Down 39%, Is It Finally Time to Buy Upstart Stock?

Key Points

Upstart reported strong first-quarter growth, along with a net loss.

The business is rebounding despite the continued headwinds of high interest rates.

Upstart stock is still expensive at the current price.

- 10 stocks we like better than Upstart ›

Despite progress in its turnaround, artificial intelligence (AI) stock Upstart (NASDAQ: UPST) disappointed the market with its first-quarter earnings, and the stock is down 39% this year. Is it an opportunity to buy on the dip? Or a value trap? Let's check it out.

Upstart is disrupting credit with AI

Upstart's AI and machine-learning-driven credit evaluation platform represents a fundamental change in how lenders assess credit. Legacy credit scores use a handful of criteria to see if a potential borrower is trustworthy, leaving excellent candidates sidelined. According to management, Upstart's model approves more borrowers without adding risk to the lender. That's a win-win for both parties.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

When it became a public company six years ago, Upstart had only 10 lending partners, and one in particular that presented a huge majority of its business. Today it has more than 100, including a deal it announced just this week with USF Credit Union, a Florida-based financial cooperative.

It has branched out of its original category of personal lending into auto lending and home products, and these have been fast-growing segments, with originations up 300% and 250%, respectively, year over year in the 2026 first quarter. Part of the model includes working with institutional partners that fund its loans so that it has low exposure to interest rate changes and defaults.

While Upstart reported fabulous growth when interest rates were low, it hasn't been as successful in the higher-rate environment. Even its robust algorithms have a harder time identifying good borrowers when rates make it a challenge to pay back loans, and there are fewer people who are looking for loans at high rates.

It does seem to have hit rock bottom, though, and it's been reporting higher growth for several quarters now.

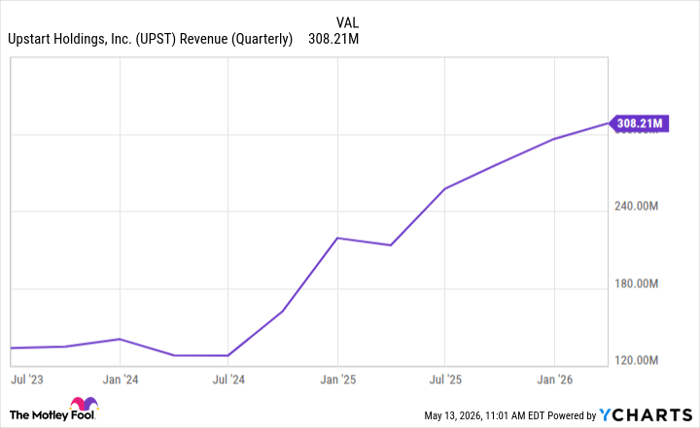

UPST Revenue (Quarterly) data by YCharts

In the first quarter, transaction volume increased 77%, and revenue was up 44%. That's excellent progress given the continued high-rate environment. However, it's come at a cost, and it reported a $7 million net loss for the quarter.

One exciting update is that Upstart is applying for a bank charter, which could expand its operations.

Value trap? Opportunity? Or neither?

My personal opinion is that Upstart is neither a great opportunity or a value trap. The business model looks strong, but it's facing competition from other credit disruptors as well as the king of the field, Fair Isaac, which is also using AI to improve its scoring methods. It's still expensive, trading at 69 times trailing-12-month earnings, which is why it's not quite a bargain chance to buy nor cheap enough to be called a value trap.

For now, I'd continue to stay on the sidelines and wait for more sustained growth and stability.

Should you buy stock in Upstart right now?

Before you buy stock in Upstart, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Upstart wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $472,744!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,353,500!*

Now, it’s worth noting Stock Advisor’s total average return is 991% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 14, 2026.

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Upstart. The Motley Fool recommends Fair Isaac. The Motley Fool has a disclosure policy.

Recommended Articles