Gold and Silver Prices Rebound Strongly: Short-Term Recovery or Start of a New Bull Market?

TradingKey - Precious metals rebound strongly after sharp volatility as the market faces a pivotal directional choice.

Following a two-day rout, the precious metals market staged a strong rebound on Tuesday. On the 3rd, gold and silver futures prices in New York closed significantly higher, as market sentiment showed clear signs of recovery. Investors are reassessing the panic previously triggered by policy factors and are actively seeking "buy-the-dip" opportunities.

At the close, gold futures for April delivery on the COMEX rose 6.07% to $4,935.00 per ounce, marking the largest single-day gain since 2025; silver futures for March delivery surged 8.17% to $83.301 per ounce. Subsequently, in overnight trading, gold and silver prices continued to recover, with gold prices returning above $5,000 per ounce.

Last Friday, gold prices ( XAUUSD) recorded their largest single-day drop since 2013, while silver ( XAGUSD) saw its steepest single-day decline in history. Market sentiment continued to deteriorate on Monday, pushing gold prices even lower.

Analysts believe this period of intense volatility in precious metals was driven primarily by two short-term factors: first, a periodic rebound in the U.S. Dollar Index, which weakened gold's role as an alternative safe haven; and second, the Chicago Mercantile Exchange (CME) raising margin requirements for precious metals futures, which increased the cost for long positions and triggered a passive contraction in liquidity.

Following historic selling pressure and volatility, the gold and silver markets are at a critical turning point. Whether this marks the start of a new upward cycle or a prolonged period of weak consolidation remains to be seen.

Concerns Over Short-Term Volatility in Precious Metals

According to a report from Goldman Sachs ( GS ), the recent single-day declines in COMEX gold and silver contracts broke records spanning nearly 40 years, representing the most intense sell-off since the early 1980s.

Despite prices bouncing back from extreme lows, overall volatility remains elevated. The report also highlighted that liquidity in the gold and silver options market briefly dried up, further magnifying trading risks and price instability.

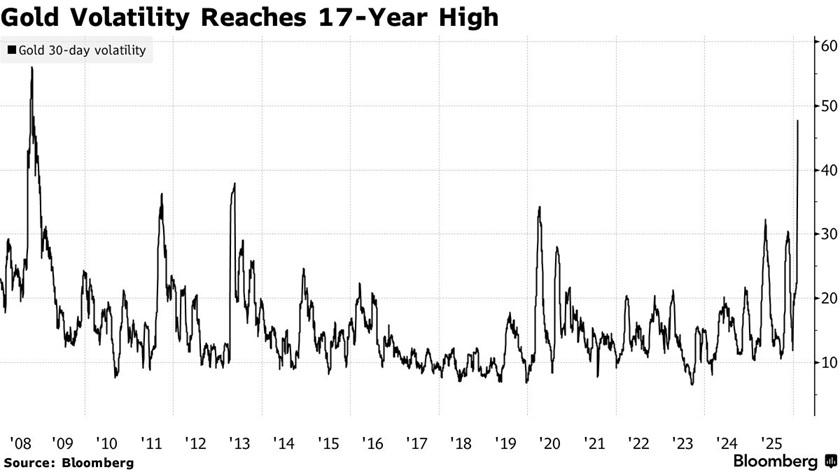

According to a key measure of volatility, gold price volatility has reached its highest level since the peak of the 2008 global financial crisis.

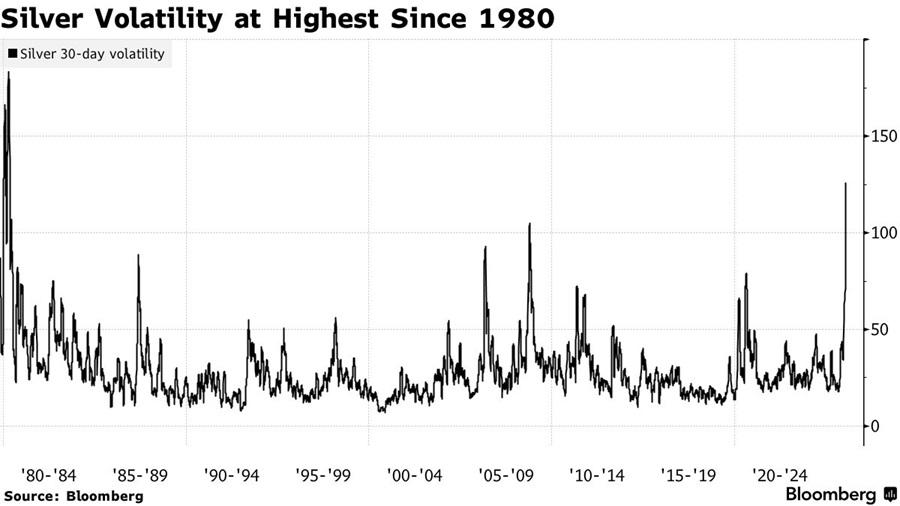

Meanwhile, the level of turbulence in the silver market is approaching historic extremes not seen since 1980.

Amid the current landscape of global financial uncertainty, safe-haven sentiment, and policy maneuvers, the precious metals market is likely to remain in a state of high volatility in the short term.

Institutions Maintain a Long-Term Bullish Outlook on Gold

Despite the recent price swings, several major international financial institutions remain firmly bullish on gold’s long-term performance, generally agreeing that the short-term sell-off has not undermined its core investment thesis.

Analysts at Deutsche Bank ( DB) noted that sharp declines like the current one are more likely triggered by short-term catalysts rather than fundamental shifts. While a recent uptick in market speculation is evident, it alone does not explain such a severe price correction.

They stated: "The scale of the downside in gold and silver has exceeded the significance of the triggers themselves. Looking at overall capital flows, the medium-to-long-term appetite for precious metals remains solid among central banks, institutions, and individual investors alike."

Deutsche Bank emphasized that the current macro backdrop supporting gold is significantly different from the prolonged periods of weakness in the 1980s or 2013. In an environment of persistent global uncertainty and frequent geopolitical tensions, the conditions for a sustained downward trend in gold prices are absent. Consequently, the bank reaffirmed its year-end gold price target of $6,000 per ounce.

Struyven, a commodities researcher at Goldman Sachs, maintained his forecast for gold to reach $5,400 per ounce by the end of 2026. He noted that the three core assumptions supporting his prediction remain valid: central banks purchasing an average of 60 tons of gold per month, the Federal Reserve expected to cut rates twice this year, and stable levels of gold allocation from private capital.

Struyven further emphasized that fiscal sustainability issues in developed economies are unlikely to be fully resolved before 2026. Given that gold's current share in traditional investment portfolios remains low, there is significant potential for asset reallocation into the gold market, with overall price risks tilted to the upside.

JPMorgan ( JPM) expressed similar views. Yuxuan Tang, Head of Macro Strategy for Asia at JPMorgan Private Bank, pointed out that while the recent pullback was sharp, it constitutes a technical correction.

"We have seen classic buy-the-dip behavior in the market, which is a common technical reaction when asset prices fall near 20%," he noted. He emphasized that this volatility flushed out short-term speculative bubbles, helping the market return to fundamental analysis. "The nomination of Warsh as Fed Chair has not changed our long-term bullish stance on gold."

JPMorgan expects gold prices to range between $6,000 and $6,300 per ounce by 2026, supported by adjustments in policy expectations, shifts in asset allocation behavior, and a sustained long-term demand for safe-haven assets.

Silver: Industrial Support Persists Amid High Volatility

Compared to gold, silver's recent market volatility has been even more extreme, exhibiting a classic "rollercoaster" trend. This is primarily due to silver's relatively smaller market size, greater price swings, and higher retail participation. Consequently, silver is more sensitive than gold to short-term shifts in sentiment and unexpected events.

eToro market analyst Zavier Wong noted: "In the short term, the massive volatility in silver is closely tied to speculative positioning. Because retail participation is significantly higher in silver than in gold, price movements are often more susceptible to short-term sentiment."

However, he also stressed that attributing all volatility solely to retail speculation is "overly simplistic," as silver possesses solid tangible demand within global industries, particularly with rapid growth in applications for data centers and AI infrastructure.

Beyond its financial properties, silver's industrial demand profile provides significant support for its long-term price. A research report released this January predicts a structural supply-demand gap in the silver market over the next decade. As solar PV installations continue to grow and battery technologies shift toward more silver-intensive designs, annual global silver demand could reach 48,000 to 54,000 tons by 2030, while supply is projected to reach only about 34,000 tons. This suggests that only about 62% to 70% of global silver demand may be effectively met.

Specifically, silver consumption in the solar industry is expanding rapidly. The study estimates that by the end of this decade, the PV industry will consume between 10,000 and 14,000 tons of silver annually, potentially accounting for up to 41% of total global supply. This provides the silver market with clear and robust mid-to-long-term fundamental support.

Wong concluded: "The real issue isn't whether silver has value support, but that it often exhibits price surges that outpace fundamentals during bullish phases. Current market action is more a natural correction of silver's rapid short-term gains rather than a fundamental change."

Recommended Articles