U.S. Government Shutdown Odds Plunge — Can Wall Street Finally Break the September Effect?

TradingKey - In a last-minute bid to avoid a government shutdown, President Donald Trump met with congressional leaders on September 29 — just hours before federal funding expires. The move caused shutdown probability in prediction markets to drop sharply, reigniting investor optimism that U.S. equities could finally break the infamous “September Effect.”

With the deadline for a government shutdown set at October 1, this was Trump’s first meeting with congressional leaders during the final stretch of negotiations. Given his earlier cancellation of talks and dismissive remarks like “let it shut down,” this sudden engagement signals a strong urgency to prevent a shutdown.

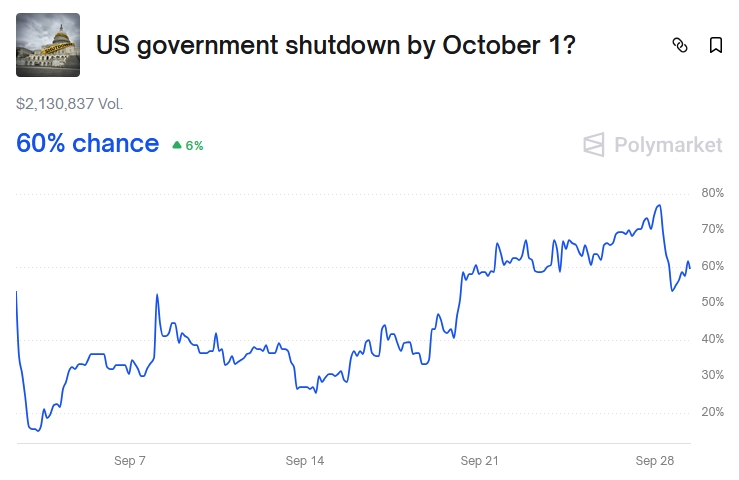

As a result, Polymarket, a leading prediction platform, showed the odds of a U.S. government shutdown falling from a peak of 77% to around 60%.

U.S. Government Shutdown Probability, Source: Polymarket

As TradingKey previously noted, investors are closely watching whether key economic reports — such as the September Nonfarm Payrolls (Oct 3) and CPI (Oct 15) — will be delayed due to a potential shutdown.

However, given that alternative indicators like ADP and jobless claims have pointed to weaker labor data, and economists still expect September nonfarm payrolls to come in near 50,000 (in line with recent trends), markets may enter a “no news is good news” phase — where even silence supports bullish momentum.

The political brinkmanship has pushed the crisis to the final days of September — coinciding with the last window for Wall Street to break the “September Effect.”

Historically, September is the worst-performing month for the S&P 500, averaging a decline of over 1% over decades. But so far in 2025, the index is up 3% this month and trading near all-time highs.

Gary Schlossberg, Senior Market Strategist at Wells Fargo, had warned that a shutdown on October 1 could delay the release of the September jobs and CPI reports, potentially disrupting market expectations.

He added that this time, the impact could be broader than the 2018–2019 partial shutdown, as more agencies face funding gaps due to Congress failing to pass any of the 12 appropriations bills.

Kevin Gordon, Senior Investment Strategist at Charles Schwab, said:

“This one could come at a really unfortunate time because we are supposed to get the jobs report on Friday. If we don't get access to that data, it's going to be a problem."

But Gordon noted that whenever the data arrives, it will likely reflect ongoing softness in hiring, including the impact of buyouts among federal workers earlier this year.

This view aligns with broader economist sentiment: with recent job reports showing weakness and major downward revisions to prior employment figures, a slowing labor market is now widely accepted — reinforcing the Fed’s projected path of two more 25-bp cuts this year.

Even as concerns grow over the sustainability of the “AI closed loop” formed by OpenAI, Oracle, and Nvidia, overall market sentiment remains resilient. Some investors are rotating into underperforming sectors like energy, seeking value amid stretched valuations elsewhere.

Last week, JPMorgan raised its end-2025 S&P 500 target to 7,000, citing strong corporate earnings and supportive monetary policy. While the market may see short-term pullbacks due to seasonal headwinds, extended rallies without correction, elevated retail participation and post-Fed relief selling, JPMorgan maintains strong confidence in the medium-to-long-term outlook.

Recommended Articles