Is TJX Companies a Buy After Their Latest Earnings Report?

Key Points

Growth came across the board and across all income levels.

Its well-oiled growth engine shows no signs of slowing down.

Management also raised guidance, even while remaining conservative in its outlook.

- 10 stocks we like better than TJX Companies ›

Investors looking for signs of life in retail just got a loud one from TJX Companies (NYSE: TJX). The parent company of TJ Maxx, Marshalls, HomeGoods, and Sierra, delivered a solid first quarter for fiscal 2027, significantly beating analyst expectations.

The stock is looking stronger than it has in years. But after such a strong run, is TJX still a buy? The answer increasingly looks like yes -- though not without a few caveats.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

A blowout quarter across the board

Overall, the apparel and home fashions retailer had an extremely good quarter. Net sales increased 9 percent to $14.3 billion, and comparable sales rose 6 percent versus the year-ago quarter.

Adjusted EPS (earnings per share) increased 29 percent to $1.19. That was well above the analysts' estimate of $1.00.

What made the quarter even better was the breadth in growth. Comparable sales grew across all four main divisions, including HomeGoods (+9%), TJX Canada (+7%), Marmaxx (which houses TJ Maxx, Marshalls, and Sierra) (+6%), and TJX International (+4%).

This is impressive because retailers sometimes have a strong quarter because of one hot category or temporary promotions. TJX's momentum looked much broader.

What's noteworthy is that management repeatedly pointed out during the earnings call that, across both the apparel and home categories, growth was driven by all income levels and regions, and by both higher customer traffic and larger basket sizes.

Plainly put, TJX isn't just winning over lower-income shoppers. Higher-income consumers are shopping there too.

Image source: Getty Images. TJX Companies' growth has been driven by a broad shopper profile.

The growth engine: exceptional merchandise availability

TJX's business strategy has been different from that of most traditional retailers, and it may be one of the reasons why it has been successful.

Traditional retailers purchase their inventory months in advance, relying almost exclusively on pre-planned product assortment strategies. In contrast, TJX purchases products opportunistically throughout the year. Its 1,400-plus buyers scour the market all through the year to find the best discounts across all brands. The retailer adds thousands of new vendors each year and is often the first call for these vendors looking to offload excess inventory.

Management stated that merchandise availability right now is "off the charts," and used that phrase multiple times during the conference call.

Margins up, guidance raised again

TJX's pre-tax margin widened to 12%, a 170 basis-point increase versus last year. Gross margin expanded 180 basis points to 31.3%. In the retail industry, those are substantial gains.

Analysts, obviously, probed whether those margin improvements were sustainable or simply boosted by temporary factors like fuel hedges and freight timing. While management acknowledged that favorable fuel hedges helped the quarter, it also stressed that merchandise margins were stronger than expected and that expense leverage from higher sales played a major role.

Importantly, TJX raised its full-year guidance. Comparable sales growth is now expected at 3% to 4%, while the outlook for earnings per share (EPS) is now between $5.08 and $5.15 for fiscal 2027.

However, management indicated it did not fully capitalize on the upside in the first quarter for its full-year guidance. Specifically, CFO John Klinger noted that the company assumed that elevated diesel prices would persist throughout fiscal 2027. Therefore, should diesel prices fall later in the year, margins potentially could expand beyond the current guidance. https://www.fool.com/earnings/call-transcripts/2026/05/20/tjx-tjx-q1-2027-earnings-call-transcript/

International expansion is also a key part of the story

One underappreciated part of the TJX story may be international expansion. The company now operates in 10 countries and recently opened its first store in Spain, where management described customer response as "terrific."

Investors have long viewed TJX primarily as a mature U.S. retailer. This quarter suggests management sees far more runway ahead.

So, is TJX Companies a Buy?

No retailer is immune to risks associated with the current economic climate. TJX still faces wage inflation, freight and fuel volatility, and the possibility that consumers eventually pull back on discretionary spending.

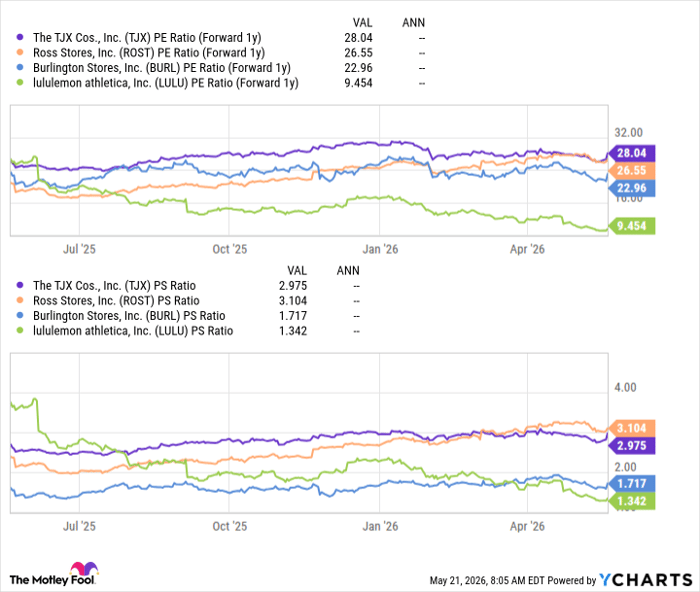

The stock isn't relatively cheap among apparel stocks, either. Nevertheless, yesterday's earnings announcement reinforced several key strengths, such as strong traffic trends, expanding margins, excellent inventory access, and possibly the most underrated factor -- continuing demand across all income levels.

TJX PE Ratio (Forward 1y) data by YCharts.

Furthermore, management stressed the importance of investing in long-term growth. The consistency and breadth of the latest quarterly results underscore that.

The market clearly liked what it saw. Shares of TJX rose roughly 5.7% in yesterday's trading session following the earnings release.

TJX Companies offers a compelling case for long-term investors seeking a retailer that's consistent in execution, has resilient consumer demand, generates significantly higher profitability, and presents multiple paths toward future growth.

Should you buy stock in TJX Companies right now?

Before you buy stock in TJX Companies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and TJX Companies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $475,063!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,369,991!*

Now, it’s worth noting Stock Advisor’s total average return is 996% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 21, 2026.

Isac Simon has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lululemon Athletica Inc. and TJX Companies. The Motley Fool has a disclosure policy.

Recommended Articles