Trump TACO Trade Saves Market, But Who Are the First Victims of the TACO Trade?

- Gold Price Forecast: XAU/USD keeps looking for direction above $4,500

- Gold Price Forecast: U.S.-Iran Negotiations Face Uncertainties, Gold May Fall Below $4,400

- Gold declines to near $4,500 as renewed US‑Iran tensions, Fed tightening bets weigh

- Gold edges higher above $4,550 on US-Iran peace optimism

- Forex Today: Risk flows dominate markets on US-Iran deal hopes

- Gold holds steady near $4,550 as market eyes Middle East developments

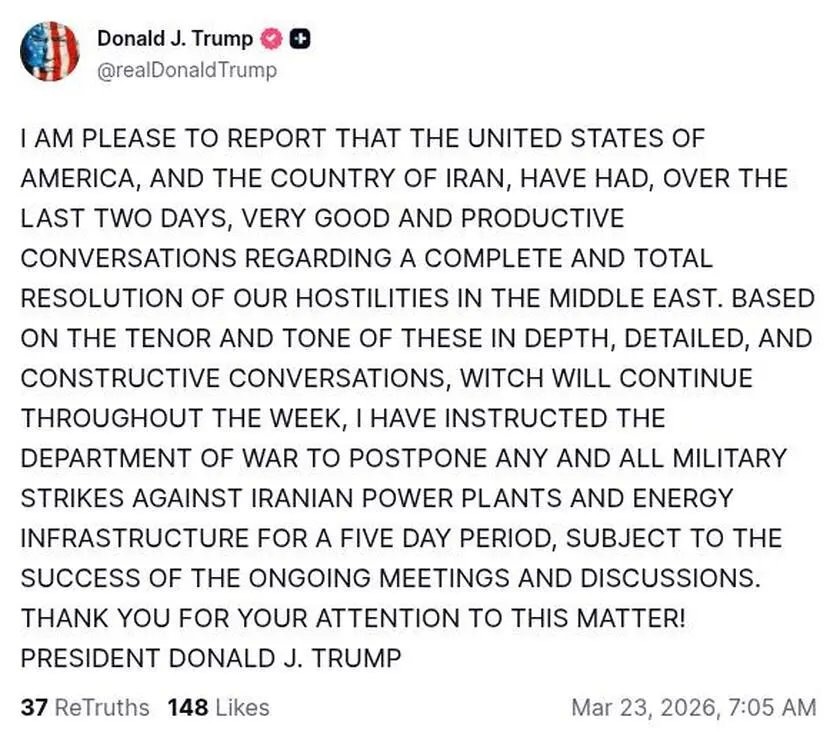

TradingKey - As U.S. President Trump once again signaled a de-escalation of tensions in the Middle East, global markets swiftly entered "TACO trade" mode: risk assets rallied, safe-haven assets retreated, and volatility rapidly converged.

On the surface, this trading logic benefits most global risk assets and weighs on crude oil; however, from the perspective of deeper market structures, its true impact is actually on a specific type of trading strategy.

What is Trade At Cash Open (TACO) trading?

The "TACO trade" is a term coined by Financial Times columnist Robert Armstrong during Trump's implementation of global tariffs, referring to the market's attempt to anticipate the extreme volatility caused by U.S. President Trump issuing massive tariff threats and then subsequently backing down.

TACO is an acronym for "Trump Always Chickens Out," broadly questioning whether Trump consistently retreats from his tariff threats. The TACO trade refers to investors profiting by buying the dip after market sell-offs triggered by Trump's tariff threats.

In 2025, Trump repeatedly reversed his position after adopting a hardline stance on tariff sanctions, instead signaling more moderate policy intentions; as a result, global markets frequently experienced crypto-style volatility characterized by violent rallies and crashes.

TACO’s Biggest Victim

The first victims are often highly leveraged funds betting on a "unilateral escalation" of the conflict.

First, "geopolitical premium bulls" in the energy market bear the brunt. In the early stages of a conflict, the rise in oil prices is driven more by the pricing of supply disruptions and shipping risks rather than long-term demand-side improvements. Once policy signals show marginal signs of easing, this risk premium will be rapidly compressed, and the pace of price retracement is often faster than the rally phase.

Under these circumstances, long capital relying on trend continuation, particularly short-cycle CTA strategies, is prone to passive profit-taking or even stop-loss exits during reversals, becoming the earliest group to suffer losses.

At the same time, leveraged directional shorts also face structural pressure. Taking inverse products that short technology stocks or single assets as examples—such as the TSDD ETF and various stock index inverse ETFs—these assets face "path-dependency risk" in a "TACO environment."

When the market exhibits high-frequency reversal characteristics of "sharp falls and rapid rallies," even if medium-term judgments are correct, frequent counter-trend fluctuations will erode net asset value through compounding decay, causing actual returns to deviate significantly from expectations.

A more easily overlooked category of victims is volatility buyers. During the escalation phase of geopolitical conflicts, implied volatility rises rapidly, benefiting long options and tail-hedge strategies significantly. However, as the market gradually forms a "TACO consensus"—that the conflict is subject to upper bounds—volatility will systematically decline. This means that capital betting on uncertainty will face a "double squeeze" of time value decay and falling volatility, with profit margins rapidly compressed.

In addition to the explicitly affected groups mentioned above, some funds that "passively take on risk" also face challenges.

For example, risk parity and certain passive allocation funds typically hedge risks by increasing commodity allocations and reducing equity exposure during conflict escalation. When the market quickly shifts to "de-escalation expectations," the adjustment pace of these funds often lags behind active traders, causing them to endure extra volatility during violent asset price reversals.

In a "TACO-dominated" market environment, expectations for recovery after a crash will gradually heat up. Therefore, the most vulnerable are not necessarily investors with incorrect judgments, but rather trading strategies that are overconfident in a single narrative and layered with high leverage.

For investors, this means that in the coming period, the risk-reward profile of unidirectional bets is declining, while the importance of hedging, diversification, and dynamic adjustment capabilities continues to rise.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.