3 AI Stocks Trading at Bargain Prices After the Recent Sell-Off

Key Points

The ongoing stock market sell-off has growth investors rotating capital away from artificial intelligence (AI) stocks.

Some AI stocks boast strong revenue and profitability profiles despite what their plummeting share prices may imply.

Three members of the "Magnificent Seven" now trade for attractive valuations amid selling pressure.

- 10 stocks we like better than Nvidia ›

If there is one theme driving the stock market right now, it's uncertainty. Whether it's geopolitics, the midterm elections, possible changes in monetary policy, inflation, or unemployment, stock prices are whipsawing on just about any narrative or headline these days. Since Feb. 1, the S&P 500 and Nasdaq Composite have dropped 3.7% and 4.7%, respectively. Among the biggest laggards in the market this year are technology stocks -- particularly, the "Magnificent Seven."

While cratering stock prices tend to induce fear and panic, smart long-term-focused investors understand that times like these often present rare opportunities to buy quality businesses at steep discounts. Let's take a closer look at three leading artificial intelligence (AI) stocks that I see as no-brainer buys right now as investors continue to hit the sell button.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

1. Nvidia

Nvidia (NASDAQ: NVDA) might just be the most influential business in the AI realm. What began as a chip specialist in graphics and visuals for video games has evolved into the de facto platform on which generative AI applications are built.

Nvidia's Hopper, Blackwell, and upcoming Rubin graphics processing unit (GPU) architectures continue to be in high demand among major AI hyperscalers, including Microsoft, Amazon (NASDAQ: AMZN), Alphabet, Meta Platforms (NASDAQ: META), Oracle, and OpenAI. With an estimated 92% of the AI data center GPU market, Nvidia has been able to steadily command enormous levels of pricing power for its chipsets throughout the AI revolution.

Given these dynamics, not only has Nvidia's revenue accelerated at an impressive rate, but its profit margins continue to widen. In the fourth quarter alone, the company's data center revenue grew 75% year over year. Meanwhile, the company's gross margin expanded by 200 basis points and earnings per share (EPS) increased 98% year over year.

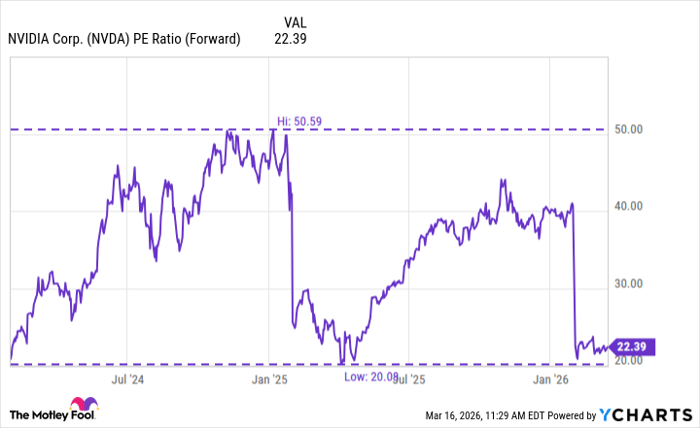

Nevertheless, Nvidia stock has struggled throughout 2026 as growth investors rotate capital away from more volatile sectors such as technology.

Data by YCharts.

Whether it's the company's ability to sell chips in a major market like China, rising competition from Advanced Micro Devices and Broadcom, or the perception that Nvidia is a one-trick pony in the semiconductor landscape, the valuation trends above could suggest that investors are beginning to view Nvidia as somewhat risky, or, at the very least, no longer positioned for explosive growth.

I see each of these risk factors as short-sighted. During the company's Q4 earnings call, management provided investors with extremely robust forward guidance figures. These financials did not include any impact from China.

Moreover, Nvidia has made several strategic investments in ancillary markets, including enterprise software, telecommunications, and other infrastructure opportunities that should pave the way for new revenue streams beyond data centers down the road.

With its forward price-to-earnings (P/E) multiple hovering near its lowest level throughout the entirety of the AI revolution -- despite a strong market position supported by ongoing secular tailwinds fueling the AI infrastructure market, in combination with new catalysts that are yet to bear fruit -- I see Nvidia stock as an absolute bargain right now.

2. Amazon

Amazon stock has been a unique case study so far in 2026. Despite reporting strong financial results for Q4 and full-year 2025, Amazon stock trades down 8.2% so far this year -- wiping out nearly $400 million in shareholder value.

The main driver behind the sell-off in Amazon stock is the company's budget for capital expenditures (capex) this year. While Wall Street was expecting around $150 billion for capex, Amazon's management shocked investors when it revealed its budget would be closer to $200 billion -- about a 51% increase over last year.

Procuring chips, designing custom silicon, and building data centers take time. So, the concern with accelerating infrastructure spend is its impact on near-term profitability. As of Q4, Amazon's trailing-12-month free cash flow declined 71% -- with the main drag being rising capex.

Image source: Amazon Investor Relations.

While I understand Wall Street's concerns, I think the degree of panic is overblown. In Q4, Amazon Web Services (AWS) -- which accounts for the majority of Amazon's operating profit -- generated its strongest growth in nearly three years.

Much of this growth can be attributed to Amazon's savvy partnership with Anthropic. As the AI start-up becomes further embedded within the broader AWS ecosystem, I am optimistic that Amazon is well on its way to building a highly profitable, vertically integrated model featuring its own chips, labor-efficient robotics in its warehouses, and blossoming cloud infrastructure in the long run.

With a P/E ratio hovering around 29, Amazon stock is trading near its cheapest valuation in a year. I think now is a great opportunity to buy the dip in Amazon as the company lays the foundation for its next chapter of AI-driven growth.

3. Meta Platforms

While Nvidia may be the most influential AI company, Meta might be the most misunderstood. Meta generates the majority of its revenue and profit through advertisements on its social media platforms: Facebook, Instagram, and WhatsApp.

Here's the problem: Online advertising is a fiercely competitive and relatively commoditized business. Meta's investments in AI have helped change that narrative, though. Over the last few years, the company's new suite of machine learning advertising tools, dubbed Advantage+, has grown into a $60 billion annual revenue run-rate business.

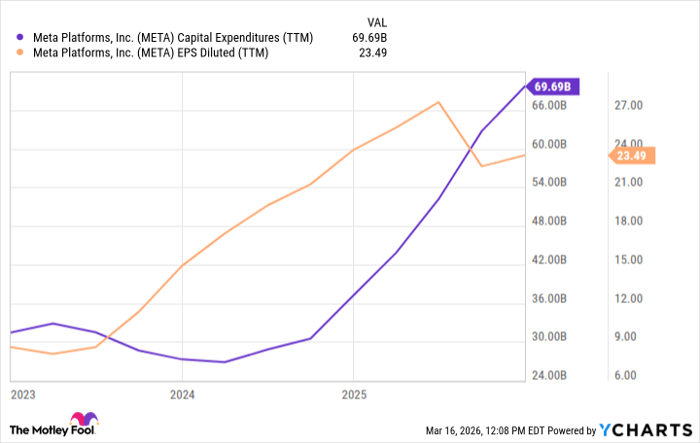

Data by YCharts.

In my eyes, investors do not fully appreciate how accretive AI has become for Meta's ecosystem. While the company's spending has risen substantially, Meta's earnings power has nearly tripled throughout the AI revolution so far.

To me, this underscores how impactful Meta Advantage+ is becoming in the world of advertising -- cementing Meta as a market leader across various consumer demographics. Despite its robust profitability profile and booming AI services business, Meta remains the cheapest Magnificent Seven stock based on its forward P/E of just 21.

I see Meta stock as an absolute steal right now and think long-term investors should buy shares hand over fist before the rest of Wall Street catches on to the company's monster potential.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $494,747!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,094,668!*

Now, it’s worth noting Stock Advisor’s total average return is 911% — a market-crushing outperformance compared to 186% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 20, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles