Think You Missed Out on Nvidia Stock? Here's Why It Could Have Room to Run.

Key Points

Nvidia is rolling out a new chip generation that could drive a revenue increase.

Nvidia's stock looks cheap compared to its peers.

- 10 stocks we like better than Nvidia ›

Since the artificial intelligence (AI) arms race kicked off in 2023, Nvidia's (NASDAQ: NVDA) stock has risen nearly 1,400%. That's a huge run that has made it the world's largest company, leaving many investors worried that they missed out on one of the biggest winners of their lifetimes.

However, I don't think that's the case. While Nvidia isn't going to deliver another 1,000% run anytime soon (it likely won't at all), I'm still confident that it can deliver strong, market-crushing returns.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

The market has tried to move on from Nvidia stock and is looking elsewhere for AI-related returns. This is premature, as Nvidia's outlook is still bright.

Image source: Getty Images.

Nvidia is still the king of AI compute

AI requires a ton of computing power to train and run. The vast majority of computing power has come from Nvidia since 2023, and that's unlikely to change due to the deep relationships Nvidia has formed and how workloads have been tailored to run on Nvidia's computing units. This keeps Nvidia in a solid position, but it also isn't resting there.

Later this year, Nvidia's new Rubin architecture rolls out, and it has several improvements over the already impressive Blackwell architecture. Rubin chips can run inference at a tenth of the cost and can train models at a fourth of the cost. Those are major benefits that deserve a premium over prior generations, which will help Nvidia sustain its impressive revenue growth.

Additionally, the AI build-out is far from over. Nvidia estimates that by 2030, global data center capital expenditures will reach $3 trillion to $4 trillion annually. That may seem far-fetched, but Nvidia already projects the major AI hyperscalers will spend $1 trillion in 2027. Should both of those projections pan out and Nvidia maintain its market share, the returns on its stock could be phenomenal, and easily crush the market.

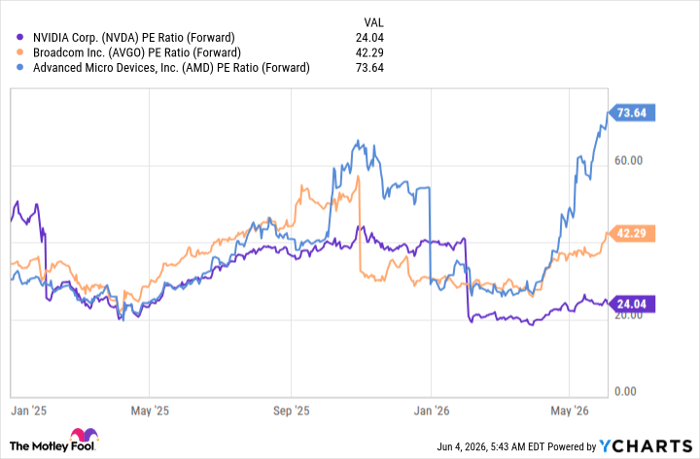

As a last point, Nvidia's stock is cheap compared to its peers. Other competitors in the AI computing world, like AMD and Broadcom, have captured the market's attention for what could happen with their offerings, while investors ignore what Nvidia is already doing. From a forward price-to-earnings (P/E) perspective, Nvidia trades at nearly half the level of Broadcom, and about a third the level of AMD.

NVDA PE Ratio (Forward) data by YCharts

Nvidia is reasonably valued and has a bright future ahead with new products rolling out. I think this makes Nvidia a solid stock pick over the next five years, and investors who missed out on its first run don't need to miss out on its second.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $443,191!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,258,838!*

Now, it’s worth noting Stock Advisor’s total average return is 941% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 7, 2026.

Keithen Drury has positions in Broadcom. The Motley Fool has positions in and recommends Advanced Micro Devices and Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles