Japanese Stocks Fall Nearly 1% at Open, 10-Year Yield Tops 2.8% to Hit Near 30-Year High

TradingKey - During the early Asian trading session on May 18, the Nikkei 225 Index dropped nearly 1% at the open as concerns intensified over the continued rise in global interest rates. Meanwhile, the 10-year Japanese Government Bond (JGB) yield surged to 2.8%, marking a nearly 30-year high since 1997.

Stock markets under pressure as semiconductor sector leads declines.

The Nikkei 225 index opened lower at 61,299 points, down 109 points or approximately 0.5% from Friday's close, before trending lower in volatile trading as losses widened to 1.5% during the morning session.

[Source: Yahoo Finance]

Analysis suggests that the broad sell-off in U.S. stocks last Friday weighed on Japanese equities, with the Dow Jones Industrial Average dropping over 500 points and the Nasdaq Composite also retreating significantly; selling pressure was particularly acute among high-valuation tech stocks led by semiconductors, amid generally weak market sentiment.

In terms of individual stock performance, semiconductor-related shares extended their decline, with SoftBank Group and Fujikura both falling over 2%, and Toyota Motor dropping more than 4%; the banking sector remained relatively resilient, as Mitsubishi UFJ Financial Group rose more than 3% and Sumitomo Mitsui Financial Group gained over 0.55%.

Market analysis indicated that rising global long-term interest rates are making equity valuations appear increasingly stretched, prompting a shift toward investor caution. The yield on the newly issued 10-year JGB rose to its highest level in approximately 29 years, further dampening market risk appetite.

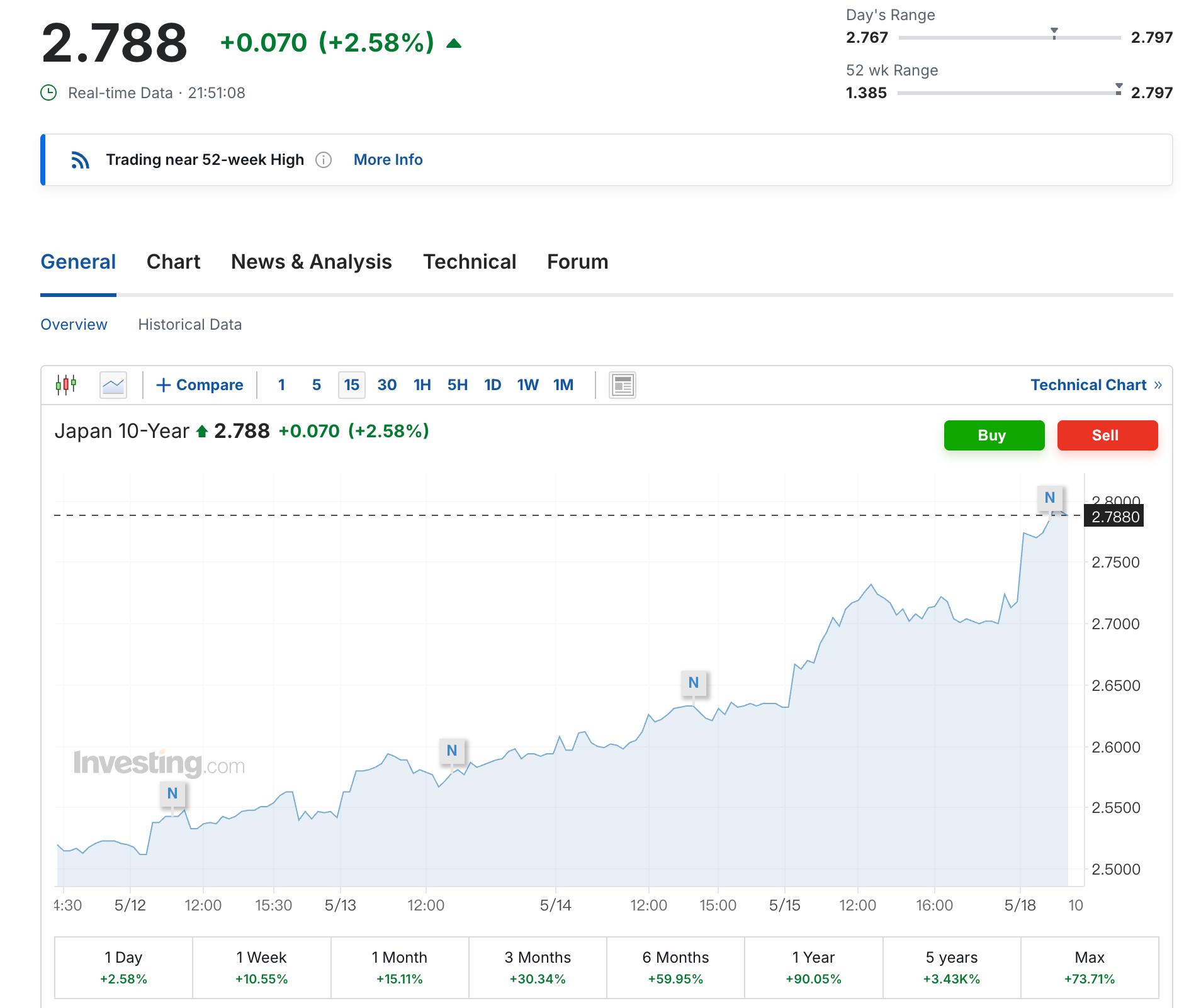

JGB yields climb across the board, 10-year yield surpasses 2.8%

The 10-year JGB yield briefly rose to 2.8% in early trading, continuing to hit a 28-year high, as the market anticipates it could advance toward 3% within the year. The 5-year yield climbed to a historic high of 2.0%, while the 20-year and 30-year yields reached 3.64% and 4.01% respectively, setting new multi-year highs.

[Source: investing]

The drivers of this round of rising JGB yields are not economic growth, but rather the combined impact of rising energy prices, loose fiscal discipline, and deteriorating supply-demand dynamics in the bond market.

Climbing Treasury yields, coupled with tensions in the Middle East pushing up oil prices, saw the 10-year U.S. Treasury yield rise to 4.612%. Meanwhile, Japan's corporate goods price index surged 4.9% year-on-year in April, further intensifying imported inflationary pressures.

Furthermore, the government is considering a supplementary budget for energy subsidies, sparking market concerns over a widening fiscal deficit. The convergence of these triple pressures continues to drive yields upward.

Intensifying BoJ hawkishness and rising JGB yields weigh on stocks.

The Bank of Japan maintained its interest rate at 0.75% with a 6-3 vote at its April meeting, but hawkish sentiment within the board was exceptionally strong, resulting in a rare three dissenting votes since the Governor took office. Some members explicitly stated that rate hikes are "likely to begin as early as the next meeting" and warned that the bank should "not hesitate to accelerate the pace of rate hikes" if price risks rise.

The Summary of Opinions indicated that current interest rates are still a considerable distance from neutral levels, suggesting a need for rate hikes every few months going forward. While traders estimate the probability of a June hike at approximately 77%, cautious signals from the government and variables in trade policy continue to present uncertainties.

Japanese government bond (JGB) yields continue to climb, exerting clear pressure on Japanese equities that have been rising since April. Keisuke Tsuruta, an analyst at Mitsubishi UFJ Morgan Stanley Securities, noted that market concerns over a widening fiscal deficit have driven up the "fiscal risk premium," serving as a major catalyst for the upward movement in interest rates.

Notably, some institutions forecast that long-term interest rates could rise to 3% this year; however, the recent strengthening of the yen may dampen bond demand, making the results of upcoming government bond auctions crucial to monitor.

Overall, the global interest rate environment is undergoing a systemic shift, and the normalization of Japanese rates is accelerating. The valuation pressures and capital outflow risks facing Japanese stocks cannot be ignored.

Recommended Articles