TSMC Has a Monopoly on Making AI Chips. Here's Why This Stock Could Be the Safest Bet in the $700 Billion Capex Boom.

Key Points

Much of big tech's 2026 spending will go toward building data centers and expanding cloud capabilities.

Taiwan Semiconductor Manufacturing Company (TSMC)'s efficiency and scale make it the go-to for manufacturing advanced AI chips.

TSMC is increasing its spending plans to accommodate increased demand.

- 10 stocks we like better than Taiwan Semiconductor Manufacturing ›

Although artificial intelligence (AI) technology itself isn't new, the popularity of AI apps and tools has thrown it fully into the mainstream. And in true big tech fashion, where there's an increase in eyeballs, there's an increase in their spending.

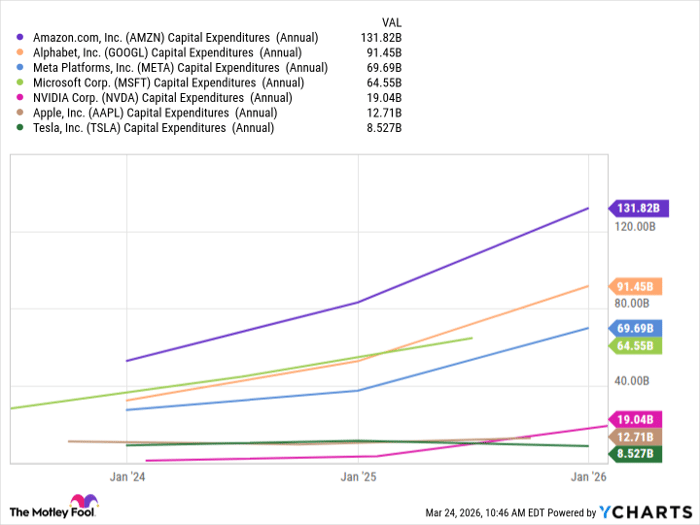

Over the past few years, major hyperscalers -- companies like Microsoft, Amazon, and Alphabet that power a lot of the digital world -- have spent billions building out their AI infrastructure. It seems these checks are only going to get bigger, too. Major tech companies are expected to spend around $700 billion on their AI infrastructure in 2026 alone.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

However, as hundreds of billions are being spent, the safest bet isn't the company with the best chatbot or productivity tools. It's Taiwan Semiconductor Manufacturing Company (NYSE: TSM), also known as TSMC.

Image source: The Motley Fool.

It all comes back to TSMC

TSMC is the world's largest semiconductor (chip) foundry. Instead of making chips for general sale that companies can buy in stores or online, semiconductor foundries manufacture the physical chips that other companies design. For example, Apple designs the chips it needs for its iPhones, but TSMC is the one who brings them to life.

You may wonder why these major tech companies don't just manufacture their own chips, but it's not that easy. Manufacturing chips (especially advanced ones) requires a ton of specialized talent, highly advanced machinery, and years of experience. For almost every tech company, it's much simpler and cheaper to let an expert like TSMC handle it.

TSMC has a 72% market share in the pure-play foundry market, but it has a virtual monopoly in making AI chips. The latter is why it's the safest bet in the ongoing AI boom.

AI as we know it today would suffer without TSMC

To understand TSMC's importance in the AI ecosystem, it's helpful to work backwards, starting with the AI apps and tools people interact with daily. For those tools to be effective, they need to be trained on tons of data. This amount of data can't be stored in traditional ways; it requires huge data centers with a lot of different hardware filled with various chips.

The importance of those chips is why a company like Nvidia -- which designs GPUs critical to processing lots of info -- saw a historical explosion in business and market cap and is now the world's most valuable public company.

Without TSMC's expertise, effectiveness, and scale, there's a strong case to be made that AI as we know it today would be less advanced. It's why companies are willing to pay a premium for TSMC's services rather than go with competitors, and why it continues to put up impressive financial results.

In 2025, TSMC made $122.4 billion in revenue, up nearly 36% from 2024 and well over double what it made five years ago. Its gross and operating margins also increased by 3.8% and 5.1% year over year, respectively, highlighting its pricing power, knowing companies need it.

The expected spending from AI hyperscalers

Goldman Sachs predicts AI infrastructure spending will exceed $500 billion in 2026, potentially reaching $700 billion if it aligns with peak telecom investment spending in the 1990s. The majority of this spending will come from AI hyperscalers (like the "Magnificent Seven" stocks) building out data centers and other infrastructure needed to expand their cloud capabilities.

The last thing these companies want is to be left behind in the AI race, and they're willing to spend to ensure it doesn't happen. As Goldman Sachs noted in its report, "supply bottlenecks or investor appetite" are more likely to slow down spending than cash concerns.

AMZN Capital Expenditures (Annual) data by YCharts

All of this spending won't be going toward AI chips, but a decent amount will inevitably find itself in the hands of chip designers like Nvidia and, in turn, TSMC. The company is also preparing to take on increased demand and has upped its 2026 spending plans. It expects its capital budget to be between $52 billion and $56 billion in 2026, well over the $41 billion it spent in 2025.

While major tech companies fight it out on the consumer side, TSMC is as well positioned as any company in the AI ecosystem.

Should you buy stock in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $497,659!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,095,404!*

Now, it’s worth noting Stock Advisor’s total average return is 912% — a market-crushing outperformance compared to 185% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 26, 2026.

Stefon Walters has positions in Apple, Microsoft, and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Taiwan Semiconductor Manufacturing, and Tesla and is short shares of Apple. The Motley Fool has a disclosure policy.

Recommended Articles