May Jobs Data Exceed Expectations. U.S. 10-Year Treasury Yield Returns to 4.5% Level, But Citi Says Nonfarm Impact on Stock Market Has Dropped Sharply.

TradingKey - On June 2, concerns that the war in Iran would continue to fuel inflation, combined with the ADP report (the "private payrolls" data) beating market expectations, drove oil prices and U.S. Treasury yields higher while stocks fell.

The U.S. labor market has shown unexpected resilience, but beneath the surface, persistent high inflation is eroding real household income, pushing the personal savings rate to a nearly four-year low. This paradoxical economic backdrop has left traders attempting to bet on the Federal Reserve's rate path in a quandary.

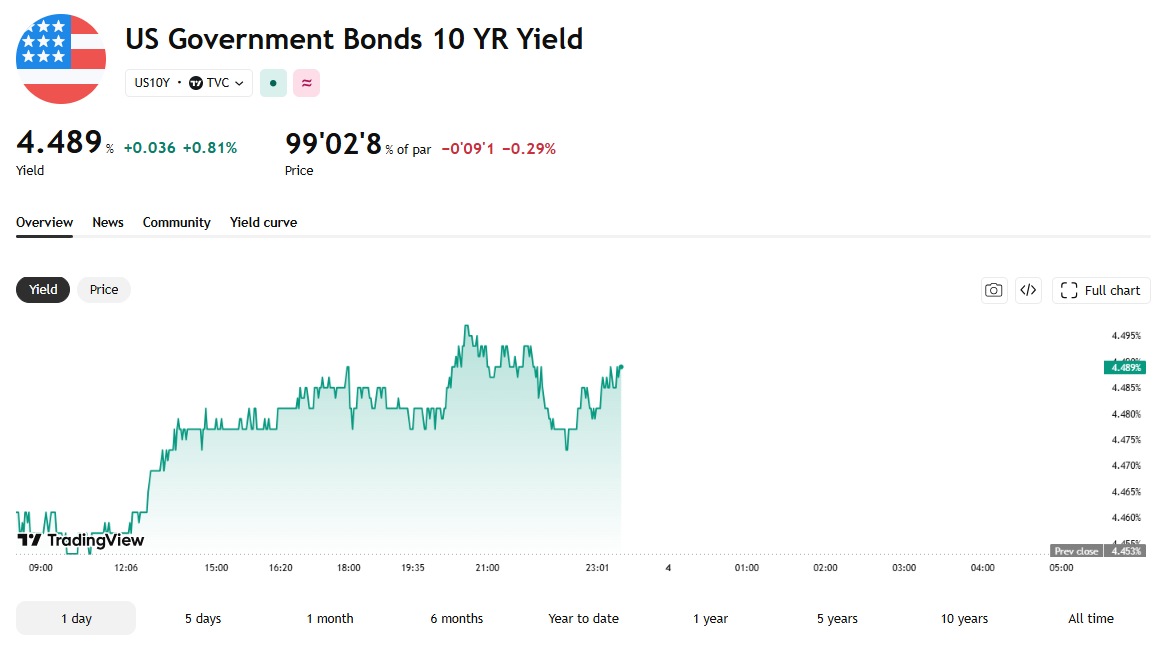

Following the ADP release, the 10-year U.S. Treasury yield, a key benchmark for mortgage rates, hit 4.499%; the 2-year yield, seen as a bellwether for short-term Fed rates, reached 4.093%. The 30-year yield touched 4.997%.

[Source: TradingView]

This shifts the market's focus to this Friday's non-farm payrolls report, where expectations are for 85,000 jobs to be added. The unemployment rate is likely to remain steady at 4.3%, while average hourly earnings are expected to rise 0.3% month-over-month.

If U.S. employment data remains robust, market pricing for the Fed's rate path will tilt further hawkish. Valuation pressures on high-multiple tech sectors and AI concept stocks will then inevitably become the central market conflict.

Notably, alternative views have emerged: driven by escalating geopolitical tensions, the surge in oil prices is sparking a new wave of inflation fears. This is gradually replacing jobs data as the core variable influencing Fed policy expectations and market performance.

Citi noted that the options market is anticipating an unusually muted reaction to Friday's payrolls data, with bets implying a move of just ±0.6% for the S&P 500. This is below the 0.7% average actual volatility recorded on payroll days over the past year, making it potentially one of the quietest payroll sessions in months.

Recommended Articles