DocuSign: This SaaS Giant Is Reinventing Itself

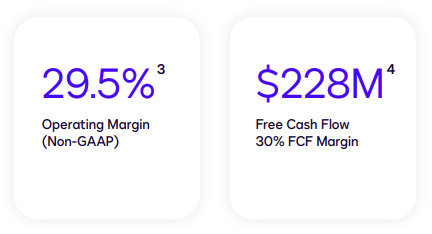

- Docusign reported a 29.5% non-GAAP operating margin and 30% free cash flow margin in Q1 FY26.

- The Intelligent Agreement Management (IAM) platform surpassed 10,000 customers and aims to reach double-digit subscription contribution by year-end.

- A $1.4 billion stock repurchase authorization signals confidence and capital discipline, covering nearly 19% of market capitalization.

- Despite a 61.2x GAAP P/E, Docusign trades at 21x non-GAAP and ~16x EV/FCF, suggesting valuation rerating potential.

TradingKey - While almost every investor is anchoring on Docusign’s (DOCU) post-pandemic hangover and a high valuation that isn’t exactly pretty at first glance, the market could be missing out on the company’s bigger transformation: an irreversible move into AI-native enterprise infrastructure.

Source: Grand View Research

Docusign’s present price level at $74 represents the company in transition, no longer just a digital signature solution but increasingly becoming an intelligent agreement platform. The result? A financial scenario with progressing margins, recurring revenue clarity, and platform adoption that’s getting momentum and potentially overdue for a huge rerating.

Source: Seeking Alpha, Stock Price Summary

What makes this thesis contrarian is that valuation compression and platform expansion coexist simultaneously. On a forward GAAP P/E basis, Docusign is trading at 61.2x, over 112% above the sector median. But such seeming overvaluation disintegrates when placed into perspective with platform reinvestment lens and margin normalization adjustments. In reality, the company recently announced a 29.5% non-GAAP operating margin and a 30% free cash flow margin in Q1 FY26 despite macro headwinds. These measures of efficiency that are greatly overlooked by headline multiples reflect a scalable model going into inflection.

Source: Docusign Q1’26 Presentation

On top of that, there's a $1.4 billion authorization for stock repurchase, a sign of capital discipline and confidence that's difficult to find among software businesses that are themselves continuing to invest meaningfully in product transformation. If the Intelligent Agreement Management (IAM) platform continues scaling at the slated rate, into a low double-digit percentage of subscription revenue by year-end, Docusign could surprise the market with something more than steady growth, but with operational leverage and monetization depth that few are contemplating today.

In short, Docusign isn’t just a COVID bubble residue; it’s a modest infrastructure investment in an economy that’s dependent on contracting. When the IAM platform scales and monetizes workflows with AI-based foundations, DOCU’s stock arguably has asymmetric potential upside from a defensible free-cash-flow platform.

From Signatures to Intelligence: Re-Architecting the Agreement Economy

Docusign's business model has evolved significantly from its roots in e-signatures. The company now positions itself as the foundation for enterprise agreement intelligence, to a place it itself has created, "Intelligent Agreement Management" (IAM). This transformation is more than superficial. On the basic level, it is evidence of a shift away from isolated digital interaction towards a platform-based workflow engine embedded throughout legal, procurement, HR, sales, and finance functions.

The IAM platform consists of three connected modules: Create, Commit, and Manage. In this architecture, organizations are enabled to create, negotiate, and execute agreements with simplicity and interact with third-party systems like Salesforce (via Docusign for Agentforce), Coupa, and even biometric identification by CLEAR. With the recent addition of Docusign Iris, their own AI engine, the company has embedded large-scale contract intelligence at every aspect of the agreement life cycle. AI Contract Agents, AI-Assisted Review, and Obligation Management Dashboards transform static documents into fluid data pipelines.

It’s not only tech differentiation; it’s getting Docusign more deeply ingrained in customer infrastructure. More than 95% of the Fortune 500 are already customers of Docusign for e-signatures. IAM provides a roadmap to broaden wallet share from digital-only customers into comprehensive enterprise deployments. That growth is happening now: Docusign went past 10,000 IAM customers during Q1 FY26 and is aiming for double-digit percentage contribution by year-end to the subscription business.

Source: Grand View Research

And the global story is gaining traction. With 28% of revenue now generated outside the U.S. and 10% YoY international revenue growth, Docusign is going local with its IAM go-to-market playbook. Geographic prioritization by tiers, from digital-first through fully localized direct sales, has defined a scalable global distribution model with margin-sensitive efficiency.

Source: Docusign Q1’26 Presentation

That shift, from signature application to workflow platform, builds a strategic moat that few comprehend. The unit of business is the agreement. When Docusign controls that workflow start-to-finish, it’s digitizing paperwork; it’s business-ifying trust at scale.

AI-Native versus App-Based: Competitive Positioning of DocuSign against Increasing Noise

The competitive environment for Docusign has intensified over the past two years, with incumbents such as Adobe, cloud-native players such as PandaDoc, and vertical-specific CLM providers such as Ironclad or Agiloft vying for their seats at the table. But what the IAM pivot truly does is shift the competitive calculus entirely by framing Docusign’s moat in platform breadth, AI-native architecture, and data closed loops.

Unlike competition with bolt-on AI or standalone contract lifecycle offerings, Docusign’s AI engine learned from over 20 years’ experience in contract workflow, so Iris is a domain-specific LLM that’s fine-tuned for legal and enterprise use. That’s not generic GenAI, it’s proprietary learned intelligence from billions of agreement interactions. That provides a first-mover advantage that’s tough to scale by horizontal offerings such as Microsoft Copilot or Google Workspace.

Moreover, Docusign’s approach significantly differs from the majority of the competition. Most are focused on high-growth top-line with high-churn digital plans, yet Docusign derives 85% revenue from direct enterprise and commercial customers. Subscription model (prepaid, multi-factor) with seat-based, volume envelopes, and feature-based allows for strong renewal visibility and pricing power, with over 39% agreements with longer than 12-month term lengths.

Source: Docusign Q1’26 Presentation

Dollar Net Retention (DNR) rose to 101%, not great but heading in the right direction, thanks to IAM upsells and more frequent customer success touchpoints. With over 1,100 enterprise customers over $300,000 ACV, Docusign is forming a high-ACV cohort that should propel platform growth into workflow areas like CLM, vendor management, and automation of compliance.

Finally, where everyone is chasing logos, Docusign is taking share out of existing accounts. Its multi-channel go-to-market, from digital to direct, enables land-and-expand movement within 1.7 million global customers. In addition to an expanding ecosystem of 500+ SIs and 140+ resellers, the omnichannel model reduces CAC and sustains GTM leverage.

It’s simply an argument for integrally embedded, AI-enhanced workflows that have a measurable impact throughout the org, rather than the lowest price or sexiest UI. In an environment where “AI” is tossed around by every SaaS provider, Docusign’s value proposition comes down to having AI that actually delivers because it’s learned where it makes the most difference: at the agreement workflow.

Margin Expansion, Cash Flow Power, and the Valuation Disconnect

Under the surface-level valuation grades, Docusign’s financials have a much rosier picture than most investors realize. Q1 FY26 recorded the fifth consecutive quarter of expanded non-GAAP margins, with a 29.5% operating margin and a 30% free cash flow margin. Subscription gross margins are stable at 84%, despite headwinds from cloud migrations.

Source: Docusign Q1’26 Presentation

Billings were at $739.6 million (+4% YoY), revenue grew 8% to $763.7 million, modest but steady amid post-COVID normalization. With IAM adoption due to pick up again during Q3 and Q4, management aimed for FY26 revenue at $3.151–$3.163 billion and billings up to $3.339 billion, anticipating low-double-digit growth despite FX-neutral headwinds.

Source: Docusign Q1’26 Presentation

Capital efficiency is another underappreciated lever. Using this quarter's $228 million FCF and $1.1 billion cash availability, Docusign is self-funding platform transformation and stepping up capital return. The board recently approved another $1.0 billion in growth for the share repurchase program; total available authorization is now $1.4 billion, or nearly 19% of the current market capitalization. This aggressive buyback mindset is remarkable for a transformational company: it shows confidence in cash generation and recognition of share undervaluation.

But the judgment of the market is clouded by trailing valuation measures. The banner GAAP forward P/E figure of 61.2x is distorted by non-cash charges and inflowing reinvestments. On a non-GAAP forward P/E basis, Docusign trades at 21.03, near the sector median of 22.44. Its PEG GAAP ratio of just 0.02 (relative to the sector median of 0.95) suggests that future growth is being enormously underappreciated relative to earnings power.

Correspondingly, EV/EBITDA (TTM) is 48.65, 185% above peers; however, by eliminating compressions associated with normalized future FCF compounding and stickiness off the platform, such premium compresses quickly. Run-rate annualized FCF at ~$900 million implies forward-looking EV/FCF at ~16x, which is attractive for a margin-expanding and strategically rejuvenated SaaS business.

The bottom line: valuation optics are obscured by trailing GAAP noise, but the business asserts itself with silent strength in cash flow growth, adoption, and platform scale. Even a rerating to 25x FCF would be supportable at a share price above $100, with 30–35% upside potential from here.

Risks: Execution, Adoption of IAM, and Macro Headwinds

Despite the intriguing transformation storyline, Docusign still experiences material execution risks. The IAM platform, uniquely differentiated, is itself a new product category that requires customer evangelism inside the firm, complex implementation, and redrafting of workflow, especially by legal and procurement groups. Delays in product maturation or customer enablement could derail upsell momentum and DNR growth.

Second, competitive risk from better-resourced competition, such as Microsoft or Google, that could embed contract workflows within their suite offerings, still poses an existential threat. Contract data sets and contract intelligence are now Docusign’s moats, but hyperscalers’ distribution muscle and bundling opportunities should not be underestimated.

Third, macro headwinds could soften enterprise purchase cycles, most notably in Europe and emerging regions where Docusign is focusing investment for direct growth. With 28% of revenue now going overseas, any geopolitical or currency disruption could affect billing visibility. Finally, valuation normalization depends upon sustained margin discipline. While Docusign marches forward with FY26 cloud migration, gross margin headwinds may persist, and stock-based compensation always represents a concern. Over $145 million in SBC was added back just to get up Non-GAAP EPS in Q1, a number that should be viewed with concern over dilution risk, even with offset buys.

Conclusion

Docusign is building an AI-native solution at the very center of enterprise workflows while hiding behind the outdated valuation prism. With Intelligent Agreement Management gaining increasing momentum and margin expansion compound, DOCU offers asymmetrical upside for those considering beyond headline multiples.

Copyleaks Report: https://app.copyleaks.com/report/3449rr0z7zzuymo7/preview?key=c22qztcxctzdoiwb&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

.png)

Get Started

Recommended Articles