Inflation Traders Fully Pivot to No-Cut Bets. Fed’s Next Rate Cut Will Be in Late 2027?

TradingKey - Market expectations for the trajectory of monetary policy are shifting significantly. According to the latest CME FedWatch data, traders have markedly scaled back short-term rate-cut bets, pivoting to a "higher-for-longer" macro narrative.

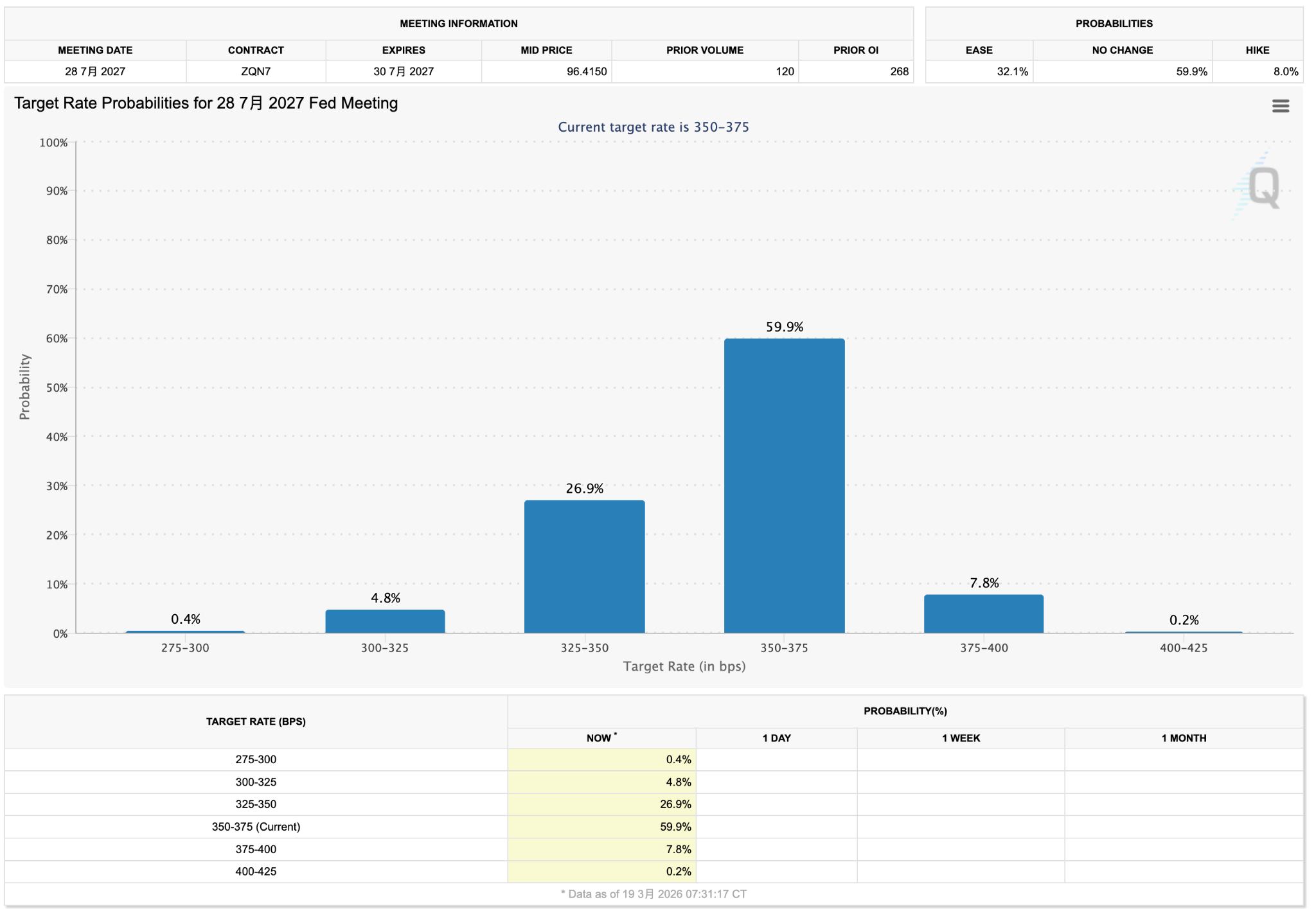

Based on current interest rate distributions, market pricing for July 2027 shows a 59.9% probability of rates remaining in the 3.50%–3.75% range. Larger rate cuts have been marginalized, indicating that the market has almost entirely abandoned bets on a rate cut within the year.

Previously, Federal Reserve Chair Jerome Powell repeatedly emphasized persistent inflation in press conferences, which the market interpreted as hawkish, dampening expectations for a rate cut this year. Based on the implied path of interest rate futures, traders generally expect the next substantive rate-cut window to be pushed back to late 2027, significantly later than the previous consensus of 2026.

The conflict in the Middle East has reinforced the inflationary stickiness driven by rising energy prices. On one hand, recent U.S. inflation data has consistently exceeded expectations, bolstering the case for persistent inflation; on the other, Middle East tensions are driving up energy costs, prompting markets to price in the risk of "secondary inflation." In this context, it is more difficult for the Fed to pivot quickly toward an accommodative policy.

Furthermore, from an asset pricing perspective, the strengthening "no-cut" expectation is reshaping market structures.

A high-rate environment means funding costs remain elevated, weighing on growth stocks and high-beta assets, while U.S. dollar assets continue to find support from yield differentials and liquidity advantages.

Recommended Articles