A Few Things You Need to Know About the Gold and Silver Plunge

TradingKey - January 30, Eastern Time, Silver (XAGUSD) and Gold (XAUUSD) experienced their largest decline since the Hunt brothers' attempted market manipulation in 1981. As of press time, gold and silver have yet to stop their slide. In this precious metals bull market, the rallies in silver and gold have become "distorted," which we characterize as a "precious metals bubble." Such gains are unusual and unsustainable for safe-haven assets, as they are largely driven by speculative capital.

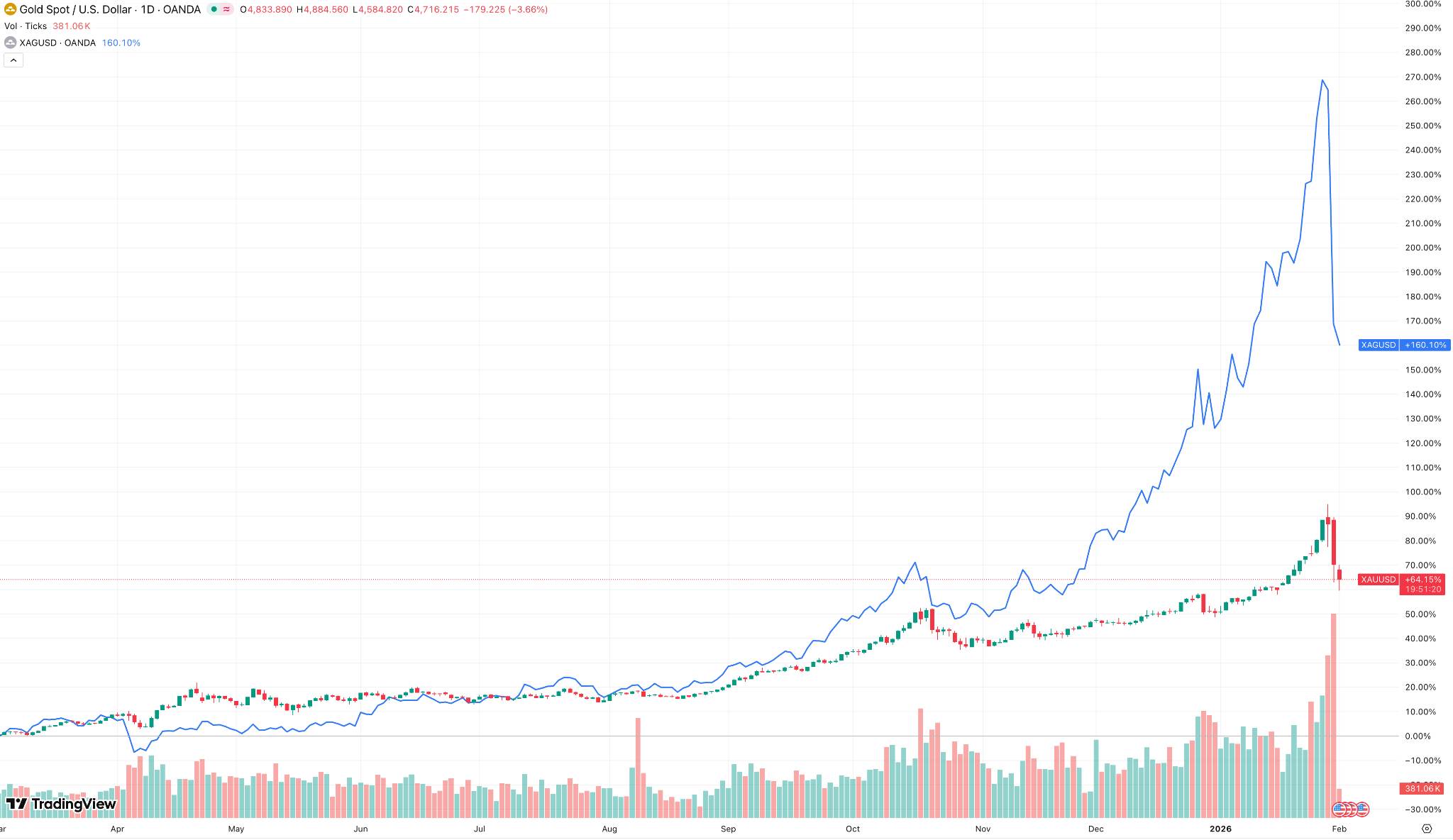

[Gold and silver fell sharply after massive gains, Source: TradingView]

Here are a few things you need to know:

What fueled the rise in gold and silver?

First, the loosening of macro pricing anchors served as the fundamental premise for the rally in gold and silver.

Under the traditional framework, gold is highly negatively correlated with U.S. real interest rates. However, the current rally has transcended these limitations, shifting toward a loss of market confidence in future policy paths.

Markets are questioning U.S. fiscal sustainability—expectations of "passive easing" of monetary policy in a high-debt environment continue to erode the credibility of long-term real interest rates as a pricing anchor.

Markets have realized that high interest rates may only be a temporary tool, naturally re-elevating the pricing basis for gold's strong safe-haven attributes. This rally is not a reaction to a single rate cut, but a reassessment of the institutional credit discount rate.

Second, structural changes in global asset allocation logic have amplified the demand for precious metals. Against a backdrop of historically high equity valuations and the long-term erosion of real bond returns, traditional "stock-bond dual allocation" is failing.

Large institutional investors, particularly sovereign wealth funds, long-term capital, and insurance funds, have begun to increase their allocation weights to "assets without counterparty risk." Consequently, gold is no longer just a safe-haven tool but is gradually returning to its role as a "macro risk hedging tool." In this process, silver's performance has been notably more elastic; its upward logic is driven by gold but also possesses its own unique amplification mechanism. Compared to gold, the silver market is smaller with more fragile liquidity, while possessing both financial and industrial attributes.

When capital begins to rotate from "defensive precious metals" to "offensive precious metals," silver often becomes the preferred asset. Especially while industrial narratives like new energy and photovoltaics remain intact, expectations for industrial demand provide additional fundamental support for silver, causing it to exhibit significantly higher beta characteristics than gold during rallies.

From a financial market structure perspective, there was a widespread underweight or even bearish sentiment before gold and silver began their ascent. Once prices broke through key technical and psychological levels, capital that had been on the sidelines or in defensive positions was forced to chase prices higher. This rally, driven by position squaring, is often accompanied by simultaneous inflows into futures and ETFs, giving the price increase a "non-linear characteristic." Silver is particularly emblematic of this stage; any marginal capital inflow can trigger violent volatility due to limited market depth.

Within the context of the global landscape, geopolitics is not merely short-term noise but the logical support for the safe-haven attributes of precious metals. Whether it is great power competition, regional conflicts, or the fragmentation of trade and financial systems, these factors continue to undermine the foundation of global trust in a single currency system.

In this context, gold is being redefined as a "neutral store of value." This shift in perception is not reflected in prices daily, but once collectively accepted by the market, its impact is often profound and difficult to reverse.

What historical events have driven rallies in gold and silver?

The Hunt brothers event is the most classic historical case of silver prices being distorted by the direct force of capital. In the late 1970s, amid high inflation and wavering confidence in the U.S. dollar, the Hunt brothers attempted to control the supply of circulatable silver by hoarding physical silver on a large scale and establishing massive long positions in the futures market to drive up prices.

In a short period, silver experienced a surge far exceeding its fundamentals and significantly outperformed gold. However, when the exchange raised margin requirements and restricted trading, the leveraged structure collapsed rapidly, and prices plummeted, ending in a historic crash.

This event served as a warning to capital markets: when precious metal rallies are driven primarily by concentrated capital and leverage rather than long-term allocation demand, the gains are often unsustainable, and the pullbacks are extremely severe.

When will the current decline in gold and silver end?

First, we must state our view: given the long-term allocations by central banks and the continued instability of macro factors, we remain bullish on gold. However, considering the current sentiment peak transition and the fact that speculative capital has not yet been flushed out, there is still no clear entry point in the short term.

Gold is expected to stabilize in the short term due to the backing of national governments. However, the long-term impact of macro factors must also be considered. With Kevin Warsh being considered for Fed Chair, markets interpret this as a hawkish shift, which has to some extent raised expectations for monetary policy to maintain a relatively tight stance. If expectations of cooling inflation continue to strengthen, the pressure on gold will persist.

Due to the presence of significant leveraged capital and the impact of speculative sentiment, we believe the downward trend for silver remains intact from a long-term perspective given its current overvaluation. We do not see significant investment value at these levels, as industrial value and safe-haven logic fail to justify such gains. Furthermore, silver lacks government backing, and until the market returns to rational fundamental analysis, we do not consider silver a favorable investment candidate.

Therefore, the medium-to-long-term logic for gold has not been completely undermined by the short-term correction; its price is more likely to enter a phase of consolidation within a high range, awaiting new macro variables for re-pricing. In contrast, silver, which lacks official reserve status and is more sensitive to liquidity, continues to face significantly higher volatility and drawdown risks than gold, making it harder to recover in the short term.

What strategies should we adopt in light of the decline in gold and silver?

Given the highly uncertain downward trend in gold, we recommend that non-professional investors use a dollar-cost averaging strategy on the "left side" of the trade, waiting for a valid signal of bottoming and stabilization before entering with light positions. We prefer that investors engage in value investing based on precious metal fundamentals rather than short-term scalping.

Given that silver's recent gains were excessive, we believe bears currently have the upper hand, making it unsuitable for opening long positions. With significant short-term volatility remaining, we advise against investors opening large positions. From a fundamental perspective, silver remains relatively overvalued.

Recommended Articles