Why GE Aerospace Still Fell Over 5% as Results Beat Expectations?

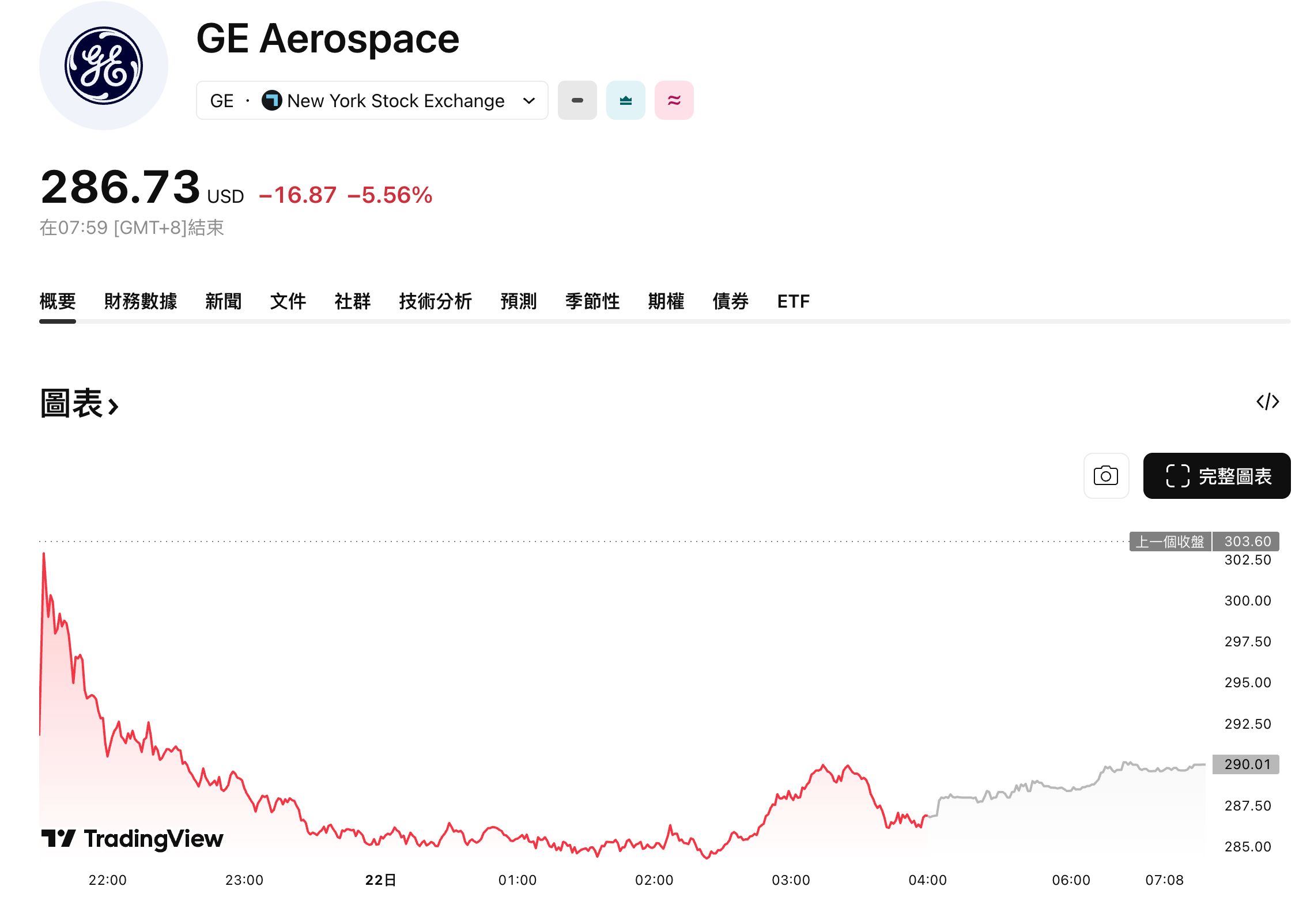

TradingKey - GE Aerospace ( GE) reported first-quarter results on Tuesday, April 21, with revenue of $11.6 billion, exceeding expectations by $900 million. Adjusted earnings per share were $1.86, beating market estimates by $0.26. Despite the earnings beat, the stock closed down 5.56% at $286.73, with approximately $20 billion in market value wiped out in a single day. The primary reason for the decline was the potential impact of the Middle East conflict on the aviation industry.

[Source: TradingView]

Results beat expectations across the board.

In the first quarter, GE Aerospace recorded total orders of $23 billion, up 87% year-over-year. Commercial Engines & Services orders reached $17.3 billion, an increase of 93% year-over-year, while Defense & Propulsion Technologies orders were $6.2 billion, up 67% year-over-year. During the period, customers including American Airlines, United Airlines, and Delta Air Lines collectively ordered more than 650 commercial engines, with the commercial services backlog surpassing $170 billion.

Adjusted revenue was $11.6 billion, up 29% year-over-year and significantly higher than the market expectation of $10.69 billion; adjusted earnings per share were $1.86, up 25% year-over-year and beating the estimate of $1.60; free cash flow was $1.7 billion, a 14% increase year-over-year.

GE Aerospace vs RTX

On the day GE Aerospace released its earnings report, its stock price reversed a 2.4% pre-market gain to close down 5.56% at $286.73, bringing its year-to-date decline to 6.91%.

Its competitor Raytheon Technologies ( RTX) also released its earnings report on the same day, closing down 4.4% and outperforming GE Aerospace overall. This was primarily because RTX has a broader business scope, including the Pratt & Whitney engine aftermarket, Collins Aerospace, and Raytheon Missiles & Defense; its missile business benefited from global defense spending expansion, hedging commercial aviation risks. In contrast, about 75% of GE Aerospace's profit is derived from commercial engines and services, making it significantly more sensitive to flight volumes than RTX.

Middle East Conflict Reshapes Flight Expectations

During the earnings call, management identified the conflict in the Middle East as the primary uncertainty. CEO Larry Culp stated that the company needs to face reality. While global flight volumes grew by single digits in the first quarter, they declined by high single digits in the Middle East, which accounts for 5% of GE Aerospace's total flight volume.

Disclosures from the conference call indicate that after evaluating multiple scenarios, the company lowered its 2026 global flight growth forecast from single digits to flat or low single digits, with the Middle East expected to see a low double-digit decline for the full year. This decline is estimated to represent a drag of approximately 0.5 to 0.8 percentage points on GE's overall flight volumes.

Larry Culp noted that the conflict's impact could persist through the summer, but the company expects the effect on 2026 service revenue and profits to be limited. This is primarily due to the lag between flight changes and service demand, coupled with a cushion of over $170 billion in commercial services backlog. FlightGlobal reported that first-quarter commercial aftermarket service revenue reached $6.8 billion, up 39% year-over-year, accounting for 76% of total commercial revenue.

CFO Rahul Ghai stated that Brent crude is assumed to remain at elevated levels throughout the quarter, with potential for a pullback only toward year-end. Goldman Sachs estimates that if the Strait of Hormuz remains closed, Brent crude could average $120 per barrel in the third quarter. GE's fuel assumptions reflect recent supply constraints but do not incorporate a global recession scenario.

Airline customers under pressure

Rising fuel costs have already been passed on to downstream customers. United Airlines' quarterly report, released the same day, indicated that although first-quarter net profit rose 80% year-over-year to $699 million, the impact of rising fuel prices led it to significantly lower its full-year 2026 adjusted earnings per share guidance from the previous range of $12 to $14 to $7 to $11. United also announced a reduction in capacity for the second half of the year by approximately 5% and expects that 40% to 50% of the increase in fuel costs can be passed on through fares in the second quarter, rising to 80% in the third quarter and reaching 85% to 100% by year-end.

Assuming fuel costs remain at elevated levels, airlines may postpone maintenance on older engine models such as the CFM56 and GE90, which are the primary profit drivers for GE's services business. According to IATA data, jet fuel prices have doubled since January. Management stated that service demand typically lags behind changes in flight activity, but airlines have already begun adjusting their near-term plans.

The defense business provided support during the quarter. Larry Culp noted that military engine utilization has improved since March, benefiting the aftermarket for platforms including the T700 Black Hawk, Apache, F-15EX, and F-16. While defense and systems deliveries grew by 24%, growth in the defense segment was unable to offset market concerns regarding the medium-term outlook for commercial aviation.

GuruFocus data indicates that GE Aerospace's stock price is 27.5% higher than its GF Value, placing it in the modestly overvalued range.

Future outlook

The U.S.-Iran ceasefire agreement expired on April 22, and transit through the Strait of Hormuz has not resumed. Iran stated that unconditional passage is "a thing of the past." The International Air Transport Association (IATA) warned that Europe could see flight cancellations by late May due to fuel shortages.

GE Aerospace reported robust Q1 orders, but downward flight revisions, soaring fuel costs, and customer earnings downgrades have reshaped industry expectations. The stock price decline is not a reflection of poor performance, but rather the market beginning to price in geopolitical risks.

Investors should monitor the recovery of Middle East flights (weekly IATA data), United Airlines' Q2 capacity guidance in May, and the jet fuel-Brent crude spread. Should these indicators improve, GE Aerospace's valuation recovery window could open earlier than expected.

Recommended Articles