AMD Q3 Earnings: Strong Beat Across the Board but Some Margin Headwinds

Summary

TradingKey - Advanced Micro Devices has been confidently riding the AI wave. Year-to-date, the stock has been up 115%, hitting new all-time highs. The deals with OpenAI and Oracle for its MI350 and M450 provided solid credibility for the company’s products. Due to Nvidia’s chips being superior in terms of power (and supported by the CUDA software system), AMD is often seen as of second importance or as a laggard in the GPU space. However, this also provides a lower basis for AMD to bring positive surprises.

Earnings Overview

Metric | 2025Q3 Actual | 2025Q3 Estimate | 2024Q3 Actual | Beat/Miss | YoY Change |

Revenue | $9.25bn | $8.76bn | $6.82bn | Beat | +36% |

Non-GAAP EPS | $1.20 | $1.17 | $0.92 | Beat | +30% |

Non-GAAP Gross Margin | 54% | 54% | 54% | Meet | +0pps |

Data Center Revenue | $4.34bn | $4.10bn | $3.55bn | Beat | +22% |

Client & Gaming Revenue | $4.05bn | $3.66bn | $2.34bn | Beat | +73% |

Overall, the 2025 Q3 results of AMD are solid, as the company achieved beats across the board and the guidance was upbeat too. The stock, however, went down nearly 5% after the market closure, mostly due to the recent broad AI-stock sell-off, as well as the fact that Amazon sold its stake in the chip maker, worth $206 million.

Data Center Segment

The data centre segment is surely the most important for AMD’s investment thesis, as this is where the AI-related revenue is. The segment primarily comprises the Instinct GPUs and the EPYC CPUs series, with the first being the main growth driver. Both of these products are used by hyperscalers, cloud providers, supercomputers and high-tech enterprises.

Product Line | Share of Total Segment Revenue | Main Products | Year-over-Year Growth Driver |

EPYC CPUs | ~50% | 5th Gen (Turin), EPYC4004 | Strong adoption in cloud/enterprise servers; market share of data center CPUs hit ~39% by Q1 2025. |

Instinct GPUs | ~50% | MI300X, MI350, MI325X | AI/HPC accelerators (e.g., MI-series); ramped from near-zero in 2023.

|

Rack-Scale | NA | Helios AI Platform | From recently acquired ZT Systems; Expected $2-3bn revenue in FY2026 |

Source: Company Presentation

The data centre revenue increased 22% driven by both EPYC CPUs and MI350 GPUs, once again excluding the MI308 GPU shipments to China. The MI355 chip which was recently launched, is already contributing significant revenue and the ramp-up is in early stages, that would be the main competitor to Nvidia’s B200. Next year, we also expect launches of AMD’s MI450 and NVIDIA’s Rubin chips, continuing the intense competition among these two.

The segment operating margin of 25% is worse than what we saw in 2024 Q3, but this is mostly due to strategic decisions by the management, such as 1) front-loading R&D expenses; 2) ZT Systems acquisition costs and 3) more share-based compensation to attract talent.

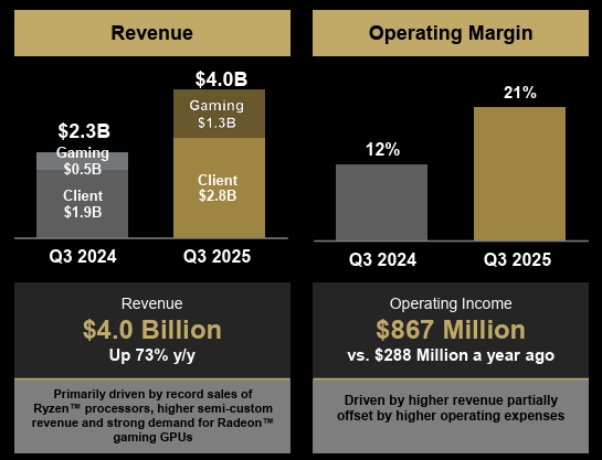

Client and Gaming Segment

Source: Company Presentation

The main product line in the client segment is the Ryzen-series chips, used primarily in PCs, laptops and Chromebooks from various brands such as Dell, HP, Lenovo and ASUS. On the gaming segment side, we have the Console SoCs and the Radeon Discrete GPUs used in gaming consoles and PCs.

For Q3, the client and gaming businesses altogether had an impressive growth of 73% year-over-year on the back of a broad PC and Gaming market recovery.

We also see a big expansion in the operating margin for these two business lines from 12% in 2024Q3 to 21% in 2025Q2. This is mostly because products like Ryzen AI 300 and Radeon 9000 can dictate higher pricing. In addition, unlike in the data centre segment, here the management does not need to spend excessively on R&D or share-based compensation.

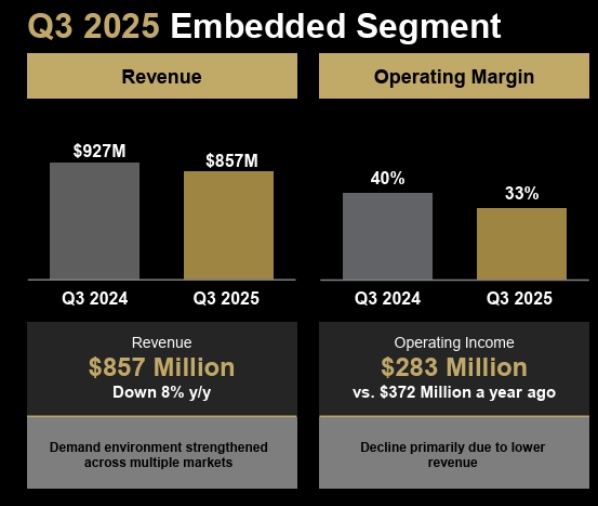

Embedded Segment

Source: Company Presentation

The embedded segment is aiming at hardware for industrial, networked, and edge applications. It is relatively high gross margin (above 54%) but also quite cyclical and not as big as compared to the other two segments (less than 10% of the total Q3 revenue). In Q3, the revenue went down 8% year-over-year, mostly due to weakness in spending within the telecom and industrials sectors, and it may take some time before we see a recovery here.

Balance Sheet and Cash Flows

Total inventories were significantly up at around $7.3 billion (versus $5.7 billion at the end of 2024). We believe this build-up is not about suppressed demand but more like preparation for sales in the coming quarters. Also, the cash position and the short-term investments, totaling $7.2 billion, far exceed the short-term and long-term debt of $3.1 billion. We also saw a big increase in the operating cash flows of almost four times from $628 million to $1.79 billion.

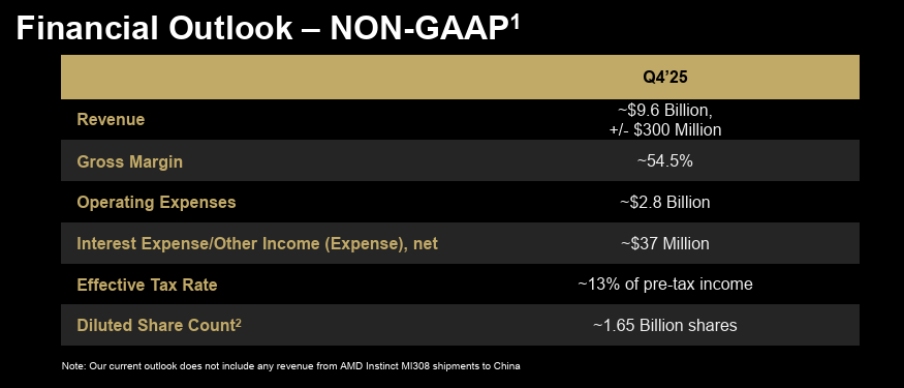

Guidance

Source: Company Presentation

Q4 guidance of approximately $9.6 billion and 54.5% gross margin is higher than what most analysts expected, again, excluding the potential shipments of MI308. In case the situation normalises and shipments resume, we can see some sort of revenue-sharing arrangement with the US Government, and this can be a potential upside for AMD. The MI308 impact on the revenue can be around $800 million, and that can be a conservative estimate.

Outlook

Beyond 2025 and 2026, the company will benefit from the inference stage, which is expected to take full pace in 2027-2030, and according to the words from both Jensen and Lisa, will be way bigger than training. AMD has been preparing for the inference stage for years. For the inference, clients may favour memory capacity and cost efficiency, areas where AMD can compete (and even outcompete Nvidia).

Factor | AMD | Nvidia | Advantage |

GPU Cost | $25K | $40K | 38% |

Power (per GPU) | 750W | 1,000W | 25% lower |

Memory Bandwidth | 8TB/s | 4.8TB/s | 67% faster |

Memory Capacity | 288 GB | 141 GB | 2x bigger |

Another major tailwind will be the OpenAI 6GW deal, valued at around $90 billion. If the ramp-up is smooth, this will be able to bring an extra $15-20 billion annual revenue for the data centre segment.

Considering the 1) future inference tailwind; 2) the current strong demand for data centre GPU; 3) the recent mega deals; and 4) revival of the PC segment - a 30% growth in the total revenue in the next 2-3 years is a very achievable target.

As for the margins, they currently revolve around 50% GPM and 14% GAAP OPM as we see increased operating expenses in the form of R&D and stock options. We expect an upward direction in the margins, as high-margin segments such as Data Centre become a larger portion of the company’s revenue. Nvidia GPU margins are higher at around 60-70%. With the further development of the MI GPU series, we expect the AMD gross margin to expand to around 55% catching up with Nvidia. Last but not least, the operating expense headwinds mentioned will gradually become less of a factor.

Competition with Nvidia

Many may argue that Nvidia chips are better, and this is true (for now). We can see this with the 90%+ market share in the AI GPU market. However, a better product does not mean a better investment.

Historically, in the chip industry, there is cyclicality, but the current AI boom breaks out from this; thus, demand right now is not a concern, and the question is not about either Nvidia or AMD. Total cost for AMD products is lower, implying certain price/power efficiency, which will become more important as scalers try to control their massive capex numbers. Also, clients do not want to rely entirely on Nvidia; they need to diversify their supply chains.

With an enormous market cap of $5 trillion, it is very difficult for Nvidia to grow its market cap at this scale. AMD’s market cap is 10 times smaller; thus, buying an underdog like AMD definitely provides more upside.

Last but not least, AMD will continue to improve its products, making them more powerful, efficient and competitive with Jensen’s products.

Risks

A major risk amid the recent mega deal with OpenAI is Sam Altman’s company being financially unsustainable and not being able to break even, due to a lack of demand or losing market share to competition. If that’s the case, these $90bn of potential revenue for AMD, partially or in full, may not materialise.

Competition is still a risk as well, and it may come from where we don't expect. Intel has experienced a lot of problems in recent years, but they laid the foundation for a long-term recovery, and if it starts to make things work, that can bring pressure to AMD.

Delivery and operational obstacles may also hit AMD’s plans. We saw certain supply chain issues in Nvidia last year, and AMD is not immune to that either. As AMD is ramping up the new MI-series chips, it may experience delivery delays, logistics problems and so on. This can affect both the revenue and the margins.

Geopolitical tensions are still on the table. Last quarter, we saw how both the growth and the margins took a very serious hit from restrictions on selling to China. It is unlikely to see a very stable international environment, thus another risk is on the table.

Valuation

If we assume a CAGR of 30% top-line growth, the revenue in 2028 will be around $75 billion. With a net margin of around 20% (which is still quite conservative in the context of a 50% net margin for Nvidia), that translates into $15 billion of net income and a forward PE of 27x, which is still attractive considering an earnings growth of 30%-40% and the stock may double in that period of time.

Recommended Articles