Apple FY2025 Q4 Earnings Review: Signs of a Structural Turnaround as Services and AI Set the Stage for Future Growth

TradingKey – In a 2004 interview, Steve Jobs stated, “The more and more consumer devices, the core technology in them is going to be software.” Over two decades later, Tim Cook has carefully and consistently carried out that vision. On October 30, Apple released its full-year financial report for fiscal year 2025 after the market closed, reinforcing that strategic shift with strong financial evidence.

FY2025 Q4 Highlights

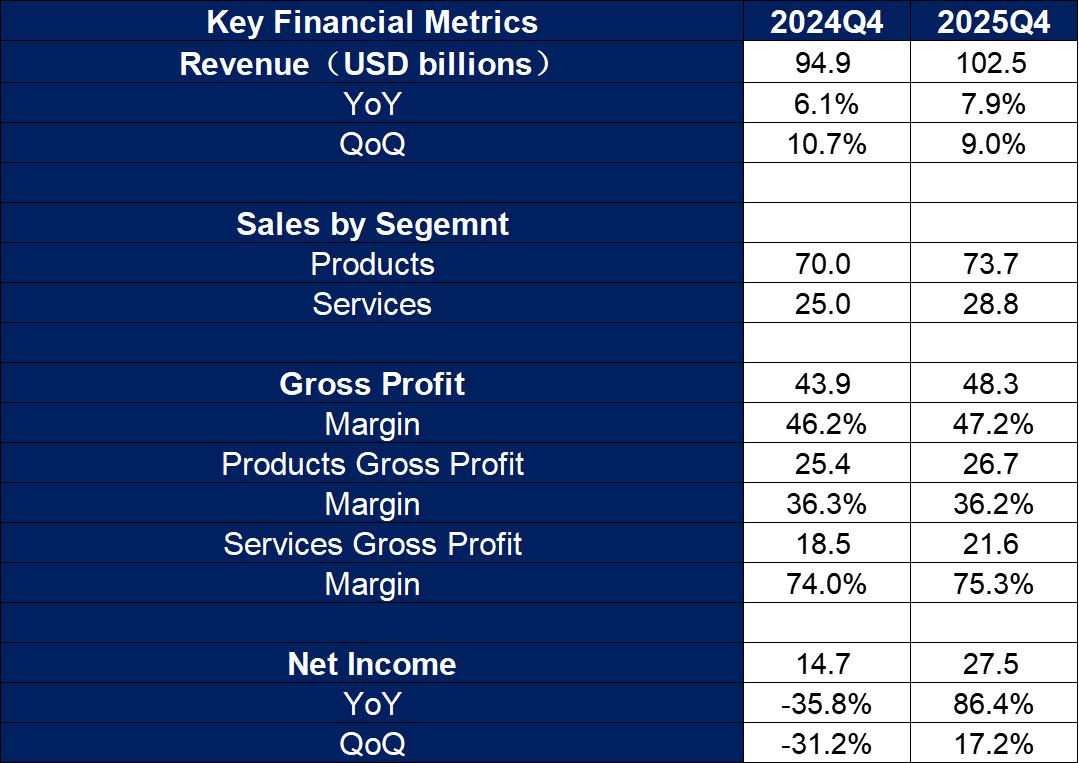

Boosted by surging demand for the new iPhone 17 lineup, margin-rich software and services revenue, and some relief in global tariff pressures, Apple once again delivered an earnings beat. Total revenue for Q4 came in at $102.47 billion, up 7.9% year-over-year and 9% sequentially, exceeding Wall Street’s consensus estimate of $102.19 billion and setting a new annual revenue record.

Gross profit reached $48.3 billion with a margin of 47.2%, exceeding the high end of forecasts. Net income grew to $27.47 billion—an 86.4% YoY increase and double-digit QoQ growth. For the full fiscal year, Apple posted $416.16 billion in revenue (up 6%) and $112 billion in net income (up 19%), marking annual gains on both top and bottom lines.

Data Sources: Reuters, TradingKey As of: October 31, 2025

Segment Breakdown

Both hardware and services performed solidly year-over-year. Hardware revenue reached $73.7 billion (+5.3% YoY), while services grew at a faster pace, rising from $24.97 billion to $28.75 billion—up more than 15%.

Data Sources: Reuters, TradingKey As of: October 31, 2025

● Hardware:

iPhone sales came in at $49 billion, a 6% YoY increase, slightly below market expectations given a mid-quarter launch for the iPhone 17 series and delayed deliveries of the iPhone 17 Air in Greater China. As such, the current quarter only partially reflects full-cycle sales. Nonetheless, initial demand appears strong—early tracking indicates that iPhone 17 sales in the U.S. and China were 14% higher than the iPhone 16 in its first ten days of availability.

With robust early momentum, management offered a bullish outlook, stating that Q1 2026 could mark Apple’s strongest-ever quarter for iPhone shipments, driven by double-digit growth.

Mac, meanwhile, saw a standout quarter, with revenue rising 12.7% YoY to $8.73 billion. Driving this performance was the launch of MacBook models featuring Apple’s new M5 chip, which offers 3.5x AI performance improvements over previous generations.

● Software & Services:

While devices remain Apple’s entry point to customer ecosystems, it’s services that have become the company’s profit engine. Services revenue reached $28.75 billion this quarter alone, up over 15% YoY, with gross margins expanding from 74% to 75.3%—more than twice that of hardware operations.

As a result, Apple’s total gross margin for the quarter rose to 47.2%, and for the first time in history, services overtook iPhone as the largest contributor to gross profit: services accounted for 42% versus 41% from iPhones. Analysts expect services margins to stay above 70% for the foreseeable future, far exceeding hardware’s projected 36%, further supporting income growth in fiscal 2026.

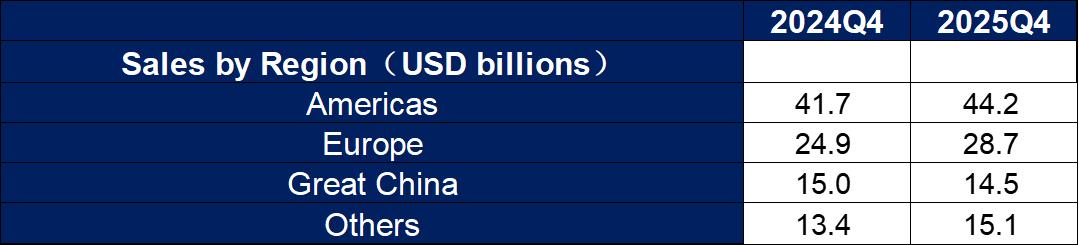

Regional Performance:

Data Sources: Reuters, TradingKey As of: October 31, 2025

One area of concern is Greater China, the only region where Apple saw revenue decline, slipping 3.6% YoY to $14.49 billion. Despite repeated assurances from Tim Cook regarding the market’s strategic importance, pricing sensitivity and rising local competition continue to weigh on results.

Apple had attempted price cuts the previous quarter to stabilize sales in China, but initial results remained mixed. That said, the outlook may improve: improved chips and pro-grade cameras in the iPhone 17 series are resonating with consumers. Apple has reportedly instructed suppliers to raise production targets—up 25% YoY for the base iPhone 17 and an outsized 60% increase for the Pro Max.

Balance Sheet & Cash Flow

Apple ended Q4 with $132 billion in cash and marketable securities—a slight dip in asset size due to a drawdown in inventory, but a record in cash holdings. Short-term liabilities fell by $10.76 billion (-6.1%) as the company aggressively paid down debt. As a result, the debt-to-asset ratio improved from 84.4% to 79.5%.

Operating cash flow jumped to $29.73 billion, the largest ever in a single quarter, with free cash flow exceeding net income. The operating cash-to-net income ratio stood at 1.08—signaling high earnings quality and solid receivables collection.

Investment cash flow was negative $2.59 billion, reflecting ongoing CapEx and targeted reinvestments. Total CapEx reached $12.7 billion for FY2025, a 34.5% increase YoY. CEO Tim Cook noted during guidance that Apple intends to ramp up AI-related R&D and expand via acquisitions where needed to advance its strategic roadmap.

Financing cash outflow stood at -$27.48 billion—driven by significant buybacks and dividends. Despite that, free cash flow was sufficient to cover outflows. The board declared a dividend of $0.26 per share, payable on November 13, 2025.

Looking Ahead: Key Themes to Watch

● AI Strategy Taking Shape

Apple’s AI roadmap is coming into focus. The company has scaled up investments across private cloud infrastructure and chip-level AI processing. Siri is currently being rebuilt with large language model capabilities and is expected to be released as part of the next-generation iOS update in 2026.

Additionally, Apple announced a sweeping $60 billion U.S. investment plan over four years—focusing on silicon engineering, onshore manufacturing, and AI infrastructure. A new AI facility in Houston has already begun shipping.

● Foldables and Wearables on the Horizon

The company’s first foldable iPhone is reportedly on track for a 2026 launch with an expected starting price of $1,800. While foldables remain a niche segment, Apple’s entry could unlock new TAM and drive adoption among existing and new customers.

Headsets are another major hardware vector in development. Though Apple has confirmed no new headset launches in 2026, starting in 2027, the company is expected to roll out multiple AR/VR offerings. Sources suggest that Apple is secretly developing seven wearable SKUs, comprising three Vision series headsets and four smart glasses models.

Valuation & Takeaways

Among the "Magnificent Seven" tech giants, Apple has been the quietest around AI development. While some investors worry it might miss the next big wave, this quarter’s results suggest the urgency may be overstated. Consumers are not yet demanding AI smartphones, and Apple’s product stacking and iterative engineering remain effective in driving upgrades.

Meanwhile, the company’s strategic transformation is visibly working: services have become its most profitable growth lever. With a supportive install base and growing monetization per user, this trend is likely to continue.

On valuation, Apple now sits above a $4 trillion market cap, joining the ranks of the most valuable U.S. firms. Based on its FY2025 net income of $112 billion, the current trailing P/E ratio is around 36X. Adjusting for non-recurring tax effects in FY2024, Apple delivered ~8% normalized net income growth this year.

Looking forward, management’s bullish stance on iPhone sales suggests both revenue and net income could sustain a high single-digit growth into FY2026. That would still leave forward P/E above 30X (a premium to Apple’s historical 25X–35X band) meaning the stock might not be “cheap” by traditional standards.

However, with a massive user base, pristine balance sheet, and potential for upside from new hardware or AI product breakthroughs, Apple still offers long-term upside for investors focused on quality and consistency.

Risks to Watch

Competition from Huawei, Samsung, and others remains intense, particularly in smartphones and wearables.

Tariff instability and geopolitical pressures could further strain Apple’s supply chain, putting pressure on margins and volume.

Macroeconomic fluctuations and huge capital expenditure commitments have brought significant operational pressures, posing a test to its financial stability.

Execution risk looms: delays or failures in AI, foldable phones, or wearable rollouts could impair future earnings momentum.

Recommended Articles