JD.com (JD) 3Q Results: Huge Investment Return Potential but Only the Patient Ones will be Rewarded

Overview

JD remains one of the few Chinese tech giants that has not experienced a significant stock rally this year. In fact, the stock price has been down 9% year-to-date. The very low valuation, combined with the strong business model and financial position, provides a solid downside protection. JD stock has a lot of upside potential, but this is only for the patient investors who are willing to endure the current negative sentiment.

Earnings Recap

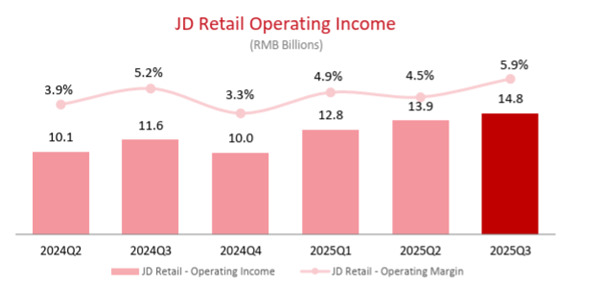

The company reported Q3 earnings before the market opened on Thursday, the 13th of November, and the stock price went down 1.7%, due to the overall market meltdown. However, there are certain encouraging signs, such as better-than-expected EPS and the JD Retail Operating Margin being up to 5.9%.

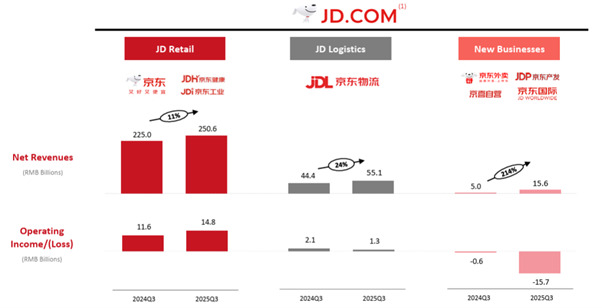

Metric | 2025Q3 Actual | 2025Q3 Estimate | 2024Q3 Actual | Beat/Miss | YoY Change |

Total Net Revenues | RMB 299.1bn | RMB 294.0bn | RMB 260.4bn | Beat | +14.9% |

Non-GAAP Diluted EPS | RMB 3.73 | RMB 2.75-2.89 | RMB 8.68 | Beat | -57.1% |

JD Retail Revenue | RMB 250.6bn | RMB 249.0bn | RMB 224.9bn | Beat | +11.4% |

JD Logistics Revenue | RMB 55.1bn | RMB 53bn | RMB 44.4bn | Beat | +24.1% |

Non-GAAP Operating Margin | 0.1% | 5.0% | 5.0% | Miss | -4.9pp |

Source: Investors’ Presentation

Source: Investors’ Presentation

JD Retail

JD Retail is the main business segment of JD. It is where e-commerce is. JD Retail business model is mostly first-party, as they hold the inventory themselves and record a gross profit from the difference between the sale and purchasing prices of a product.

However, they also have a third-party e-commerce business where they serve as a platform between buyers and sellers (just like Alibaba). This business is still relatively small (10% of the total retail revenue) but growing fast and contributing to the overall profit of the company with its high margin. Under the cap of Retail, there are also JD Health and JD Industrials - much smaller-scale businesses.

JD Retail growth was just 10.5% year-over-year due to a higher base last quarter. JD Retail is heavily driven by electronics and appliances revenue and, as we know, the national campaign of trading in old appliances was launched last year, which gave a boost to JD Retail's revenue in the recent quarters. However, as the effect of the campaign fades away, we are observing growth rates normalizing. As we see from the Q3 earnings, the appliances product line grew only 4.9% from last year.

Marketplace and general merchandise had a solid growth of 18.8% and 23.7%, respectively, each driven by: 1) investments in supply chain and 2) users acquired from the food delivery business started also spending on non-food products.

The favorable product mix (more general merchandise than appliances), as well as the effects from the supply chain optimization, were able to drive the retail margins up towards 5.9% versus 5.2% in Q3 last year. Let’s not forget that the marketplace (3P) business is also margin accretive.

Source: Investors’ Presentation

JD Logistics

Logistics is one of the defining features of JD. The well-developed logistics network is what ensures efficient delivery. JD Logistics serves the internal e-commerce operations of the firm, as well as outside clients. Unlike some competitors like Cainiao and ZTO, JD mostly owns its logistics assets, and its wide network of warehouses is perhaps the main pillar supporting its e-commerce business.

Company | Model | Company Warehouse Count (2025) | Total Floor Space (sqm) |

JD Logistics | Asset-heavy | 3,600+ (both owned and third-party) | 34+ million |

Cainiao | Asset-light | 1,100+ (global network) | 16.5 million |

SF Express | Asset-heavy | ~500-1,000 (est. hubs & facilities) | 20-30 million (est.) |

ZTO Express | Asset-light | 79 (sorting hubs) + 28,900 outlets | N/A (focus on outlets) |

In Q3, the logistics segment delivered a growth of 24% year-over-year, mostly from acquiring new customers. Other contributing factors include the optimization and technological innovation of the current logistics network, as well as the recent overseas expansion efforts.

New Businesses

New Businesses is the smallest but also the fastest-growing segment. This segment predominantly includes the food delivery business, launched earlier this year, and the delivery of non-food goods (the recently-incorporated DADA Nexus). It also includes property investments, discount stores and all the overseas operations, but these are very marginal, so we won’t talk about them.

In the traditional food delivery business model, revenue comes from the following sources:

- Delivery fees - paid by customers per order

- Merchant commission fees - where restaurants pay to be listed on the food delivery platform

- Advertising fees - extra fees paid by merchants for better visibility in the app

Currently, JD predominantly charges 0% to merchants onboarded on their platform, as part of their strategy to increase their presence in the market.

For Q3, the New Businesses growth has been up 213.7% year-over-year to nearly RMB 15.59 billion of revenue. However, as we see a very rapid growth rate in revenue, we also see massive losses of RMB 15.74 billion, mostly from subsidies and discounts given to customers – this being the main reason of the lower EPS than last year. The management is dedicated to cutting losses and making this segment profitable over the long term, as they gradually lower the incentives.

Balance Sheet and Cash Flow

Source: Investors’ Presentation

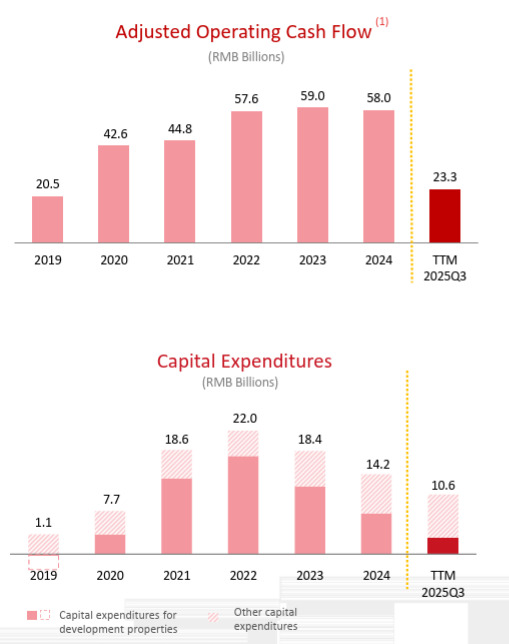

Over time, JD has proven to be a cash flow-generating machine. Even during the pandemic, the company maintained strong cash flows from operations. Currently, we see a ramp-up in capital expenditure, mostly due to the recently-launched food delivery business. However, despite the massive investments in capex, the adjusted FCF is still strictly in a positive territory.

Source: Company’s Filings

Competitive Landscape and Outlook

In the context of the involution in recent years, causing a cut-throat race-to-the-bottom, the margins of JD remained suppressed, and they also lost market share to Pinduoduo and Alibaba. Currently, JD’s market share is slightly behind Pinduoduo (~20%), but far behind Alibaba (50%).

However, there is strong evidence that JD will continue to be one of the dominant forces in the Chinese e-commerce industry and maintain market share, primarily due to the nature of its first-party model and in-house logistics capabilities that both ensure: 1) high product quality; 2) efficient delivery; 3) emphasis on logistics optimization and 4) superior user experience.

As for food delivery, currently, JD’s market share is rather small at around 5%, but that makes it third within the country. Meituan is dominating with a 65-70% market share, and Alibaba’s Ele.me is a solid second with 20-25% market share. However, JD delivery has done a great job in taking over the more premium deliveries with a 45% share there, and this has been achieved in just a year from the launch of the delivery business.

JD has a strong chance to establish a long-term presence in the country’s food delivery industry and even expand market share due to the following reasons:

● Well-established e-commerce business with over 700 million active customers that can feed the food delivery business, they also have a pre-established supermarket delivery business (DADA Nexus), implying that infrastructure does not need to be built from scratch

● Strong first-party logistics network that can assure secure and timely delivery

● Strong connection with large merchants, which will be willing to pay for higher-quality delivery service

● Strong balance sheet serving as a shield and gunpowder for longer price wars, with the highest cash-to-debt ratio among the three competitors

| Alibaba (BABA) | JD.com (JD) | Meituan (3690.HK) |

Cash & Equivalents + Short-Term Investments | RMB 416.3bn | RMB 223.4bn | RMB 188.9bn |

Total Debt | RMB 232.1bn | RMB 47.1bn | RMB 44.8bn |

Net Cash Position | RMB 184.2bn | RMB 176.3bn | RMB 144.1bn |

Cash-to-Debt Ratio | 1.79 | 4.74 | 4.21 |

*Data is from Q2

Overall, the current state of irrational competition cannot last forever, and sooner or later, the market participants will focus back on monetization and profitability expansion. Also, in this race, it is not necessary for the winner to be the only one. In many markets, there are two or more well-established delivery players. For instance, in the US, there are three - DoorDash, Uber Eats and Grubhub.

With all the above-mentioned advantages in hand, JD has a realistic chance to sustain its market share in traditional e-commerce and double its market share in the coming years. Not only that, the food delivery margin in the future will most likely be higher than the historical average of JD’s e-commerce business, lifting the profitability.

Valuation

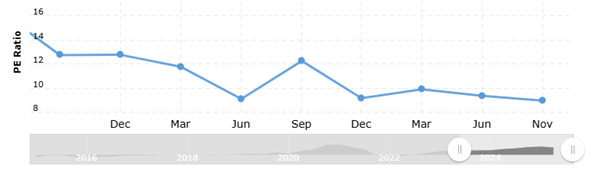

The forward PE ratio of JD is less than 9x. This is lower than the recent 2-year average of 12xPE. The current multiple of 9x is also significantly lower than peers like Alibaba (18x), Meituan (20x) and Pinduoduo (14x). We believe the market punishes JD too harshly and multiple should revert back to 12-13x, giving the stock a 30%-40% upside potential or a target price of $40-$42 per ADR.

Source: macrotrends.net

Source: macrotrends.net

Risks and Why the Price May Stay Low for Longer

Overall, JD is an established player with a well-functioning business model; however, the investment return on the stock paints a different picture. Since the IPO in 2014, the stock has increased just 58%, or 4.8% per year on average.

No Catalyst: The issue with JD is that there is no well-defined catalyst to make the price go up. For example, the catalyst for BABA was AI. JD’s approach towards AI is more low-profile, as it is mostly focused towards internal use (e.g. logistics optimization), while BABA's approach is way more holistic, encompassing cloud, language models and chips, making it more visible for investors to notice.

Continuous Price Wars: Also, the intense price wars in e-commerce and food delivery may take longer than we expect, something the market will not be happy about, because that directly suppresses margins. For instance, the new business segment, where the food delivery is, is expected to generate over RMB 40bn of operational losses, and the breakeven may take several years to happen. An extra RMB 1bn of operating losses is equal to nearly 0.1pp of margin compression.

Market Share Erosion: Another potential risk is the expected market share loss in e-commerce. In recent years, we saw platforms like Pinduoduo, focusing on providing cheaper goods, taking away market share from JD, which can be considered more of a high-end provider. If the Chinese consumer continues to be more price-sensitive, that will be bad news for JD.

Recommended Articles