Semiconductor Sector Continues to Rise, Should Retail Investors Buy Intel or AMD?

- US President Donald Trump says trade will be priority in summit with Xi, not Iran

- Gold drifts higher to near $4,750 ahead of US CPI inflation release

- Gold slumps below $4,700 on Trump rejection of Iran peace proposal

- WTI falls to near $93.50 after Israel, Iran signal an end to hostilities

- Inflation 'High Fever' Fails to Stop Rally? BTC Temporarily Loses 80,000 Mark, But Arthur Hayes Sees Peak of $126,000

- When Will the Gold Dilemma Be Resolved? Breakdown of US-Iran Negotiations Puts Gold Prices Under Pressure Again, Can It Return to $5,000?

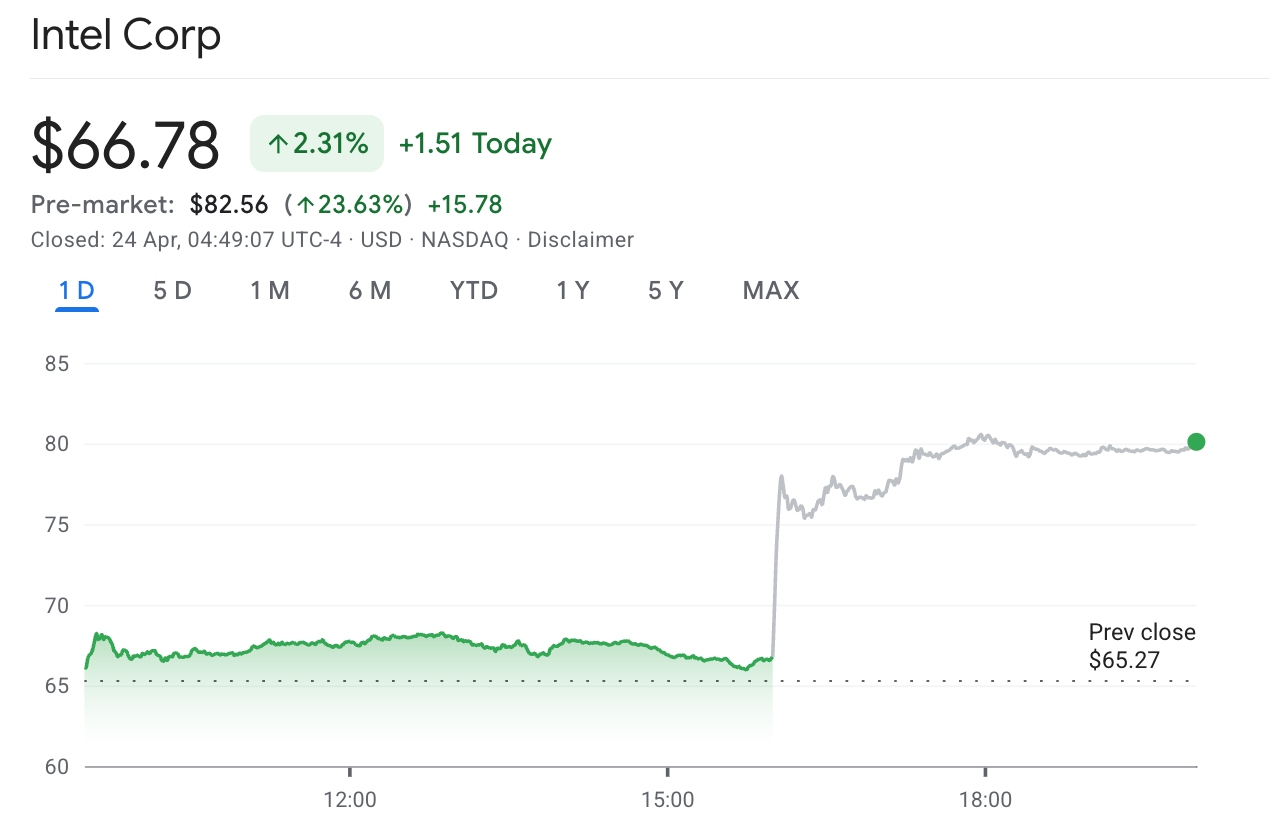

TradingKey - On April 23, Eastern Time, Intel (INTC) reported its latest quarterly earnings results, showing that revenue grew 7% to $13.6 billion and earnings per share was $0.29, beating expectations. Analysts had on average projected revenue of $12.4 billion and EPS of $0.01.

At the same time, Intel expects second-quarter revenue to range between $13.8 billion and $14.8 billion, far exceeding the $13.0 billion previously expected by analysts. EPS is projected to be $0.20, higher than the earlier forecast of $0.09.

Driven by the news, Intel's stock price surged 20% in after-hours trading, breaking the $80 mark and reaching its highest level since the dot-com bubble burst. Meanwhile, Intel's strong earnings results boosted semiconductor technology stocks as a whole, AMD gained 7.65% in tandem after hours,

Notably, AMD has already risen over 40% in 2026. As the wave of AI computing power shifts from 'training' to 'inference,' both chip giants have reached their respective highlight moments.

For retail investors, should they bet on the high-flying AMD, or position themselves in an Intel that has just proven its recovery capability?

Positive Earnings Outlook Fails to Stop Wall Street From Voting With Its Feet

Intel has clearly stated that AI-related business now accounts for 60% of its total revenue, and customers are purchasing Intel Xeon processors in large quantities for inference tasks beyond GPUs. A supply gap reaching "billions of dollars" has provided a buffer for the stability of upcoming earnings reports. Coupled with Q2 guidance that far exceeded market expectations, this underscores management's strong confidence in future demand.

Furthermore, two major customers— Tesla (TSLA) announced the adoption of Intel's 14A process for AI chip production, while Google (GOOGL) signed a multi-year agreement to deploy Xeon processors and collaborate on the development of custom chips. These votes of confidence provide substantial support for the long-term prospects of Intel's foundry business.

Nevertheless, judging solely by valuation, Intel's current valuation clearly struggles to support its current stock price.

As of the April 23 earnings release, among the 34 Wall Street analysts covering Intel, 24 issued a "Hold" rating, with an average price target of only $55.33. Most Wall Street institutions remain bearish on Intel, viewing it as a target that lacks cost-effectiveness.

While Jefferies raised its price target to $80 following the results, JPMorgan lifted its target to $45, and Jefferies Group maintained its Hold rating while raising its price target, and Mizuho Securities downgraded the rating but raised its target to $71, nearly all institutional price targets remained below the stock's after-hours closing price that day.

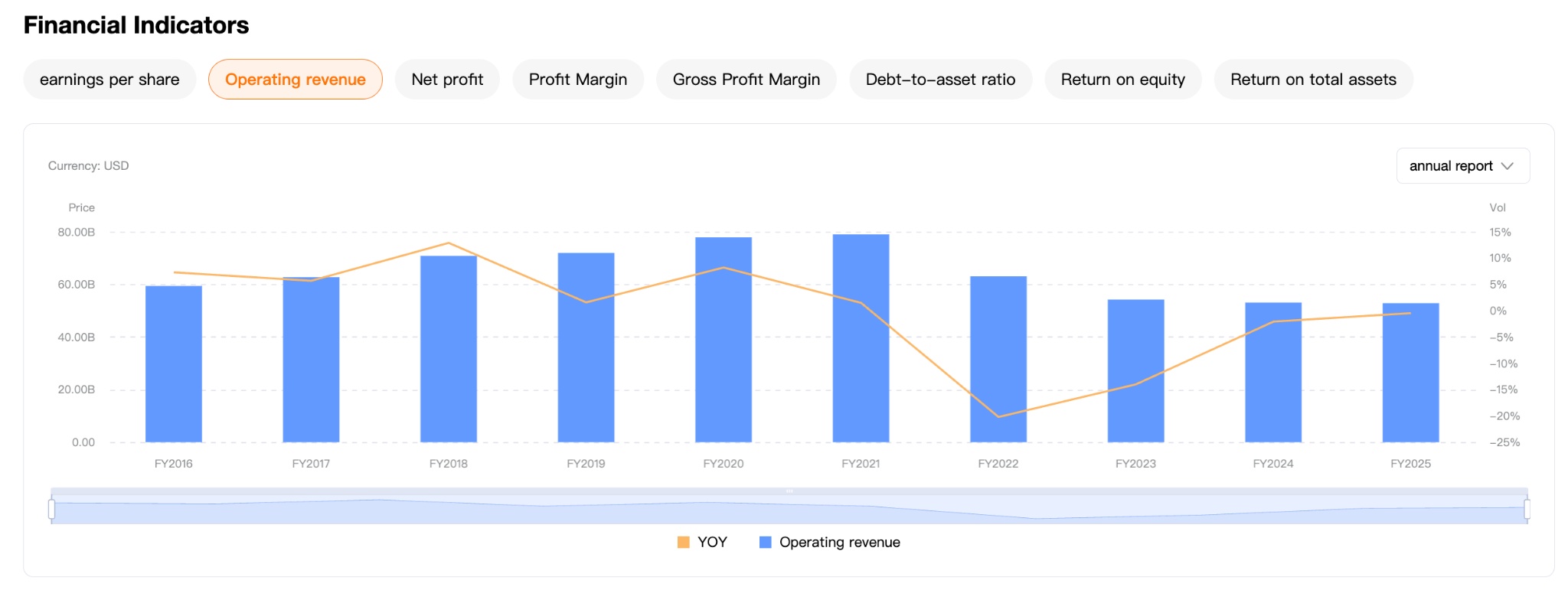

It is worth noting that despite Intel's impressive earnings report, its projected 2025 full-year revenue remains 32% below its 2021 peak.

The growth prospects for the two differ.

Both companies' bets on "AI inference" are aligned in direction, but there are distinct differences in their narrative structures.

Intel's turnaround strategy is based on a revaluation of CPU value driven by AI agent architecture. During the earnings call, CEO Lip-Bu Tan stated directly that "CPUs are once again becoming an indispensable foundation of the AI era." The core reason is that as large AI models move into the inference and agent deployment phases, the ratio of CPUs to GPUs is shifting from 1:8 toward 1:4, driving unprecedented demand for CPUs in general-purpose servers.

Tesla will utilize Intel's 14A process for AI chip production, and Google has signed a multi-year supply agreement to secure the market position of Intel Xeon processors in cloud AI inference—these two top-tier industry endorsements provide solid support for Intel's growth prospects.

Meanwhile, AMD's moat is built on its steadily climbing market share. According to Mercury Research data, AMD's share of server CPU revenue reached 41.3% in the fourth quarter of 2025, and its share gains have effectively cannibalized Intel's market.

Additionally, AMD signed a 6GW data center agreement with Meta—this multi-year partnership directly involves Meta issuing warrants for up to 160 million shares to AMD, deeply aligning the interests of the world's largest AI infrastructure buyer with AMD.

AMD Wins Through Stability, Intel More Like a Gamble

AMD's risk-reward profile is more predictable; its server CPU business continues to capture market share, and its AI chip product cycle drives a long-term narrative with strong growth visibility.

In contrast, Intel's ability to maintain its growth momentum hinges on two variables: whether PC demand remains robust and whether its 14A process, 18A yields, and external customer orders continue to materialize.

For retail investors seeking a more stable allocation, AMD's valuation premium is backed by clear market share expansion and massive orders from Meta and OpenAI, making it more suitable as a core option for long-term holding.

If one has firm confidence in the long-term narrative of "AI inference reshaping CPU pricing power" and Intel's subsequent quarterly earnings continue to validate a supply-constrained environment, there is further theoretical room for a valuation re-rating.

However, at present, Intel's stock price has excessively reflected its growth peaks for the coming quarters; the general institutional stance remains "wait and see," and for retail investors, entering this high-beta option requires more prudent judgment.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.