TradingKey 2025 Markets Recap & Outlook | Top 10 Financial Events You Need to Know in 2025

TradingKey - 2025 can be described as a year of global asset breakout, with many assets undergoing a new round of market repricing. Here, we will review and reconstruct the ten key events that reshaped global asset pricing logic in 2025. This is not just a summary of the past, but also a lighthouse guiding us through the investment uncertainties of 2026.

I. Trump's Return to the White House: Tariffs and Deglobalization Reshape Supply Chains and Asset Pricing

Since his return to the White House in January, Donald Trump has implemented several policies, with the most profound impact on global assets stemming from the U.S.'s 'tariff stick'.

In 2024, total U.S. goods exports reached $2.06 trillion, while imports exceeded $3.26 trillion, resulting in a goods trade deficit of $1.2 trillion, a new historical high.

To reduce the massive trade deficit, Trump announced on April 2nd a 10% 'baseline tariff' on all trading partners. Over 60 countries and regions with significant trade deficits with the U.S. faced tariffs ranging from over 10% to 50%, with even higher 'punitive tariffs' imposed on some nations.

As the baseline tariff policy was implemented, global supply chains were forced to reconfigure. The market's anticipated 'transshipment trade' route—using Vietnam, Mexico, or India as intermediaries to circumvent high tariffs—was severely blocked by the Office of the United States Trade Representative. This strict regulatory crackdown directly pushed up the production costs of global end goods, compelling multinational corporations to accelerate the diversification of their capital expenditure strategies.

This policy combination triggered a fierce chain reaction in financial markets. Firstly, a resurgence in inflation expectations led to a rapid steepening of the U.S. Treasury yield curve early in the year, with a significant return of the Term Premium, causing the market to reprice the risk of 'long-term high interest rates'.

Secondly, despite the U.S. facing imported inflationary pressures, the anticipated reduction in the trade deficit due to tariffs, along with risk-averse sentiment, caused non-U.S. currencies to generally weaken, leading to a significant shift in the anchor of global asset pricing.

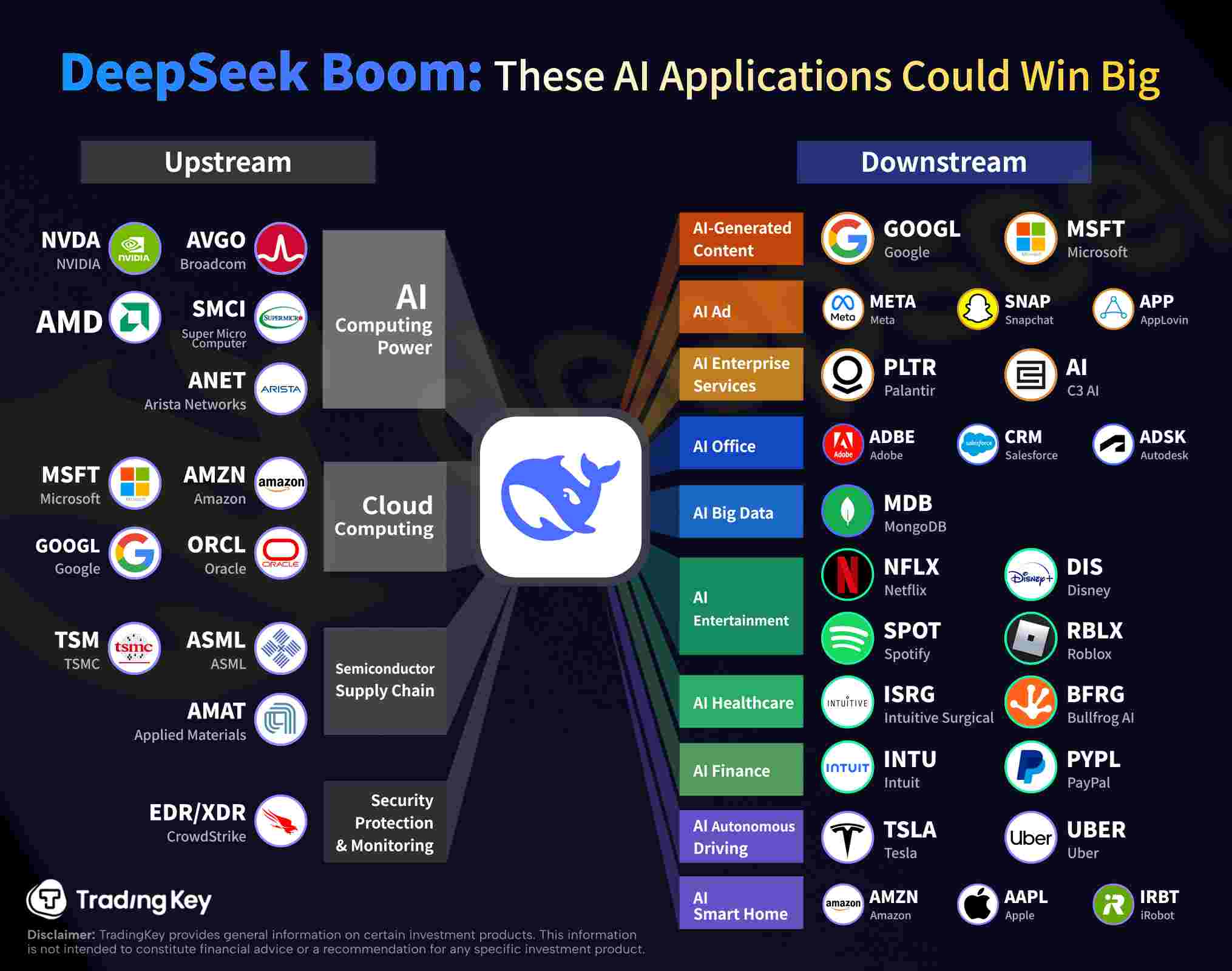

II. DeepSeek's Impact: Unveiling a New Theme of 'Low-Cost AI'

In early 2025, the release of DeepSeek-V3 and its subsequent R1 inference models became an unexpected 'black swan' in Silicon Valley. This Chinese AI unicorn, with its ultra-low Inference Cost and astonishing performance, stunned Wall Street and broke the monopoly of U.S. giants like OpenAI on the high-end large model narrative.

It demonstrated to the market that achieving Artificial General Intelligence (AGI) does not solely rely on stacking tens of thousands of H100 GPUs. Through extreme optimization of its MoE architecture and algorithmic innovation, DeepSeek slashed the API call price for an equivalent level of intelligence to one-tenth or even less than its competitors.

This event triggered a valuation re-evaluation in the SaaS sector on Nasdaq: investors began to realize that the moat for AI applications was no longer the models themselves, as models were becoming commoditized, and true value was returning to scenarios and data.

DeepSeek's ascent not only alleviated the 'computing power anxiety' of small and medium-sized developers but also compelled Silicon Valley giants to re-examine the cost-benefit ratio of their 'might-makes-right' approach.

It initiated a new theme of 'low-cost AI' in 2025, enabling the widespread penetration of AI Agents into vertical industries. From medical diagnostics to legal documentation, the popularization of AI was unexpectedly accelerated.

[Source: Compiled by TradingKey]

Recalling what we previously mentioned in our articles, on how DeepSeek models impact the AI industry chain, most of these industry chain developments have now been validated by the market.

III. AI Arms Race Intensifies, Multiple Tech Giants Reach New Market Cap Highs

Driven by deep-seated anxiety over 'falling behind' in the new wave of technological innovation, 2025 witnessed the largest capital expenditure surge in human history. Nvidia, Microsoft, Amazon, Google, and Meta collectively increased their AI-related capital expenditures to unprecedented levels that year.

Wall Street was initially alarmed by this no-holds-barred spending, with skepticism primarily focused on when the 'ROI (Return on Investment)' would materialize.

However, with the disclosure of earnings reports, the market discovered that these giants were absorbing these expenditures through cloud business growth and improved internal efficiencies. This 'winner-take-all' Matthew effect propelled the market capitalization of several tech giants to new highs in 2025, with Apple and Microsoft alternately surpassing the $4 trillion mark.

The Nasdaq 100 Index's weighting further concentrated towards the leading companies, and the market became completely bifurcated into 'AI infrastructure owners' and 'other companies'.

To support the continuously expanding demand for computing power, data centers are evolving from mere server infrastructure into heavy-asset energy systems characterized by gigawatt (GW)-scale power consumption.

Around this trend, power-supplied data centers and advanced liquid cooling technologies rapidly became central themes of interest in capital markets in 2025, also giving the utilities sector an unexpected 'shadow beneficiary' status amidst the AI investment wave.

IV. U.S. Stocks See V-Shaped Recovery and New Highs After Significant Retracement

Constrained by ongoing U.S. tariff impacts, U.S. equities experienced a 'flash bear market' from February to April this year. The Nasdaq Index alone plummeted over 25%.

This tariff shift quickly struck at a core market assumption: that corporate profit margins could continuously expand through economies of scale amid the booming AI investment landscape.

The return of tariffs meant a triple shock occurred simultaneously:

- Rising input costs: Directly pressuring capital-intensive industries such as technology hardware, servers, and data center equipment;

- Repricing of inflation stickiness: Tariffs were seen as 'tax-like inflation,' eroding market confidence in rapid interest rate cuts;

- Surging global supply chain uncertainty: Investors began to re-evaluate the earnings visibility and valuation premiums of multinational technology companies.

It was against this backdrop that the Nasdaq Index ultimately experienced a rapid correction over several months. This meant that the so-called 'flash bear market' was essentially more a concentrated repricing of policy risk than a repudiation of the AI narrative itself.

The market's subsequent rapid recovery was not due to the complete disappearance of macro risks, but rather the reaffirmation of two key points:

- Tariff risks largely remained at the policy negotiation level and did not immediately translate into substantial downward revisions in corporate orders and capital expenditures in the short term;

- Performance guidance from core hardware manufacturers like Nvidia indicated that AI investment demand possessed significant absorption capacity for price and cost impacts.

With policy uncertainty marginally easing and corporate earnings expectations stabilizing, risk capital that had previously withdrawn due to tariff and interest rate concerns rapidly flowed back, driving the market to complete a typical V-shaped reversal.

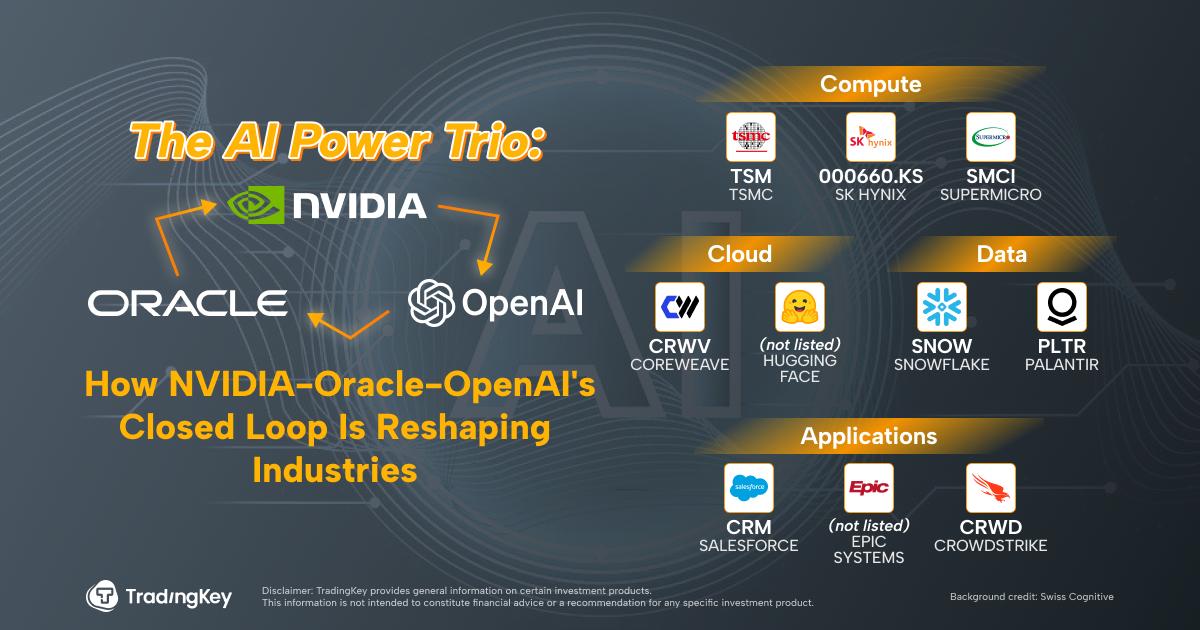

V. OpenAI–Oracle–Nvidia 'AI Closed Loop' Fuels Bubble Debate

As OpenAI continued to iterate on the model layer, Oracle established deep ties in cloud infrastructure, and Nvidia maintained its absolute dominance in computing power, an ecosystem dubbed the 'AI closed loop' by the market gradually took shape.

This high degree of synergy, spanning from models and computing power to cloud services, significantly boosted commercialization efficiency but also ignited intense debate about valuation bubbles.

Critics argued that the market was paying a premium for a decade's worth of future growth, while supporters contended that AI, as a general-purpose technology, was still in its early stages of penetration. The 2025 debate yielded no definitive answers, but it was clear that the volatility of AI-related assets rose significantly, with any signals regarding regulation, technological bottlenecks, or demand slowdowns being quickly amplified.

VI. Gold Surpasses $4,000/Ounce for the First Time

In 2025, gold prices historically breached $4,000 per ounce, revising long-held market perceptions. This surge in gold was primarily driven by the confluence of escalating geopolitical tensions, continuously expanding fiscal deficits in various countries, and growing concerns about the stability of monetary systems.

In other words, this gold rally largely reflected the market's pricing of 'future uncertainty.' Whether it was war risks, friction in international relations, or recurring debt issues in major economies, investors began to rethink which assets were more trustworthy in extreme circumstances.

From a capital flow perspective, this trend was very clear. Central banks globally, especially those in emerging markets, continuously increased their gold reserves, seeking to reduce reliance on a single currency system. Concurrently, financial investors also boosted their allocations via gold ETFs and derivative instruments, transforming gold from a 'buy only in times of crisis' asset into one increasingly integrated into long-term asset allocation frameworks.

Notably, the backdrop for gold's rally was not 'typical.' Inflation was not out of control at the time, and real interest rates fluctuated. This indicates that gold's role is evolving—it is no longer merely a hedge against inflation or short-term crises, but is increasingly seen by investors as a critical asset for hedging against systemic risks, policy uncertainties, and long-term credit issues.

For average investors, the signal conveyed by gold breaking $4,000 was not 'should I still chase it now,' but rather: in an era of recurring uncertainty, the market is redefining what truly constitutes a 'safe asset'.

VII. U.S. Federal Government Shutdown and Budget Stalemate

In 2025, the U.S. federal government once again faced a partial shutdown due to failed budget negotiations, lasting for a record duration. Simply put, the two parties in Congress could not agree on 'how to spend money and where money comes from', leading to some government agencies being forced to shut down, with civil servants experiencing delayed paychecks and some public services suspended.

From a market reaction perspective, such events no longer trigger panic as they did in the past. U.S. equities and Treasuries showed limited short-term volatility, with investors largely adopting a 'seen it all before' attitude. However, this does not mean the issues are nonexistent. Multiple rating agencies and research institutions explicitly pointed out that frequent political wrangling is eroding the credibility of U.S. fiscal governance, with the impact leaning more towards the medium to long term rather than being immediately reflected in asset prices.

For the bond market, this stalemate did not immediately trigger a sell-off, but the trend of long-term interest rates remaining relatively high persisted. The market gradually accepted a reality: U.S. Treasury bonds are still widely held not because of efficient political operations, but because the dollar system, market size, and liquidity still offer 'no alternative'.

For average investors, the signal from this event was clear—U.S. assets remain important, but their 'sense of security' stems more from market structure than from political stability itself. This is why, even amidst short-term calm, long-term risk premiums are quietly increasing.

VIII. Bitcoin Retraces Significantly After Reaching New Highs

In the first half of 2025, driven by continuous capital inflows into Bitcoin spot ETFs, Bitcoin prices once again reached new historical highs. The influx of substantial traditional capital created a perception among many investors that Bitcoin had seemingly 'been embraced by the mainstream market'.

However, the market quickly reversed afterward. With renewed regulatory uncertainty, concentrated profit-taking by early investors, and a decline in overall market risk appetite, Bitcoin experienced a significant retracement, with volatility markedly increasing.

This price movement brought greater clarity to the market's perception of Bitcoin. It was no longer merely a niche speculative tool but increasingly resembled a highly volatile 'macro asset'—extremely sensitive to global liquidity, dollar strength, and market sentiment. Capital flows in and out rapidly.

Notably, the participation of institutional capital did not make Bitcoin 'more stable.' On the contrary, price reactions remained sharp during liquidity shifts. This indicates that Bitcoin still lacks a widely recognized stable value anchor, and its characteristic cyclical surges and dips have not fundamentally changed.

For average investors, this event served as another reminder: Bitcoin should not be simply understood as a 'safe haven' or a 'stable asset.' It acts more like a tool that amplifies market sentiment, rising rapidly in favorable conditions and retracting just as swiftly in adverse ones.

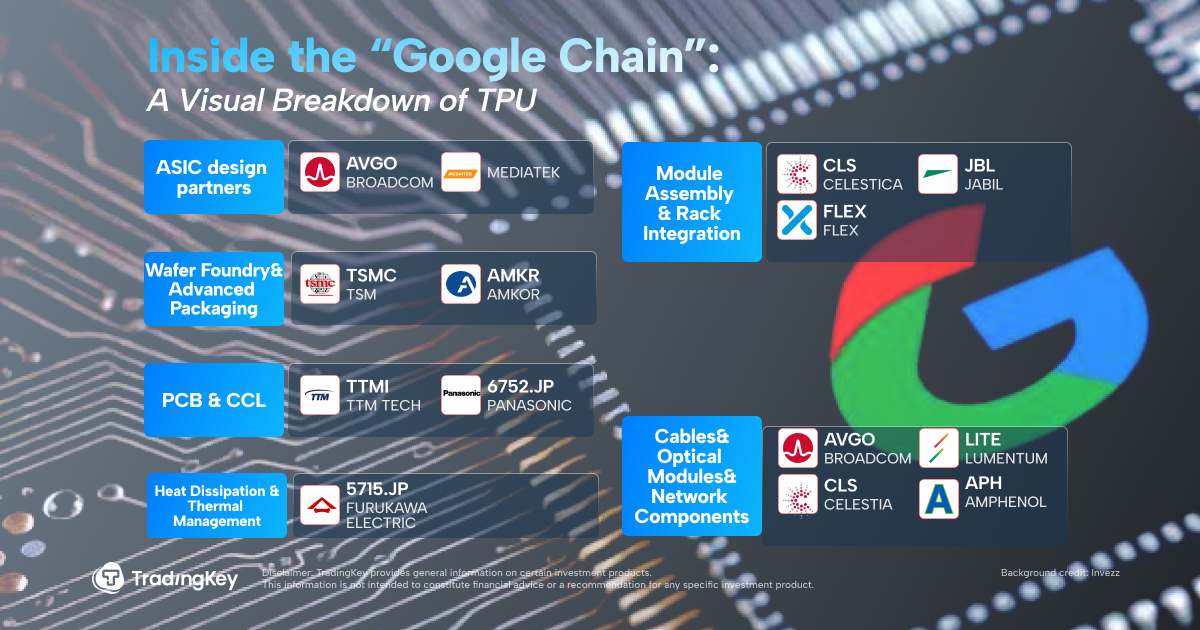

IX. Google Releases Gemini 3, 'Google Chain' Becomes New AI Narrative

Google's launch of Gemini 3 in November 2025 was seen as a critical counterattack in the AI race. Unlike previous instances, Google no longer solely emphasized model performance but systematically showcased the synergistic effects of the 'Google Chain' across its search, advertising, and Android ecosystems.

This narrative quickly gained market recognition. Investors began to re-evaluate Google's unique advantages in data, distribution channels, and commercialization pathways.

The new 'Google Chain' narrative brought significant market recognition to related industry companies, while also posing substantial challenges to the competing Nvidia chain. Industry chains associated with both experienced considerable volatility under market scrutiny.

Despite facing competitive pressures in the short term, the 'Google Chain's' 'ecosystem AI' emerged as a new valuation support logic.

X. Fed Cuts Interest Rates for Third Time This Year and Initiates RMP Bond Purchase Program

Against a backdrop of marginally slowing economic momentum, the Federal Reserve implemented its third interest rate cut in 2025. However, this round of policy adjustments was not officially defined as the 'start of a new easing cycle.' Diverging from past practices, the Fed, while cutting rates, explicitly stressed that policy would remain 'restrictive yet more flexible,' aiming to strike a balance between preventing an economic slowdown and avoiding excessively loose financial conditions.

The direct cause of the policy shift was the gradual emergence of structural deceleration signs in the U.S. economy. Consumer spending continued to cool in a high-interest-rate environment, corporate capital expenditures became more cautious, and while the job market did not significantly deteriorate, job vacancy rates and wage growth had fallen for several consecutive months.

Concurrently, although core inflation metrics had not yet fully returned to the 2% policy target, their downward trend was more widely acknowledged within the Federal Reserve.

Notably, the Federal Reserve simultaneously implemented a RMP (Reserve Management Purchase) bond program, purchasing approximately $40 billion in short-term U.S. Treasury securities monthly, aimed at easing short-term funding pressures. This was viewed as a form of 'stealth quantitative easing,' primarily impacting short-term interest rates and market supply-demand balance.

Chairman Powell repeatedly emphasized in the press conference that this was not Quantitative Easing (QE), but rather an effort to maintain ample reserve levels in the banking system and prevent turbulence in the repurchase market.

Looking back at the top ten financial and economic events of 2025, it's evident that the year did not witness a landscape-altering crisis, nor did it usher in a new phase of broad prosperity. More often, the market continuously switched between different themes: tariffs, AI, and monetary policy took turns in the spotlight, investment logic changed frequently, and uncertainty gradually became the norm.

For many investors, the most obvious change was that the market became 'harder to navigate.' Indices sometimes rose, but profit-making opportunities were uneven; while some assets strengthened consistently, many others repeatedly fluctuated. This implies that simply observing index movements is increasingly insufficient to reflect the true investment experience.

From a longer-term perspective, 2025 did not appear to be the beginning of a new growth cycle, but rather a phase of adjustment and transition. The global economy continued to operate, yet growth was not broadly accelerating but supported by a few sectors; AI, while offering long-term imaginative potential, also amplified short-term volatility, making market sentiment more prone to significant swings. Concurrently, monetary policy no longer solely provided downside support, with fiscal and geopolitical factors becoming new sources of instability.

In such an environment, the focus of investment is shifting. Rather than betting on a single trend, investors increasingly need to focus on whether assets are robust, cash flows are reliable, and if they can withstand market volatility.

While 2025 may not have offered a clear direction, it reminded the market that in an era of faster change and greater divergence, establishing more robust investment approaches might be more crucial than chasing hot trends.

Recommended Articles