Own Oracle Stock? 2 Things Investors Need to Know.

Key Points

OpenAI's current challenges are negatively affecting Oracle's stock and bonds.

This raises doubts about Oracle's expansion of its data center infrastructure.

Oracle's return on invested capital has been declining over the past 25 years.

- 10 stocks we like better than Oracle ›

As tech stocks continue their sell-off, many investors have turned their attention to Oracle (NYSE: ORCL), which has seen its shares plunge more than 21% since the start of the year. Investors may wonder if now's the time to click the sell button before shares plummet even further -- or whether now could be an opportunity to buy.

To provide some insight into Oracle's current situation, two fool.com contributors take a closer look at the tech stalwart.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Oracle's stock and its bonds are coming under pressure

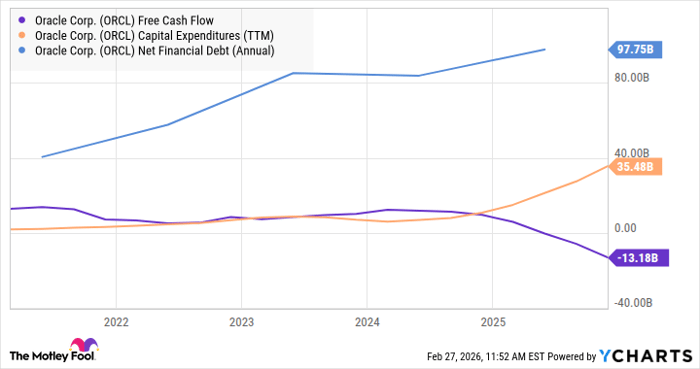

Lee Samaha: Oracle's stock has declined by more than 55% since news of its $300 billion deal with OpenAI was announced. Equity investors are growing increasingly worried about the cost of the buildout of artificial intelligence (AI) data center infrastructure for Oracle and the ability of OpenAI to raise funding and generate the necessary profitability to ensure the deal is successful for Oracle.

Those fears are exacerbated when investors look at how ballooning capital spending is leading to significant cash burn at an already indebted company.

ORCL Free Cash Flow data by YCharts

At the same time, Oracle's credit default swap (CDS) spreads jumped from around 40 basis points to 50 basis points (where 100 basis points = 1%) to an elevated level of 125 to 145 basis points. Investors buy CDSes to protect against default risk, so the higher pricing reflects the market's pricing of increased risk of its bonds defaulting. While that's not positive in itself, it's important to remember that these things are connected.

Image source: The Motley Fool.

If Oracle raises funds by issuing debt, the market is likely to require higher yields to compensate for the risk. That will negatively affect the cost of servicing the debt, and equity investors will be more negative on the stock. Similarly, a falling stock price makes it harder to raise funds by selling equity, which will negatively affect how bond investors view the company's ability to repay bonds.

Clearly, Oracle needs to convince the market that it and OpenAI can adequately fund their operations in line with their plans.

Oracle has generated declining returns on its investments

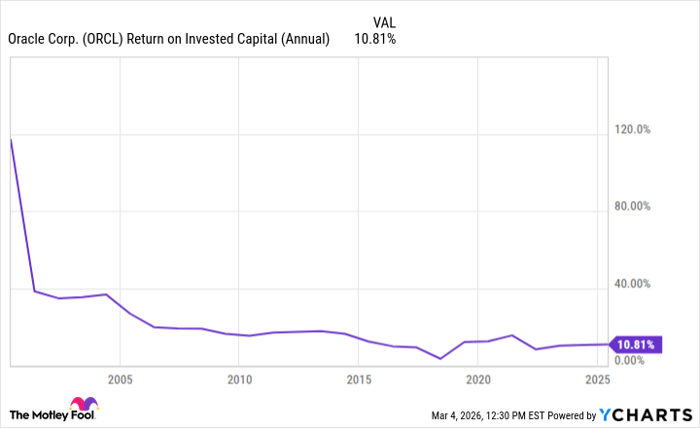

Scott Levine: Questions about the massive investments that companies are making in AI continue to grow in many investors' minds lately. This skepticism, taken in concert with the considerable capital that Oracle is deploying to build out its data center infrastructure, is contributing to much concern for Oracle shareholders.

Through the first six months of fiscal 2026, Oracle's capital expenditures (capex) totaled $16.4 billion, a significant increase over the $6.6 billion it reported in capex for the same period last year. And the heavy investments won't slow down soon. Oracle expects to raise about $50 billion in 2026 to support the development of its data center infrastructure.

While there may be greater demand for AI infrastructure, it's understandable why investors are unsure about Oracle's substantial investments, given how the company has endured declining returns on its invested capital over the past 25 years.

ORCL Return on Invested Capital (Annual) data by YCharts.

Addressing the company's capex, Ken Bond, Oracle's senior vice president for investor relations, stated on the company's second-quarter 2026 conference call, "As a reminder, the vast majority of our capex investments are for revenue-generating equipment that is going into our data centers."

On its surface, this seems like a positive, but current shareholders will want to stay acutely focused on the company's profit following the buildout of its data center infrastructure. If Oracle struggles to generate stronger profit, the company's financial health will probably be compromised as it seeks to service the huge debt stemming from the buildout.

What should Oracle investors do now?

As Oracle is a leader among cloud computing stocks, there's certainly good reason for investors to hold Oracle stock in their portfolios. Savvy investors know, however, that owning shares of Oracle, or any company for that matter, demands that they remain current with the company's dealings. It's not time to head for the exit with Oracle stock, but it's definitely time to pay especially close attention to the company's upcoming financial reporting.

Should you buy stock in Oracle right now?

Before you buy stock in Oracle, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Oracle wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $534,008!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,090,073!*

Now, it’s worth noting Stock Advisor’s total average return is 949% — a market-crushing outperformance compared to 190% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 9, 2026.

Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Oracle. The Motley Fool has a disclosure policy.

Recommended Articles