Intel Q1 2026 Earnings Preview: The Rally is Ahead of the Fundamentals

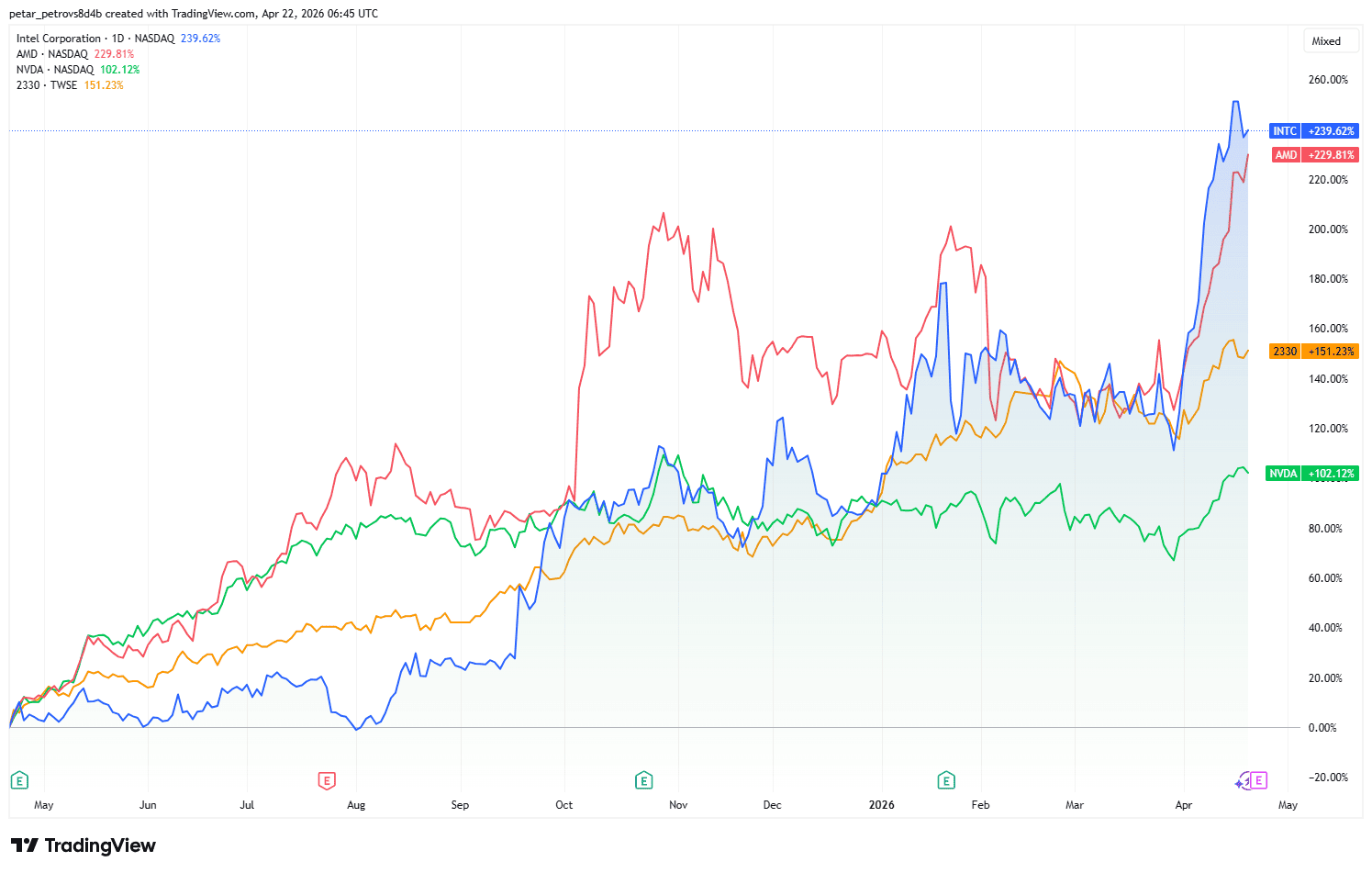

In the past 12 months, Intel (INTC) has surprisingly outperformed every major competitor — including NVIDIA, AMD, and TSMC. This is somewhat counterintuitive, given that Intel has long been viewed as the “sick man” of the semiconductor industry.

Source: TradingView

What Has Driven the Rally?

The rally has been supported by several key factors:

US Government Backing: The United States has effectively positioned Intel as its “National Champion.” The government took a 9.9% stake in the company for $8.9 billion, sending a strong signal that Intel is considered “too big to fail” despite its heavy debt load and operational challenges.

New Leadership: Hope has been reignited under new CEO Lip-Bu Tan, who took over last year. He has focused on streamlining operations and accelerating progress on the critical 18A and 14A process nodes.

Strategic Partnerships:

· The Terafab project with Elon Musk’s companies

· Collaboration with NVIDIA to package CPUs and integrate them with NVIDIA GPUs

· Deals with major hyperscalers (Amazon and Microsoft) looking to diversify their supply away from TSMC.

Most importantly, there is a rising demand for CPUs driven by the growth of agentic AI.

Q1 2026 Earnings Expectations

Metric | Consensus Estimate (Q1 2026) | Intel Official Guidance | Q1 2025 Actual | YoY Change |

Revenue | $12.52 Billion | $11.7B – $12.7B | $12.67 Billion | -1.18% |

Non-GAAP EPS | $0.01 | ~$0.00 (Breakeven) | $0.13 | -92.31% |

Gross Margin | 34.50% | 34.5% (Non-GAAP) | 37.78% | -3 pp |

Looking at these numbers, the growth and margin profile looks quite underwhelming — especially when compared to the explosive results from NVIDIA, AMD, and TSMC. This raises an important question: Is the positive market sentiment around Intel running significantly ahead of its fundamentals? In other words, are investors “turning on the stove before catching the fish”?

How Does Intel Generate Revenue

Intel’s business remains heavily concentrated in two core segments:

- Client Computing Group (CCG) — PC CPUs — which still accounts for roughly 60% of total revenue. Growth here is expected to stay sluggish or negative, as production capacity is being redirected toward higher-priority server products.

- Data Center and AI (DCAI) — Server CPUs for cloud providers — representing around 30% of revenue. In Q4 2025, this segment grew only 7% year-over-year, a modest figure compared to AMD and NVIDIA’s 30%+ growth rates. Further improvement is anticipated, but significant acceleration appears limited in the near term.

- Foundry Services: External foundry revenue remains tiny. In Q4 2025, it was only $222 million — roughly 5% of total foundry output. Even if it scales quickly, the base is so small that it will take considerable time to move the needle on overall profitability. The success of the 18A process node (Intel’s equivalent to TSMC’s 2nm) will be make-or-break, especially in achieving competitive yields.

Other business lines are relatively minor and are not expected to be meaningful contributors in the near future.

Why Intel Is Lagging AMD in Growth?

Intel’s revenue growth continues to trail AMD for several structural reasons:

- Ongoing market share erosion means Intel’s top-line growth naturally lags behind faster-growing competitors.

- “Hand-to-mouth” inventory dynamics: Intel can basically only sell what it produces, with very little inventory buffer. This caps its ability to grow revenue quickly.

- Unlike AMD, which is fabless and can leverage TSMC’s superior production capabilities, Intel operates its own fabs and is more exposed to supply disruptions and delays.

- Chronic production issues, including severe delays with Sapphire Rapids and Emerald Rapids processors.

As a result, analysts do not expect Intel to return to meaningful revenue growth until 2027–2028, when better yields, improved supply, and a larger contribution from the foundry business (through Terafab or other major third-party customers) finally kick in.

The Margin Problem

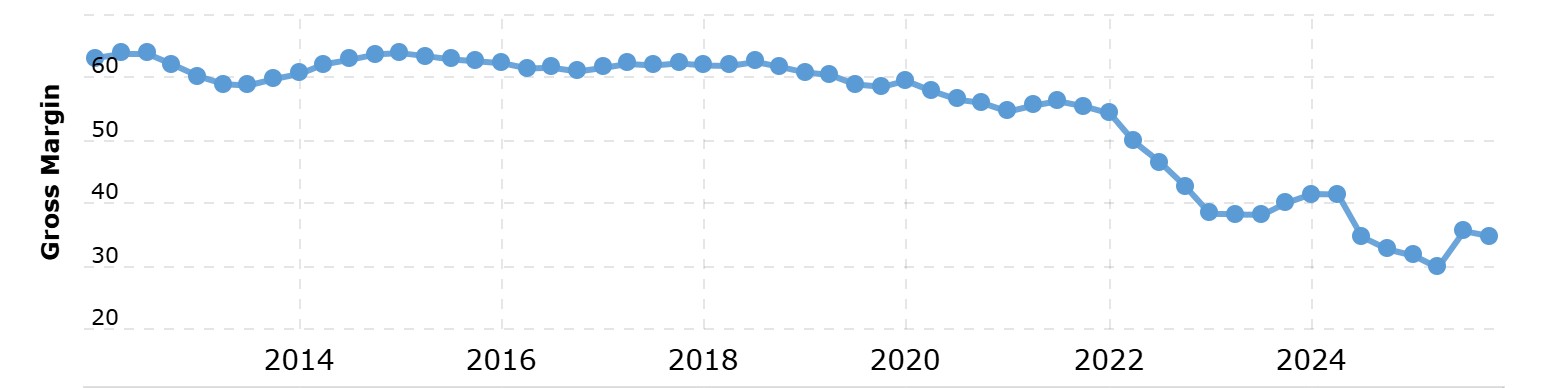

Intel’s gross margin has fallen dramatically from historical levels above 60% to around 35% today.

Source: Macrotrends

A return to those peak levels looks highly improbable. In the past, Intel enjoyed overwhelming market dominance, strong pricing power, and efficient fabs. Today, it faces intense competition, low production yields, massive capital expenditure requirements, and heavy depreciation charges.

Even matching AMD’s roughly 55% gross margins over the long term seems unrealistic. AMD benefits from a much higher proportion of high-margin GPUs (30–35% of revenue in Q4 2025 versus less than 5% for Intel). GPUs command better pricing due to their semi-oligopolistic market structure and strong software ecosystems (CUDA for NVIDIA, ROCm for AMD), while CPUs have become more commoditized.

Additionally, AMD’s fabless model results in much lower depreciation (only 8–9% of revenue) compared to Intel’s ~21%. Even if Intel’s foundry business scales up, it is unlikely to reach TSMC’s 60%+ gross margins due to differences in experience, scale, and yields. Intel’s planned CapEx of $17–18 billion is spread across both products and foundry, while TSMC is expected to spend $52–56 billion — almost entirely focused on its core foundry operations.

This gap raises doubts about Intel’s ability to catch up technologically.

Not only this, Intel is also taking a significant first-mover risk by adopting High-NA EUV lithography, in contrast to TSMC’s more conservative Low-NA approach. If successful, this could allow Intel to leapfrog TSMC by 2027–2028 with a simpler and faster path to 1.4nm chips. However, being the pioneer also means confronting all the early operational challenges without the benefit of prior experience.

While the announced partnerships (Terafab, NVIDIA collaboration, hyperscaler deals) have generated excitement, most still lack clear revenue visibility. The financial impact of Terafab remains too early to quantify, and Intel’s exact role in NVIDIA’s Vera Rubin platform is still unclear.

Final Thoughts

At $20–$30 per share, Intel was undeniably cheap. At current levels of $60 and above, however, the valuation demands far more visible execution success. Much of the positive news — government backing, new leadership, and partnerships — already appears priced in. The underlying challenges remain - sluggish growth, compressed margins, operational risks around yields, and structural disadvantages including limited pricing power and an inefficient foundry model.

The bull case relies heavily on a successful turnaround, but meaningful proof is still pending.

Recommended Articles