fallen on four occasions.

Data center revenue surged 92%

In the first quarter, NVIDIA's Data Center revenue reached $75.2 billion, surging 92% year-over-year. This not only nearly doubled from the $39.11 billion recorded in the same period last year but also exceeded Wall Street analysts' expectations of $73.47 billion by approximately 2.3%, while surpassing the historical record set in the previous quarter by 21%.

This segment now accounts for 92% of total revenue, which means NVIDIA has become a company highly dependent on AI data center capital expenditures.

These figures clearly signal that global AI infrastructure investment continues to heat up, as AI training and inference demand from cloud service providers and enterprise customers continues to drive sales of NVIDIA's high-end GPUs, networking products, and complete data center solutions. As long as the AI capital expenditure cycle does not see a significant cooldown, the resilience of NVIDIA's core revenue will remain supported.

However, the over-concentration of the revenue structure also harbors hidden concerns. When a single business unit accounts for over 90% of revenue, investors become extremely sensitive to any marginal changes. Even if the $75.2 billion in revenue exceeded expectations, the stock price could still fluctuate due to 'sell-the-news' dynamics if the growth rate fails to meet the market's previous optimistic forecasts.

From a segment perspective, based on the previous reporting framework, Data Center Compute revenue grew 77% year-over-year to $60.4 billion—a record high, yet slightly below the $61.1 billion expected by analysts. Meanwhile, Data Center Networking performed exceptionally well, with revenue skyrocketing 199% year-over-year to $14.8 billion, also hitting a new historical peak.

NVIDIA CFO Colette Kress revealed that hyperscale data center customers contributed half of the department's revenue in the first quarter, with the remaining share coming from diverse channels such as AI cloud, industrial, enterprise, and sovereign customers.

She noted that the construction of AI factories is currently accelerating and the infrastructure value for chipmakers continues to climb. Since the beginning of this year, rental prices for the H100 have risen by 20%, while cloud service pricing for the A100 has increased by nearly 15%. Many customers are generating returns by extracting value beyond the residual useful life of their GPUs.

Furthermore, Kress disclosed that the company's newly launched Vera CPU is expected to open a new $200 billion market opportunity for NVIDIA. All leading hyperscalers and system manufacturers are currently collaborating on the processor's deployment, with total CPU revenue projected to reach $20 billion this year.

Performance Guidance Under Geopolitical Constraints

NVIDIA's revenue outlook for the second quarter of fiscal 2027 shows a median forecast of $91 billion, plus or minus 2%, implying a range of $89.18 billion to $92.82 billion; while this exceeds the analyst consensus of $87 billion, it has yet to reach the market's most optimistic projection of $96 billion.

Non-GAAP gross margin is expected to be 75.0%, plus or minus 50 basis points, representing a range of 74.5% to 75.5%.

Notably, this guidance does not include data center computing revenue from the Chinese market, which makes the second-quarter outlook appear even more robust.

NVIDIA’s explicit exclusion of China revenue from its guidance stems, on one hand, from a conservative approach to uncertainty; against the backdrop of ongoing export controls, product compliance requirements, and geopolitical risks, omitting China data center revenue effectively mitigates the risk of missing expectations. On the other hand, it highlights the strength of overseas demand—even without the Chinese market's contribution, NVIDIA remains confident in achieving revenue significantly above market expectations, while any marginal improvement in China-related business could provide additional upside.

However, the Chinese market remains a critical focal point that NVIDIA cannot ignore. In an interview, NVIDIA CEO Jensen Huang admitted that while demand in China is massive, the company has effectively ceded this market to local competitors.

He noted that Huawei achieved record performance last year and is likely to continue its strong momentum over the coming year; its domestic chip ecosystem is developing rapidly, a situation directly linked to NVIDIA’s withdrawal from the Chinese market due to export restrictions.

Notably, the Chinese market once contributed at least one-fifth of NVIDIA’s data center revenue, but since the Trump administration required licenses for chip exports to regions including China, the company has effectively been shut out of this core market.

Despite this, Huang hinted that NVIDIA has not abandoned the Chinese market and remains eager to return once the external environment improves. He emphasized that NVIDIA has numerous customers and partners in China, has deep roots in the local market for 30 years, and is very willing to serve the region.

It is worth mentioning that Jensen Huang made a last-minute appearance at President Trump’s China summit last week, but the meeting did not clarify whether NVIDIA’s H200 chip would receive a license for the Chinese market.

Enhance shareholder returns

Nvidia's board of directors has approved an additional $80 billion share repurchase authorization and significantly raised its quarterly cash dividend from $0.01 to $0.25 per share, a 24-fold increase, with the new dividend to be paid on June 26, 2026, to shareholders of record as of June 4.

In the recently concluded first quarter of fiscal 2027, Nvidia returned a record $20 billion to shareholders via buybacks and dividends; by the end of the quarter, $38.5 billion remained available under its existing repurchase plan.

The additional $80 billion buyback, along with the significant dividend hike, not only aligns Nvidia's shareholder return mechanism with those of other Big Tech companies but also, as market analysts suggest, meets investor expectations for enhanced cash returns and is expected to attract new investors.

Angelo Zino, Senior Vice President at CFRA Research, noted in an interview that as the company's future growth rate gradually slows, increasing shareholder returns will become a key strategic direction for Nvidia, particularly as it reduces external investments to return more capital to shareholders, which remains an attractive opportunity for current investors.

Nvidia Updates Financial Reporting Structure

Furthermore, Nvidia announced a transition to a new financial reporting disclosure framework designed to more accurately align with current and future growth drivers, helping investors more clearly understand the company's business landscape. This adjustment consolidates the previous multi-segment classification model into two core market platforms: Data Center and Edge Computing.

Under the new framework, the Data Center platform will be divided into two sub-segments: Hyperscale and ACIE. The Hyperscale segment covers revenue from public cloud service providers and leading global consumer internet companies, while the ACIE segment focuses on AI cloud, industrial, and enterprise application scenarios, highlighting Nvidia's growth potential in the construction of AI data centers and "AI factories" across various global industries.

The Edge Computing platform covers various end-point data processing devices supporting Agentic AI and Physical AI, specifically including PCs, gaming consoles, workstations, AI-RAN base stations, robotics, and automotive systems.

Such framework adjustments often trigger short-term trading noise during the initial stages of an earnings release. Particularly for a company like Nvidia, which is closely watched by quantitative funds, options capital, and high-frequency traders, after-hours trading typically reacts to headline figures first before repricing based on the earnings call and report details. This is one reason why Nvidia's stock price experienced significant after-hours volatility following this earnings release.

For long-term investors, however, the reporting framework adjustment does not change the company's fundamentals; it merely impacts the comparability of short-term earnings models. Analysts will need to reorganize business line classifications and historical data compatibility, and determine which metrics under the new framework better reflect Nvidia's core growth momentum.

Jensen Huang explained during the earnings call that the primary intention behind this adjustment is to help investors better understand the company's business: "We want you to have a better understanding of our business. AI is very diverse, and computing is also diverse."

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.