Memory Chip Stocks Gain More Wall Street Bullishness, SanDisk and Micron Shares See Massive Recovery

TradingKey - On Wednesday, Eastern Time, Morgan Stanley (MS) significantly raised its price target for Micron from $350 to $450 in a newly released research report, while maintaining an "Overweight" rating. Simultaneously, the bank designated Micron as its top pick in the semiconductor sector.

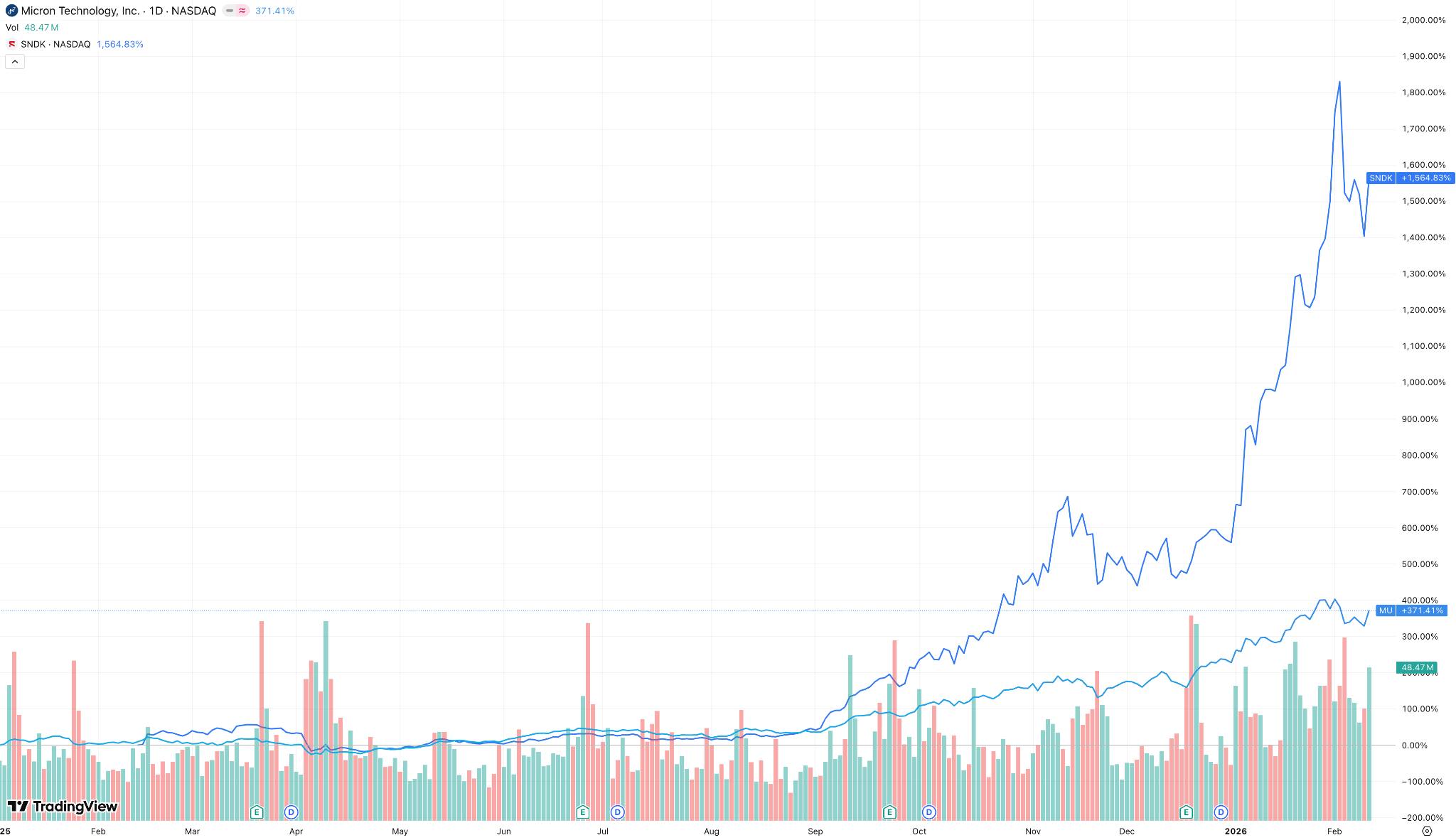

Buoyed by the news, the U.S. storage sector rallied sharply, SanDisk (SNDK) surged 10.65%, Micron Technology (MU) rose 9.94%, Western Digital (WDC) gained over 2%, Seagate Technology (STX) rose nearly 3%.

[SanDisk and Micron Price Chart, Source: TradingView]

Previously, U.S. storage chip stocks had experienced a significant decline, driven by overall market concerns over an AI bubble and a correction following the sector's massive gains.

Morgan Stanley explained its Overweight rating for this round: the mismatch between demand and production capacity continues to intensify, and pricing power continues to increase.

In reaffirming its "Overweight" rating, Morgan Stanley is not merely echoing market consensus but emphasizing in stronger terms that the current supply-demand imbalance for storage chips has far exceeded expectations—demand remains high driven by AI, while the supply side is constrained by slow capacity ramp-ups. Morgan Stanley believes the current situation is more severe than previously perceived by the market.

Whether for DRAM used in computer memory or NAND flash used in mobile phones and SSDs, prices for the first half of 2026 are rising rapidly.

While Micron did not provide specific figures in its earnings report, its latest guidance suggests that the quarter-over-quarter increase in average selling price (ASP) could be close to 30%. SanDisk, meanwhile, expects NAND prices to skyrocket by 60% in a single quarter.

This price hike translates directly into profit. Morgan Stanley predicts that Micron's 2026 earnings per share (EPS) could exceed $52—far higher than the current market consensus of approximately $12. As long as market conditions are confirmed to be better than expected, any stock price correction resulting from a "lack of guidance" could be a buying opportunity.

While investors have traditionally viewed Micron as a "cyclical stock," its profitability has now far surpassed the peak of the previous cycle, with higher gross margins and stronger cash flow. Morgan Stanley values Micron at a 25x P/E ratio, which, combined with the upwardly revised earnings forecast, results in a $450 target price, implying significant further upside for the stock.

Regarding market concerns such as capacity expansion by Chinese manufacturers and delays in HBM4 technology, Morgan Stanley believes these have been overblown. Micron has already passed HBM4 certification and is expected to begin mass production in the second quarter of 2026; even with short-term fluctuations, its mainstream product, HBM3e, continues to support robust revenue.

Recommended Articles