Precious Metal Prices at a Crossroads, Growth Engine Is Cooling: Is the Gold and Silver Bull Market Entering a Turning Point?

TradingKey - Recently Gold prices (XAUUSD) and silver prices (XAGUSD) have experienced sharp volatility amid a complex interplay of macroeconomic and geopolitical variables. Gold quickly pulled back after reaching a periodic high, while silver faced synchronized pressure. This sharp reversal in price action has rapidly fueled discussions on whether the bull market has peaked.

Bloomberg's Chief Commodity Strategist Mike McGlone stated in a recent analysis that this gold bull market may be nearing its end, suggesting that the recent highs could represent a cyclical peak for the next several years.

Reflecting on the starting point of this rally, since the 2020 pandemic shock, major global central banks implemented extraordinary easing policies. Real interest rates remained in negative territory for an extended period, and liquidity established a solid floor for gold.

Subsequently, the Russia-Ukraine conflict and ongoing global geopolitical risks continued to simmer, strengthening gold's dual attributes as both a safe haven and an inflation hedge, which significantly boosted its asset allocation profile. During this phase, gold evolved from a short-term hedge against risk events into a core defensive asset within cross-asset portfolios.

However, unlike the past few years, the current macroeconomic environment is undergoing structural changes. Although the U.S. has entered an expected phase of a rate-cut cycle, the magnitude of easing for the year is being repriced.

It should be emphasized that falling interest rates do not automatically mean gold prices will necessarily continue their upward trend. If rate cuts are accompanied by sustained economic resilience and real rates do not decline significantly, gold's 'interest rate dividend' will not be fully realized as the market expects.

Recently, geopolitical variables have increasingly become potential turning points.

Recent military actions by the U.S. and Israel against Iran have rapidly driven up the geopolitical risk premium in the Middle East, providing gold and silver with periodic buying support. However, if the situation evolves toward regime change in Iran, or a Venezuela-style political softening and restoration of international relations, the geopolitical uncertainty that has pushed gold prices higher over the past few years could cool significantly.

Once this risk premium dissipates, the safe-haven premium embedded in gold will face systematic retracement pressure.

A second, deeper variable lies in the structural strengthening of the U.S. dollar system. The U.S. has long maintained strategic dominance in the Middle East. If it further consolidates its influence over energy—particularly within the crude oil supply chain and settlement systems—during a regional restructuring, it will reinforce the dollar's central role in global energy trade.

If the U.S. dominance in the Middle East's energy and security architecture is further solidified, it will strengthen the structural linkage between energy pricing power, the dollar settlement system, and military security guarantees. Within a framework where precious metals are priced in dollars, a structural rebound in the U.S. Dollar Index itself exerts downward pressure on gold and silver.

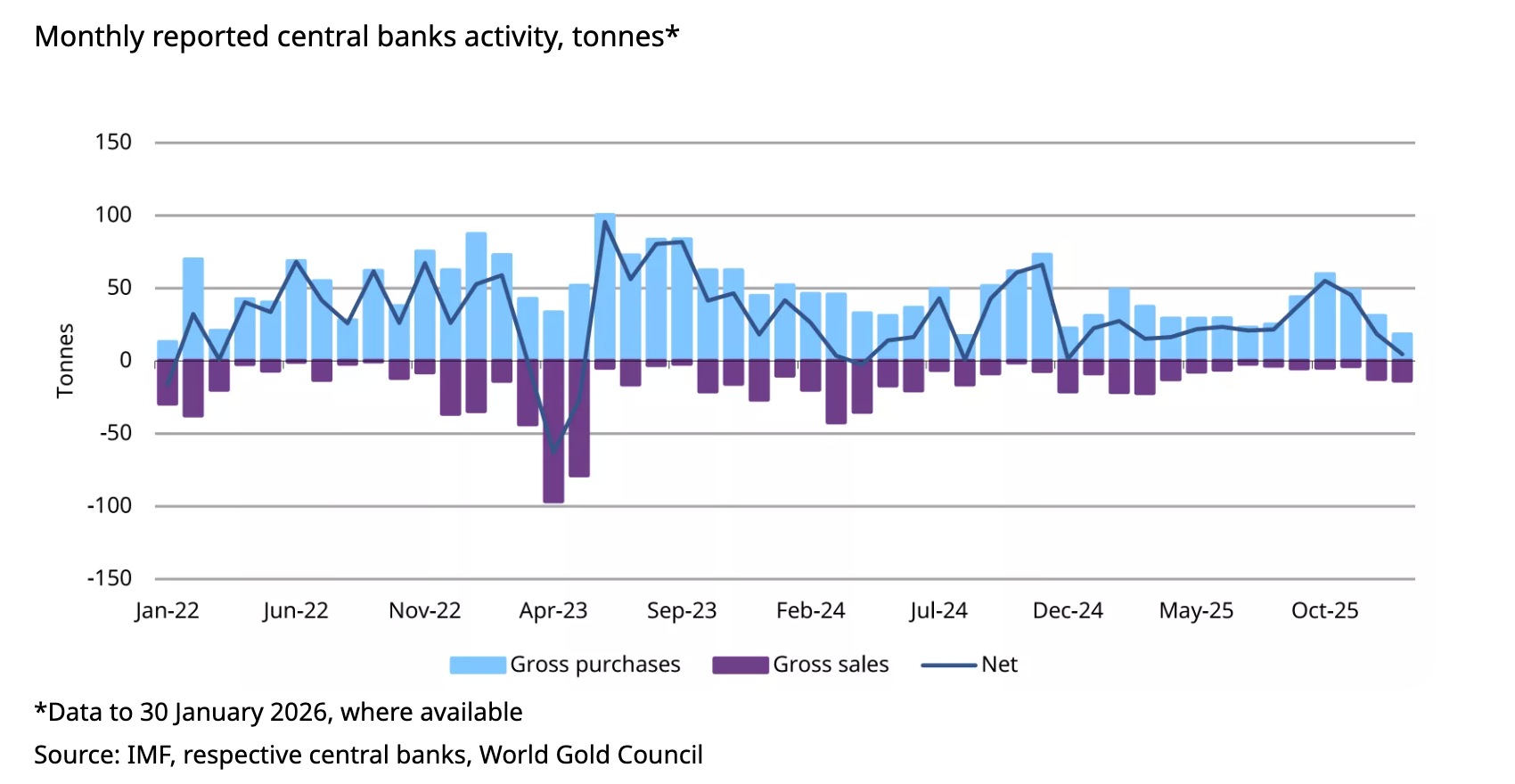

It is worth noting that some European institutions have reduced their gold ETF positions during the recent high-price phase. Regarding national gold reserves, while Asian central banks continue to increase their holdings, the pace of growth has slowed in recent quarters. This structural shift implies that global allocation forces may no longer be moving in a one-sided consensus.

Compared to gold, silver possesses industrial attributes and is more sensitive to fluctuations in the new energy and manufacturing sectors. Once the global manufacturing cycle experiences a downturn, uncertainty on the industrial demand side will amplify silver's price volatility, causing it to exhibit higher beta and faster retracement speeds during the late stages of a bull market.

From a historical cycle perspective, bull markets in precious metals often do not end with a reversal in a single variable, but rather reach a trend inflection point when a rise in real rates, a stronger dollar, and a fading risk premium converge.

The current market has not yet fully met this combination of conditions, but some prerequisites are gradually taking shape. Especially if Middle East tensions ease, U.S. strategic positioning strengthens, and the dollar system gains additional support, the risk premium accumulated by gold over many years could shrink rapidly.

For investors, the real focus should not be on short-term price pullbacks, but on whether geopolitical risks persist, how the structural strength of the dollar evolves, and whether central bank allocation behavior undergoes a sustained reversal.

Recommended Articles