Adobe’s AI Play Is Working

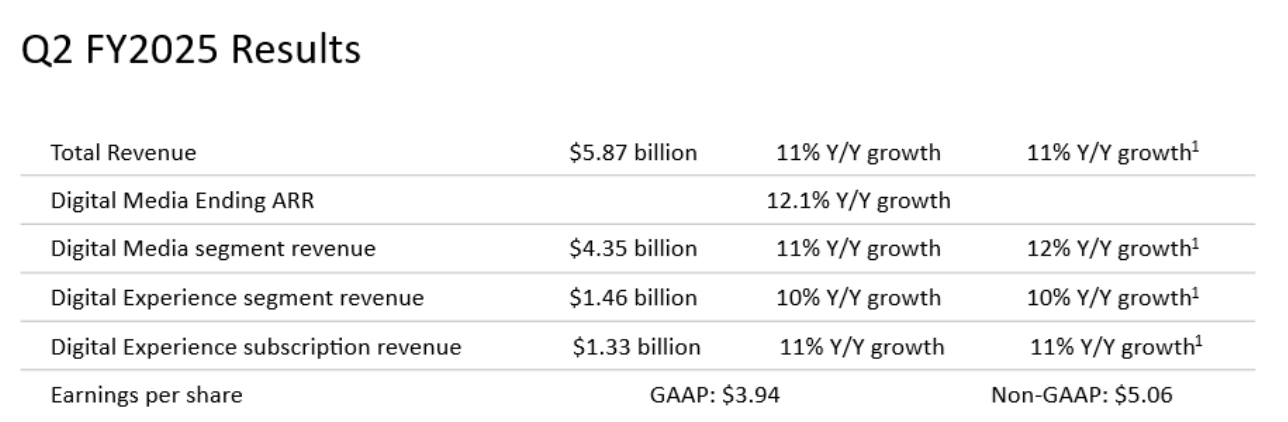

- Adobe posted Q2 FY25 revenue of $5.87 billion, up 11% YoY, with ARR reaching $18.09 billion, growing 12.1%.

- Operating margins hit 45.5% non-GAAP, with $2.19 billion in operating cash flow and $3.5 billion in share repurchases.

- Firefly and AI Assistant tools boosted productivity across Creative and Document Cloud, driving deeper monetization and user engagement.

- Despite strong fundamentals, Adobe trades at 18.3x forward P/E, 45% below its 5-year average and 17% below the sector median.

Adobe (ADBE) enters the latter part of FY2025 with strategic momentum: its own ongoing transition into an AI-first platform business. With revenues jumping by 11% year over year in Q2 to an all-time high of $5.87 billion and the FY2025 outlook increased to $23.5–23.6 billion, Adobe is clearly succeeding. Yet investor enthusiasm isn't exactly ecstatic. The stock itself trades at just 18.3x forward-looking non-GAAP earnings, down by over 45% from the 5-year average and the peer median by nearly 20%. What's going on?

It’s the investor recalibration disconnect. While there is no competition for creative software that is led by Adobe, new competition that is native to AI, like Canva, Figma, and OpenAI integrations, has redrafted the margins, pricing leverage, and cadence playbook. Adobe’s moat isn’t even broken, though. Its embeds of generative AI across Creative and Document Cloud are gaining customer stickiness, and with the business model that’s based on $18 billion+ recurring ARR, the durability that most cannot match is provided.

Business Deep Dive: Scaling Artificial Intelligence Across All Customer Segments

Adobe's business comprises two main segments: Digital Media and Digital Experience. The latter, consisting of Creative Cloud and Document Cloud, generated Q2 revenue of $4.35 billion, representing an 11% YoY growth. The ARR stood at $18.09 billion, with 12.1% growth, suggesting that users are not only remaining loyal but are increasing their expenditure.

Source: ADBE Q2FY25 Investor Datasheet

Meanwhile, the Digital Experience business, Adobe’s enterprise-class customer journey management platform, brought in $1.46 billion in revenue during Q2, up 10%. Subscription revenue was up 11%, showing that Adobe’s move away from infrequent license-based business and toward cloud-native, data-driven SaaS power is gaining traction.

Source: Adobe Q2 FY2025 Earnings Call

From a strategy point of view, Adobe is going all out with AI. Firefly-enabled new tools embedded within Photoshop and Premiere are creating more automated workstreams, and the AI Assistant within Acrobat is its foray into productivity AI, beyond visual creativity. There are no cosmetic enhancements; these are multipliers of productivity that lead to deeper monetization, especially among professional and enterprise users.

Competitive Pulse: Keeping the Moat While Playing Offense

Now that low-cost, fast, yet continually improving AI design software tools are here, Adobe is the incumbent and the disruptor. Rivals like Figma (acquired by Adobe pending various regulatory outcomes), Canva, and even Microsoft’s Copilot platform are all ready to unbundle document workflows or individual creativity.

But Adobe’s competitive strength is based upon three cornerstones: professional-level tools that are market-leading, seamless cloud-to-desktop workflow, and a horizontally scaled platform that ranges from solopreneurs to CMOs at Fortune 500 firms. Very few peers enjoy that breadth.

And Adobe’s pricing power is robust. Even in tough economics, it upsells by bundling AI functionality and new tiers, with low churn that’s industry-leading. Embedding generative AI isn’t cannibalizing revenues; it’s growth.

Strategic & Financial Deep Dive: High-Margin Growth with Structural Efficiency

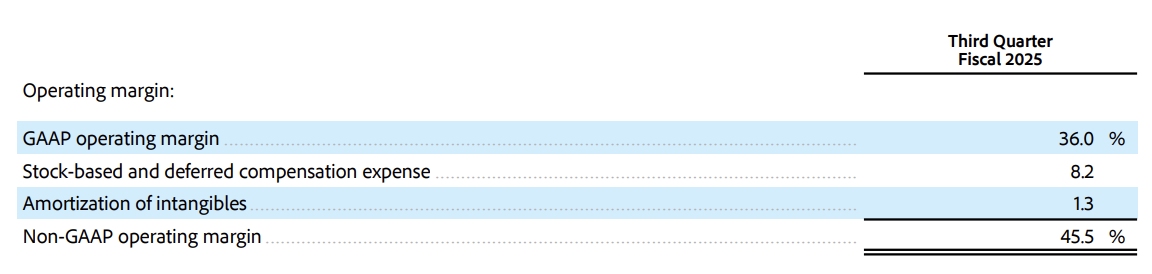

Adobe's bet on AI isn't hype; it's numbers. Operating income was $2.11 billion GAAP with a 36% GAAP operating margin. Non-GAAP margins actually looked healthier at 45.5%. The company is now forecasting full-year non-GAAP EPS of $20.50 to $20.70, a considerable jump above previous guidance.

Source: ADBE Q2FY25 Earnings Press Release

Cash generation remains strongest: last quarter's operating cash flow was $2.19 billion. That firepower is being redeployed efficiently, with share repurchases from last quarter totaling $3.5 billion, along with persistent investment across R&D and platform AI.

.jpg)

Source: Adobe Q2 FY2025 Earnings Call

But valuation multiples for Adobe actually reflect a continuing valuation by the market, like that of legacy software firms. PEGs of 0.60 (GAAP TTM) and 1.2 (FWD) reflect strong earnings growth relative to valuation. Its EV/EBITDA (FWD) is just 13.98x, reasonable for a growth firm that is raising EPS by double digits with gross margins over 90%.

However, high EV/Sales multiples (7.21x TTM, 6.91x FWD) are nevertheless troubling for value investors. Top-line growth at Adobe, while good at 10–11%, requires acceleration or diversification significantly before it can sustain such revenue multiples in the long term.

Valuation: Attractive Compression or Structural Re-Rating?

Adobe trades at a considerable discount compared with its own historic multiples and peer medians. Its forward P/E is at 18.46, which is nearly 45% lower than the 5-year median P/E ratio of 33.59 and 17% lower than the sector median. PEG ratios (both GAAP and Non-GAAP) reveal undervalued earnings growth as well.

But revenue-based multiples have a more complicated story. These types, like EV/Sales and Price/Sales, are substantially above sector multiples, more than 2x at times. That compresses earnings, but the stock is nevertheless qualifying for premium growth potential. If double-digit growth at ARR is sustained at Adobe, particularly in that high-velocity SMB and productivity AI business, the premium makes sense. But if growth comes down, that causes contraction at multiple levels.

Source: Seeking Alpha, Stock Price Summary

Looking ahead, employing a 22–25x multiple with future FY25 free cash flow (implied ~$8.5 billion – $9.2 billion) lays out a reasonable value range of $425–$460 per share. That’s 13–22% upside from here.

Risks: AI Cannibalization, Macro Drag, and Competitive Pressures

Adobe's main risk isn't financial; it's strategic. Generative AI could lower the premium creative software value by diminishing jobs that once required expertise. Adobe is adapting rapidly, yet the pace of disruption doesn’t diminish. Inexpensive alternatives could potentially undercut pricing in the long term.

Additionally, customer concentration among professional segments may expose Adobe to cyclical contraction of enterprise budgets. Macro changes, especially within Europe and Asia, could impact Digital Experience growth.

Finally, sustained oversight with respect to acquisitions (notably the acquisition of Figma) and antitrust concerns could deter M&A-based growth levers, again straining Adobe’s platform expansion.

Conclusion: A High-Margin AI Platform That’s Misunderstood

Adobe's stock is caught between crosswinds of transition. Valuation compression is a sign of market skepticism, but valuation tells a different story. With $23.5 billion+ managed revenue, 45%+ operating margins, and rising AI adoption across its suite, Adobe is positioning itself for the next level of profitable growth. Today's discount for the stock won't last forever, assuming generative AI turns out to be a commoditizing force rather than a moat enhancer.

Copyleaks Report: https://app.copyleaks.com/report/xlt6nvp6cjc5ja71/preview?key=l5qout5fkmd5t9x9&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

.png)

Get Started

Recommended Articles