Brent at $80: Did the market buy the Iran deal twice?

Brent is back near $80 and West Texas Intermediate near $77, which means the Oil market has handed back almost the entire premium it built over nearly four months of open war with Iran. The tape is treating this week's US-Iran memorandum as a finished peace: Blockade lifted, Strait of Hormuz reopening, Iranian barrels cleared to sell, equities at a record high while the President takes a victory lap on falling pump prices.

The problem is that the market ran this exact trade in April, priced the all-clear inside a single session, and got run over within hours when the people who can actually break the ceasefire were never asked to sign it. Nothing about the way this deal is built says the second attempt ends differently.

The all-clear got priced first

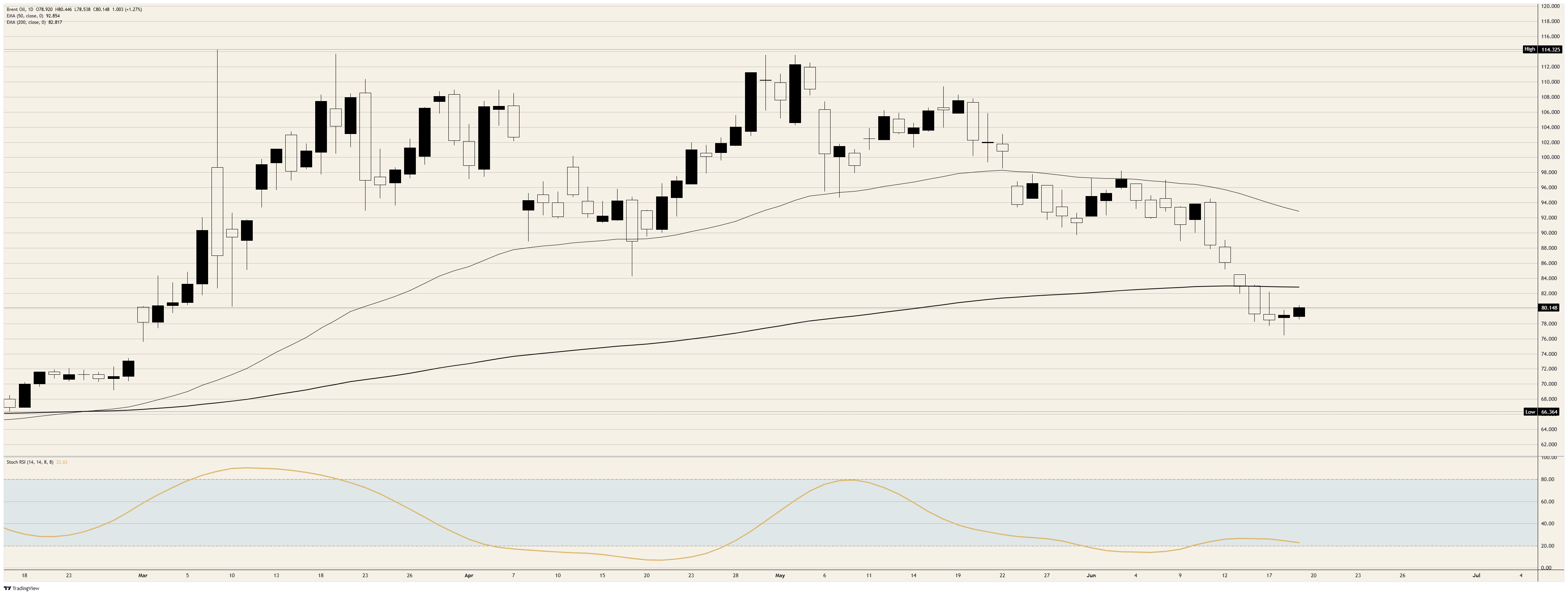

Since the fighting began on 28 February, Brent and WTI ran up more than 45%, with dated Brent cargoes printing above $120 at the peak as Hormuz traffic seized and Gulf loadings collapsed. That premium is now gone. Brent has shed roughly 8% on the week alone and sits in the low $80s, and crude has erased nearly all of its wartime gains, trading close to where it stood the day the first missiles flew.

Risk assets took the same cue, with US equities at a record high and the President crowing on Truth Social about tumbling crude and a record tape while writing off his critics as jealous or stupid. Read narrowly, the market is right: A deal exists, it is signed, and ships are moving. Read against what the deal actually binds, the de-risking looks early.

Open on paper, mined in the water

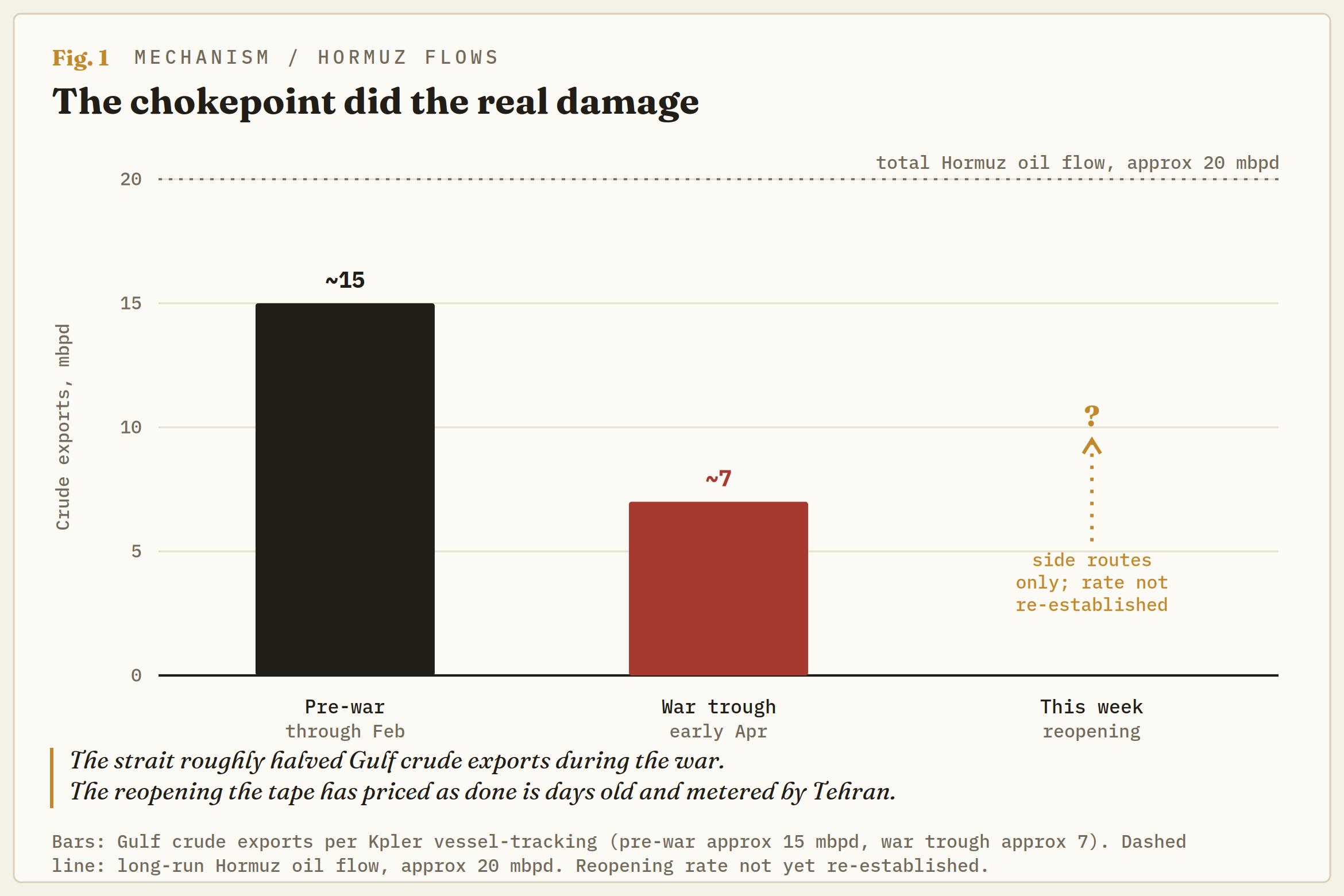

Start with the thing the entire move is pricing, a reopened Strait of Hormuz, the artery for roughly a fifth of the world's crude. It is open, but only at the edges. Tanker-industry trackers put the main central channel still closed, with an estimated 80 mines left to clear; traffic is threading the northern route inside Iranian waters and the southern route hugging Oman's coast, with US Central Command (CENTCOM) lifting port restrictions and maritime advisories steering ships to the Omani side to dodge the mines.

Even the flow that is moving is being metered by Iran's Islamic Revolutionary Guard Corps (IRGC), which has been openly capping vessel numbers to manage congestion. And Tehran is already fighting over the terms: Where Washington declared a toll-free opening, Iran says no such clause exists and that it will run the waterway on its own arrangements, inspections, services and security included. The supply relief the market has banked is therefore being delivered by Iran, at Iran's pace, reversible at Iran's word. That is not a normalised strait. It is a tap with Tehran's hand on it.

A two-party deal for a three-party war

Here is the part the price action is ignoring. The memorandum of understanding (MoU) is a bilateral document, 14 points, signed by President Trump at Versailles and by Iranian President Masoud Pezeshkian in Tehran. The war it is meant to end is not bilateral. Its most dangerous front runs through Lebanon, where Israel is fighting Hezbollah, and Israel never signed anything. The text calls for an end to the war on every front, Lebanon included; Israel's defence minister has said in plain terms that Israeli forces will hold the ground they have taken in Lebanon, Gaza and Syria indefinitely.

The gap is not academic, because Iran has already found the lever inside it. The technical talks meant to open in Switzerland today fell apart before they started, with Iran withholding its delegation over Israel's Lebanon campaign and demanding Israel withdraw first. So the 60-day clock that is supposed to squeeze Iran toward a nuclear settlement is a clock Iran can stop whenever Israel pulls a trigger Iran does not control. Three unbound actors, Israel, Hezbollah and Iran's own hardliners, can each break this, and the President's assurance that he can keep Israel in line landed hours before Israel ran its second-deadliest day of the war in Lebanon, with the government in Beirut counting 47 dead.

April already ran this experiment

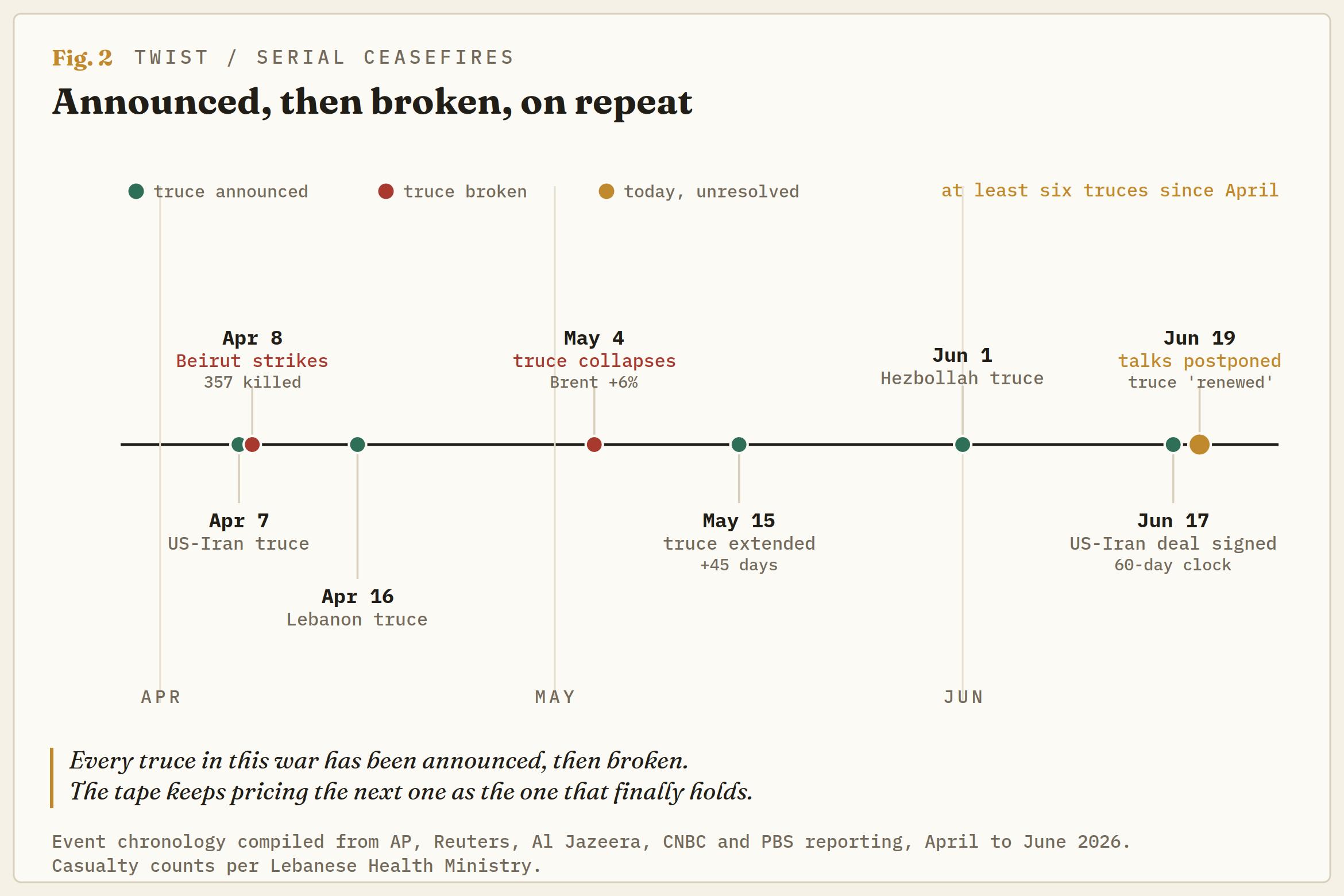

The reason to distrust the round-trip is that the market has lived it. In early April, Washington announced a two-week ceasefire and crude cratered around 16% in a single session, Brent collapsing toward the low $90s on the same logic driving today's tape. Within hours Israel hit Beirut in what it billed as its heaviest strikes of the war, killing more than 350 people, and the truce came apart.

By early May it had broken outright: Brent jumped 6% in a day back above $110, WTI cleared $100, the Dow shed more than 500 points and the volatility bid came back. The market faded the war premium then and wore the reversal. It is fading it again now, from a lower base, into a deal whose very first procedural step has already failed. The serial-ceasefire count is the tell. The Lebanon truce alone has been struck, broken and renewed at least five times since April, and today's version landed only after one of the bloodiest days of the conflict and still carries no confirmation from the Israeli military or Hezbollah. A ceasefire that has to be re-announced this often is not peace. It is a pause with better public relations.

Where the lean sits

The tape has priced a clean 60-day glide to a permanent deal. The lean is that the premium is too cheap for a window three spoilers can blow up. $80 Brent is the level the market is defending, and the triggers higher write themselves: Any incident in Hormuz, any hard break in the Lebanon truce, or an Iranian walk from the nuclear track as the clock runs down. Each one points the tape back toward the $90s, and a real re-closure of the strait reopens the $100-plus regime the market has spent weeks unwinding.

The other side is honest too: If the side routes stay open, the mines come out, and next week's Washington meetings hold Lebanon together, the premium keeps bleeding toward the low $70s base that prevailed before the war. But risk-reward skews toward keeping some war optionality into the clock rather than selling the last of it near $80. The deal is signed. Whether it holds is being decided by the people who never signed it.

Brent Spot, daily chart

Artigos Recomendados