Pound Sterling coils while the BoE and Fed freeze in lockstep

- With both central banks frozen in near-identical hawkish-hold postures, the rate gap that usually drives Cable has flatlined.

- The result is a Pound coiling ever tighter inside its converging daily EMAs.

- The next real move is almost certainly US-made with the data calendar lopsided toward Thursday's inflation print.

Cable looks dead this week, and that is not an accident. The Bank of England (BoE) and the Federal Reserve (Fed) have quietly become the same central bank. Both are sitting on their hands, both are watching above-target inflation get shoved higher by the same Middle East oil shock, both have hawkish dissenters in the room, and both now face a market pricing the next move as a hike rather than a cut. When two policy paths line up this neatly, the interest rate differential that gives GBP/USD its direction simply stops moving, and the pair is left to grind sideways while everyone waits for one side to blink.

Two banks, one problem

It is rare to see the transatlantic policy picture this symmetrical. The BoE has held Bank Rate at 3.75% for three meetings running, with its most recent vote splitting 8 to 1 in favour of a hold and the lone dissenter pushing for a hike. UK Consumer Price Index (CPI) inflation is running at 3.3%, and the bank itself expects energy pass-through to nudge it higher still over the coming quarters. Now look across the Atlantic, and the script is almost word-for-word identical. The Fed is parked, its speakers have leaned hawkish into the week, and traders are pricing a genuine chance of a July hike that barely existed a month ago. The same surge in Oil that is testing the BoE is testing the Fed, and neither bank can do much beyond wait and see how the shock propagates. Two committees, one exogenous problem, and no appetite on either side to commit.

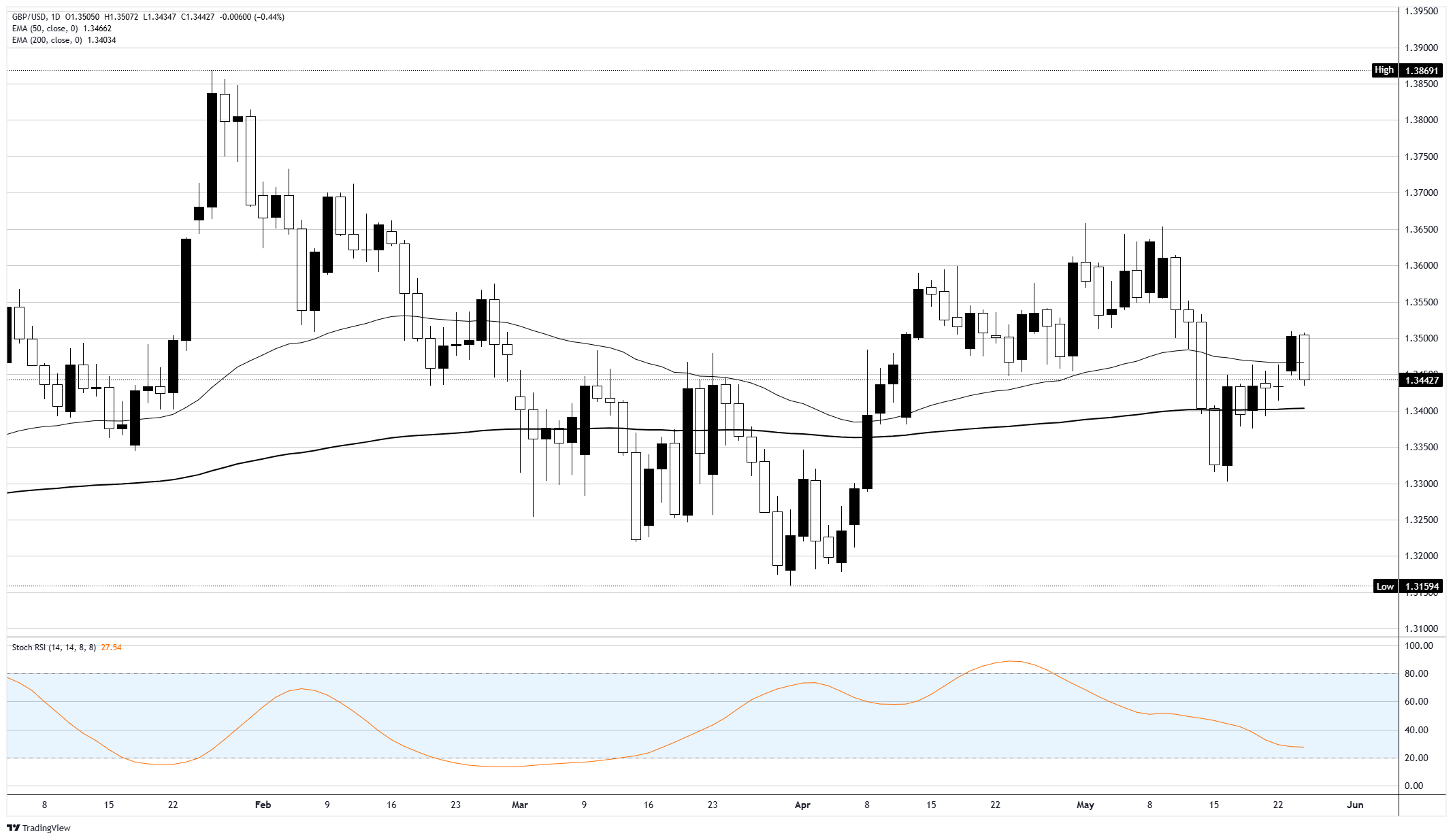

A coil, not a trend

This stalemate is written all over the chart. On the daily candlesticks, the 50 and 200-day EMAs have compressed into a tight band roughly between 1.3400 and 1.3450, with price pinned right on top of them and the broader 1.3200 to 1.3900 range that has contained the pair all year still fully intact. That kind of moving-average convergence is not noise, it is the technical fingerprint of a market with no reason to choose a direction. Momentum on the daily Stochastic RSI has rolled over toward the lower end of its range while price refuses to break, the classic signature of a coiled spring. The Pound spent Tuesday on the defensive, drifting toward the floor of its recent range before a modest late bounce, but at no point did it threaten to leave the box. This is compression, plain and simple, and compression eventually resolves with force.

The break will be made in Washington, not London

Here is the part that actually matters for positioning. The catalyst calendar is heavily lopsided toward the US. The UK has essentially nothing of substance on the docket until the next BoE decision in June, and while there is no shortage of central bank speakers this week on both sides, none of them can realistically pre-commit ahead of fresh data, so the parade of speeches is noise. The US, by contrast, delivers its Personal Consumption Expenditures Price Index (PCE) on Thursday at 12:30 GMT, the Fed's preferred inflation gauge, before rolling into its monthly data cycle. Core PCE is seen ticking up to 3.3% YoY with the headline rate expected to accelerate toward 3.8%, and a hot number would feed the hike narrative and hand the US Dollar a fresh leg. That makes the resolution of this coil overwhelmingly a dollar story, not a Pound one. The Pound is a passenger here, the dollar holds the wheel.

For now, treat the pair as range-bound while it holds inside the EMA envelope. Fade pushes toward the 1.3500 cap and buy dips toward the 1.3400 floor where the 200-day sits, but keep the size honest, the real trade is the break. A daily close below 1.3400 opens the path toward 1.3300 and ultimately the 1.3200 range floor, while a close above 1.3500 targets the 1.3600s and, further out, the top of the range near 1.3850. The medium-term play is patience, let the coil snap, then ride the breakout in whichever direction Thursday's PCE and the US data that follows dictate. Bias inside the range is neutral with a mild downside lean given the dollar's hawkish tailwind. Two frozen central banks cannot hold the spring down forever.

GBP/USD daily chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Recommended Articles