Coherent (COHR): In this round of AI optical interconnects, which deserves more attention, it or LITE?

Over the past month, almost everyone’s attention has been hijacked by the war in Iran: oil prices, shipping routes, the Middle East situation have been all over the screens every day. But if you rewind a bit further, you may or may not recall another piece of news that is highly relevant to AI infrastructure: Jensen Huang dropped 4 billion dollars in one go on optical interconnects, with 2 billion going to Lumentum and another 2 billion to a company called Coherent.

In the previous article we already took Lumentum (LITE) apart in detail, so why is Coherent qualified to stand on equal footing with it? On the surface, the news looks like Nvidia split 2 billion each between two independent companies, but once you look at it from the perspective of the industry value chain, the relationship is not that simple. In quite a few products, Coherent is the customer while LITE is one of its key suppliers, which is something many people actually don’t realize. Precisely because of this, while LITE is certainly important, if you casually lump COHR together as just another AI optical‑interconnect concept stock similar to LITE, you will completely miss its true market positioning, development path, and its very different risk‑return profile.

What kind of company is Coherent?

Coherent was originally called II‑VI Incorporated, a compound semiconductor company founded in Pennsylvania that makes materials like InP, SiC, and GaAs, supplying various lasers and optical devices—a classic materials‑driven origin story. Its first real leap came in 2019, when II‑VI completed the acquisition of Finisar for about 3.2 billion dollars. Finisar was then one of the world’s largest optical module manufacturers, with a complete transceiver product line and manufacturing system. This acquisition let II‑VI step from selling materials into selling transceivers, and it began supplying optical modules directly to data centers.

In 2022, II‑VI spent another 6.56 billion dollars to buy the old Coherent in its entirety, an industrial‑laser leader in CO₂ and fiber lasers whose customers include carmakers, metal processing firms, and semiconductor equipment vendors. After the deal closed, II‑VI simply rebranded itself, adopting the acquired company’s name, which gave us today’s Coherent Corp. To sum up, Coherent today mainly has three business segments: materials, optical modules, and industrial lasers. It sounds very complete, but the benefits and costs of stitching this together are all written on the balance sheet: the two big acquisitions left it with more than 5 billion dollars of debt. Before 2023, Coherent had to shell out over 200 million dollars of interest every quarter, which made the EPS numbers look ugly relative to what the operations could have delivered, so naturally the stock underperformed many asset‑light optical‑communications peers.

A new story started in 2023, when management kicked off a slim‑down and deleveraging campaign by selling non‑core assets and cutting capital expenditures. In August 2025, the company sold its aerospace and defense business to Advent for about 400 million dollars and used all the proceeds to pay down debt, and around the same time it disposed of the Munich industrial‑tools asset. With a few decisive cuts, it both generated real cash flow and carved out lower‑margin, non‑core businesses. By the end of 2025, COHR’s net leverage had dropped from more than 4.5 times right after the acquisitions to about 2 times. We will get back to what this shift means when we talk about the financials. For now, let’s first lay out the full picture of the business.

Three layers of business, three different time horizons

To understand COHR, the key is: don’t treat it as just a large optical‑module vendor. Its asset profile is closer to a three‑story building, with each floor playing a role on a different time horizon.

The top floor: data center & communications

This is the core engine driving revenue right now; in Q2 FY26 this segment grew 34% year‑on‑year and accounted for about 72% of total revenue. The most direct growth driver is 800G and 1.6T optical modules. COHR is one of the world’s top two data‑center optical‑module suppliers, and in the AI data‑center build‑out boom, 800G is already shipping in large volumes while 1.6T is starting to take over. Competition here is intense, with Chinese vendors like Innolight in full pursuit, so what’s being contested is not just technology but also delivery capability and yield management.

However, COHR has done something surprising on 1.6T: it supports three laser‑technology routes at the same time—silicon photonics (SiPh), InP EML, and GaAs VCSEL. These three are not in a “which is superior” relationship; rather, they are different solutions tailored to different customer requirements. At the just‑concluded OFC 2026 conference, COHR showcased 1.6T transceivers built on all three laser technologies and demoed them with DSP chips from three different vendors. Some might ask: does this mean COHR itself doesn’t know which route will win, so it’s just betting on everything? That’s a great question, and the answer is actually the opposite. Different hyperscale customers (Google, Microsoft, Meta, Amazon) have different requirements on power, cost, and packaging, and no single laser technology can sweep all use cases. COHR’s technology‑neutral approach means that no matter which technology a given customer chooses, they can come to COHR for a one‑stop solution. This is something LITE currently cannot do and is the core of COHR’s value as a platform‑type supplier.

Next up is another growth curve that is seriously underestimated: ZR/ZR+ DCI (data center interconnect). These products solve long‑haul transmission between data centers—hundreds of kilometers, inter‑city coherent‑optical links. AI data centers are not just about one building; cloud providers need to knit data centers across different regions into a single whole, and ZR/ZR+ does that job. This business has posted sequential growth for multiple quarters, which is not a fluke but reflects the steady rollout of multi‑data‑center strategies by cloud providers. Moreover, competition is more concentrated and technical barriers are higher here than in short‑reach modules, and only a few players can do it well. LITE has almost no head‑on deployment in this niche.

Looking further out, OCS (optical circuit switching) and CPO (co‑packaged optics) are two tracks where large‑scale shipments have not begun, but orders are already piling up. In Q2 FY26, COHR had more than 10 OCS customers, and its overall data‑center book‑to‑bill ratio exceeded 4 times, with demand far outstripping current capacity. For CPO, COHR announced an unusually large purchase order in Q2 FY26, with initial deliveries expected by the end of 2026 and a much more meaningful ramp in 2027.

The middle floor: industrial lasers (seen as baggage, actually a hidden option)

Many investors quickly skip over industrial lasers. After all, SiC has been dragged down by the weak EV market, and on the surface CO₂ lasers don’t seem to have much to do with AI. But there is a detail few people pay attention to: COHR is one of the core suppliers of CO₂‑laser components for EUV lithography machines. The principle of extreme‑ultraviolet (EUV) lithography is to use a high‑power CO₂ laser to hit tin droplets, generating EUV light that then exposes the wafer. In ASML’s EUV equipment, key optical components of the CO₂ laser—diamond windows and output couplers—are supplied by COHR.

So when Coherent says on its earnings calls that orders related to semiconductor‑manufacturing equipment are picking up, what it is actually signaling is that the equipment‑purchase cycles of ASML, Tokyo Electron, and Applied Materials are turning up. This is a leading indicator of advanced‑node capacity expansion, but most people have their eyes glued to COHR’s optical modules and seldom connect this line back to industrial lasers. Management clearly stated on the Q2 FY26 call that the industrial business will start to improve in the second half of 2026. If that timetable holds, the point at which this segment stops dragging results and becomes at least neutral is already on the way.

The foundation: compound‑semiconductor materials (the most underrated moat)

InP wafers, SiC substrates, GaAs—these materials rarely stand under the spotlight, but they are the foundation of the entire optical‑communications value chain. This is also where something very important is happening.

One wafer, four times the output: the world’s first 6‑inch InP mass production

Now we come to the core of this article, something most people have missed but which might actually be the single most important thing COHR has done in the last two years.

First some background: in semiconductors, the larger the wafer diameter, the more chips you can cut from a single wafer, and the lower the cost per die. This applies to all semiconductors, including InP wafers used to make laser devices. The industry’s evolution from 3‑inch to 4‑inch, then 6‑inch and 8‑inch wafers in general semiconductors has each time been a restructuring of the cost base.

The problem is that InP is extremely hard to process—more brittle than silicon and harder to control than GaAs—so the industry has long been stuck at 3‑inch or even smaller wafers. The vast majority of global InP laser makers, including the main EML‑chip players, still use 2‑inch or 3‑inch wafers today. LITE’s current InP main lines are already on 4‑inch, which counts as leading‑edge in the industry.

COHR, however, did something much more aggressive in early 2024: at its Sherman, Texas, and Järfälla, Sweden fabs, it established the world’s first 6‑inch InP wafer‑fabrication lines and then ramped them quickly into volume.

The numbers tell the story:

- For the same fab floor area, a 6‑inch wafer yields more than four times as many laser chips as a 3‑inch wafer.

- The manufacturing cost per laser is over 60% lower than in the 3‑inch era.

- Even in early mass production, the yields on the 6‑inch lines have already reached and are gradually exceeding those of the mature 3‑inch lines.

In February 2026, the Texas state government announced a 14‑million‑dollar specialized semiconductor‑manufacturing grant to COHR to further expand 6‑inch capacity at the Sherman fab. By the OFC conference in March 2026, COHR showcased larger‑scale 6‑inch InP demos and announced that a third 6‑inch fab in Zurich, Switzerland is under construction. By the end of 2026, COHR expects 3‑inch and 6‑inch wafers to each account for 50% of its InP output; by 2027, almost all incremental capacity will come from 6‑inch. COHR has also signed 3‑ to 5‑year supply agreements with multiple 6‑inch InP substrate vendors, locking in its upstream materials.

Now go back to the information from the beginning: LITE is one of COHR’s external InP suppliers. What does that imply? It implies that as COHR’s own 6‑inch capacity ramps to scale, its procurement needs from external suppliers (including LITE) will naturally decline. At the same time, the cost of COHR’s own InP lasers will be sliding down a very steep curve.

LITE’s moat today largely comes from the combination of “explosive AI‑optical‑interconnect demand + highly constrained InP supply.” In the 2026–2027 period when CPO goes from 0 to 1, that supply‑shortage story still holds, and LITE can enjoy scarcity premiums. But looking beyond that, once COHR’s 6‑inch capacity is fully ramped, the supply picture of InP will change. This does not mean LITE will collapse, but it does mean that overall InP‑supply elasticity will increase and the scarcity premium will start to compress. This is a variable that will not really show its impact until 2027–2028 and has not yet been fully priced by the market.

Liquid crystal or micro‑mirror: an open question on OCS

Turning to OCS, there is a technical detail that often gets ignored.

The previous article described LITE’s OCS product (R300), which uses MEMS micro‑mirror technology: tiny mirrors etched on the chip are tilted by electrostatic force to switch light between fibers. COHR’s OCS takes a completely different path: liquid‑crystal technology. It controls light polarization in liquid crystal to switch paths, has no mechanical moving parts, and runs at very low drive voltages (under 10 V), giving it theoretical advantages in high‑reliability scenarios. COHR has more than 18 years of experience with this technology, and its liquid‑crystal WSS (wavelength‑selective switches) have long been deployed in undersea cables, facing the harshest reliability tests.

So which technology is better? The honest answer is: at this point, no one knows. Both have real, large customers and are running in production hyperscale data centers. MEMS advantages include greater technology maturity, lower insertion loss, and better per‑port cost at scale; liquid crystal’s advantages are no mechanical motion, ultra‑low power, and unique value in high‑reliability use cases.

The market will not run a lab‑style shootout but will vote with purchase orders. In Q2 FY26, COHR had more than 10 OCS customers and a book‑to‑bill ratio greater than 4 times, while LITE had an OCS backlog of over 400 million dollars from three major hyperscale customers. Both are ramping shipments, just along different technical routes and customer mixes. In the early stages, the OCS market is unlikely to be winner‑takes‑all; liquid crystal and MEMS are more likely to coexist in different scenarios. By 2029, most institutions expect the global data‑center OCS market to reach somewhere in the low‑ to mid‑two‑billion‑dollar range annually. In a 2‑billion‑dollar market, there is room for two technology paths and for both companies to grow simultaneously. The real contest is not whose technology is “more correct,” but who can grow their customer count from 10 to 30 faster.

The financial story: two engines pushing EPS

Financials ultimately anchor the story, and here there is one detail worth highlighting because it changes how you categorize this entire thesis.

When people analyze a company’s EPS growth, they usually think: revenue goes up, margin follows, EPS naturally rises. COHR is in a special position in that it has two independent EPS‑growth engines operating in parallel.

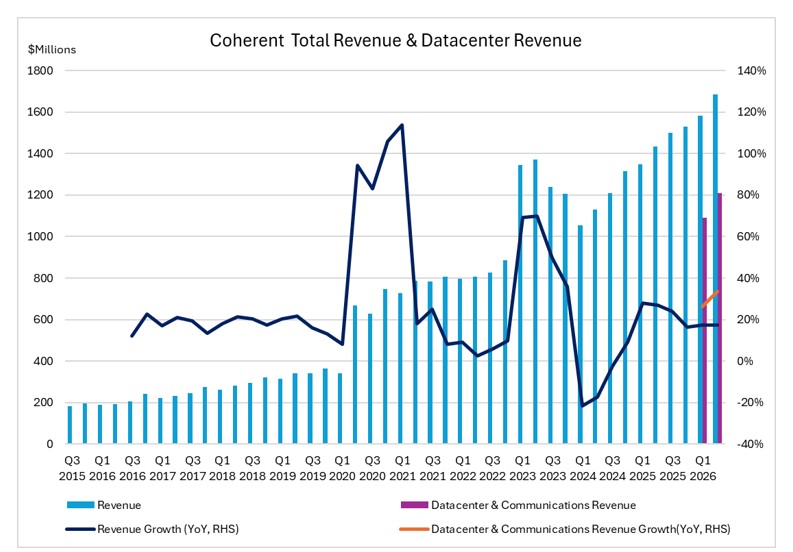

First: rapid revenue growth plus product‑mix upgrade. In Q2 FY26, revenue reached 1.686 billion dollars, about 17% year‑on‑year growth; strip out the divested defense business and underlying growth is about 22%. The data center & communications segment grew 34% year‑on‑year.

Source: Company financial reports, TradingKey

Note: Datacenter & Communications is a newly disclosed figure by the company, and currently only a few quarterly data are available.

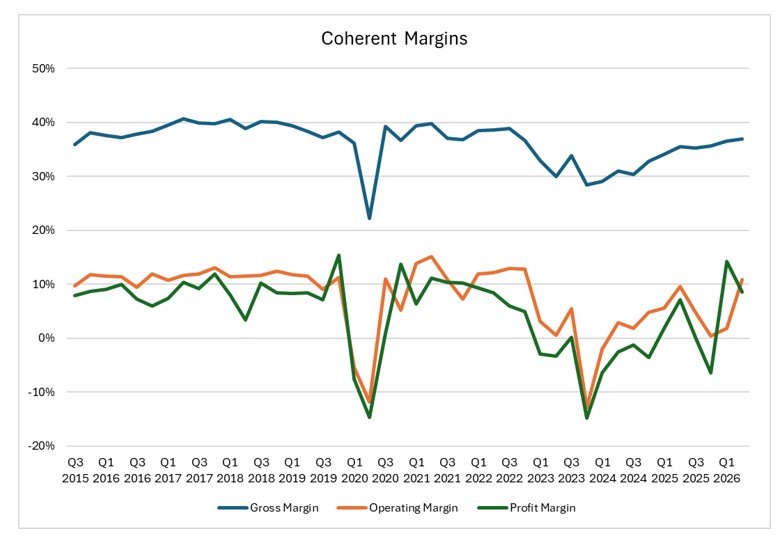

Gross margin improved from 35.5% in Q2 FY25 (non‑GAAP 38.2%) to 36.9% in Q2 FY26 (non‑GAAP 39.0%). On the one hand, 1.6T products carry structurally higher margins than 800G, so as 1.6T’s shipment share rises, overall gross margin naturally trends up; on the other, 6‑inch InP is starting to land at the margin, and every additional laser die cut from a 6‑inch wafer has a cost lower than before.

Source: Company financial reports, TradingKey

Second: a systematic decline in interest expense. In FY2025, Coherent’s annual interest expense was around the 240‑million‑dollar level. As it sells the defense assets, accelerates debt repayment, and refinances at lower rates, the market generally expects this to drop to around 140 million dollars by FY2027. The interest savings of roughly 70–80 million dollars before tax, or 50–60 million after tax annually, translate to about 0.30–0.40 dollars of EPS on the current share count, and this uplift does not require selling a single extra optical module—just following through on the debt‑reduction plan.

Putting the two lines together, current consensus calls for about 5 dollars non‑GAAP EPS for FY26 and about 7 dollars for FY27. Guidance for Q3 FY26 is 1.7–1.84 billion dollars in revenue, implying continued sequential growth, and with 1.6T and OCS shipments accelerating in the second half, non‑GAAP gross margin is expected to cross the 40% threshold.

Time to talk about risks

Having covered many of the interesting aspects, in fairness there are several real issues that cannot be ignored.

- Slower‑than‑expected margin improvement. COHR’s gross‑margin recovery has been relatively conservative compared with peers, partly because the 6‑inch transition is still absorbing upfront investment and scale effects need time to ramp. If there is no clear step‑change improvement in the second half of 2026, the market will be disappointed.

- Debt is both leverage and shackle. Quarterly interest payments are still running at about 50–60 million dollars. This means COHR is far more sensitive than LITE to swings in the AI cycle. If AI data‑center build‑outs slow for even a quarter, the contraction in cash flow, even as absolute interest is coming down, will still be magnified through leverage in the share price.

- Integration‑risk overhang. There is about 4.47 billion dollars of goodwill on the balance sheet, and the integration work from the three acquisitions is far from complete. If any business line underperforms structurally, impairment tests could trigger one‑off non‑cash hits.

- OCS‑technology uncertainty. Long‑term reliability data for liquid‑crystal OCS in large‑scale data‑center deployments is still not robust enough. If a major customer decides to slow or halt validation, today’s striking book‑to‑bill ratios could fade quickly.

- Geopolitical exposure. On the manufacturing side, COHR has facilities in Asia (Malaysia, Vietnam), and on the demand side it has some exposure to Chinese customers. Any shift in export‑control regimes is an uncontrollable tail risk.

COHR vs. LITE: same track, different bets

We can now return to the original question: how should an investor look at these two companies?

Key comparison: LITE vs. COHR

Dimension / Metric | LITE (Lumentum) | COHR (Coherent) |

Business model | Optical chip IDM, mainly selling lasers and optical components | Vertically integrated platform, covering materials, devices, and systems end to end |

FY26E revenue (est.) | About 2.7–2.9 billion dollars (AI/Datacom driven, high teens growth) | About 6.8–7.2 billion dollars (transport + industrial + CPO, mid teens growth) |

InP wafer node | Mainly 4 inch, expanding capacity | First to mass produce 6 inch InP; per wafer output about 3–4× 4 inch |

OCS technology | MEMS micro mirror, 300×300 ports, mature 400G/800G cost down | Liquid crystal OCS, 10+ customers, book to bill > 4×, tied to next gen AI racks |

1.6T laser strategy | EML + CW, focused on InP Datacom | SiPh + InP EML + VCSEL in parallel, covering short/medium/long reach |

Debt / equity | About 0.08, nominally low leverage | About 0.35, real financial leverage but within control |

Forward P/E | Around 62 | Around 40 |

AI cycle sensitivity | Revenue highly tied to AI Datacom orders, almost no interest burden; share price mainly moves with orders and valuation | More diversified but with leverage and fixed interest; cash flow and share price more sensitive to AI build out and margin recovery |

Data Source: StockAnalysis, & Company financials and guidance

Both companies received the same 2‑billion‑dollar strategic investment from Nvidia and are on the same optical‑interconnect track, but they appeal to different types of investors.

LITE is a sharper blade: focused and pure, with greater direct exposure to CPO‑laser demand and a very clean balance sheet without debt. In the 2026–2027 phase when CPO ramps from 0 to 1, LITE has higher operating leverage and is an easier story to tell. COHR is a heavier machine: larger and more complex, with debt both the cause of its current discount and the source of future value. 6‑inch InP is a manufacturing revolution in progress; DCI is an independent growth curve that LITE does not have; industrial lasers are a recovery option hidden in the financials. Its EPS story in 2027–2028 could be stronger than most models expect, but you need patience to let it shed the burden of debt.

If you believe the AI‑optical‑interconnect boom is a multi‑year theme rather than just a two‑ or three‑quarter trade, then these two names are not mutually exclusive. Instead, they are two different kinds of exposure you can allocate based on risk preference: one is a bet on scarcity at the optical‑chip layer, and the other is a bet on the manufacturing foundation of the entire optical‑communications infrastructure.

Disclaimer: This article is based on public information and does not constitute investment advice. Data is drawn from company financials, official announcements, and public sources. Investing involves risks; decisions must be made at your own discretion.

Recommended Articles