Canopy Growth's Stock Just Dropped -- Here's Why I'm Still Not Buying

Key Points

The company has struggled to improve its business -- and especially to earn a profit.

It also has a habit of making dilutive secondary share issues.

- 10 stocks we like better than Canopy Growth ›

For anyone who has observed Canopy Growth (NASDAQ: CGC) during the past few years, it won't be shocking to learn that the marijuana company's stock is diving in May. Since the start of the month, it's down by more than 12% as of this writing, against the nearly 2% gain of the bellwether S&P 500 index.

Years of net losses and struggles with sales growth have taken their toll on investor sentiment. Yet there are Canopy Growth bulls in the investing community that point to a recent acquisition, in particular, as a cause for hope.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

I'm not buying that view, and I'm not buying the company's stock. Read on for why.

A business full of headaches

The company's home country, Canada, began full legalization of recreational weed in 2018. That was also the golden era of cannabis companies, as investors flocked to weed stocks at the dawn of this seemingly glorious new market.

Except that the market wasn't so impressive. Regulatory bottlenecks in Canada hampered its development, while persistent gray- and black-market competition and oversupply left the company constantly struggling. At least it wasn't alone in that respect; north-of-the-border peers like Tilray Brands have also had a tough time prospering in such an environment.

The vast and wealthy U.S. market -- where Canopy Growth has a presence through its Canopy USA affiliate -- is always tantalizing. This is more promise than reality, however. De facto legalization is frustratingly piecemeal, and reform has occurred in fits and starts, at best.

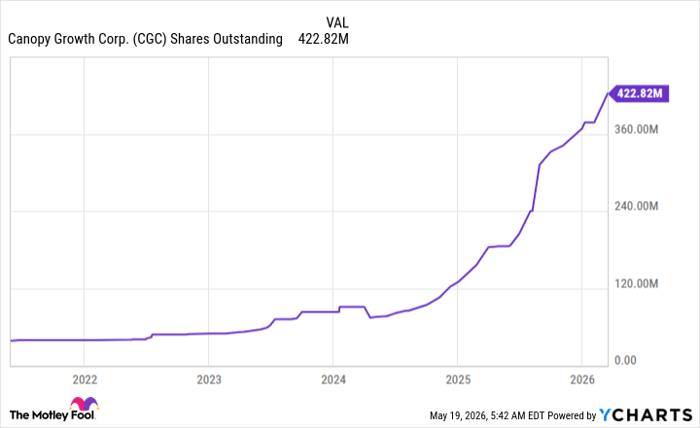

So, in both its home country and here, Canopy Growth remains challenged to eke out any growth and reduce the flow of red ink on the bottom line. Over the years, it has tried numerous times to shore up its finances with fresh secondary-share issues, but the dilution has been significant for existing shareholders and has driven away potential investors.

CGC Shares Outstanding data by YCharts.

Going the acquisition route

In March, Canopy Growth closed its acquisition of Quebec-based medical marijuana company MTL Cannabis. The notable factor in this deal is that MTL is an outlier: It's a pure-play weed company that has posted more than a few bottom-line profits.

On that basis alone, investors were excited about its potential to improve Canopy Growth's financials. I'm not as impressed; I don't think the deal -- paid with a mix of cash and stock and valued at $125 million Canadian dollars ($91 million) -- will be a game changer for the buyer.

In MTL's four reported quarters leading up to the acquisition, its gross product revenue ranged from just under C$15 million to nearly C$19 million. In two of the four quarters, it posted net income, with those profits coming in just shy of C$490,000 and slightly more than C$1 million.

Image Source: Getty Images.

Meanwhile, if we look at Canopy Growth's latest quarterly results, the pot company's top line was C$54.5 million, and its net loss (which, to give the company its due, was considerably narrower than the prior-year shortfall) amounted to almost C$45.8 million.

So even when MTL posts bottom-line profits, these surely won't do much to mitigate the chronic and deep losses of its new parent.

Not so high on the sector

Given that, I predict more dilutive share issues for Canopy Growth, as this is the company's classic go-to reaction to financial stress. I don't see many accretive deals for it in the future -- its resources are limited, and it's doubtful there are scores of (at least occasionally) profitable operators in the market ripe for acquisition.

I also don't envision the numerous challenges in Canada dissipating anytime soon, if ever. The U.S. might never enact a complete national legalization of recreational marijuana. Yet even if it does, the country has more than its share of domestic weed companies that would pounce on any meaningful legalization move.

Plus, those U.S. companies just got a break from the federal government, which last month rescheduled medical pot to a more lenient status. This change included the elimination of the Internal Revenue Service's Section 280E rule -- a move that drastically eased the tax burden on the country's multistate operators.

So, in sum, there are numerous compelling reasons to stay away from Canopy Growth stock specifically, and -- save for a very few clever companies -- the broader marijuana sector generally. There are better places to park our precious investment money.

Should you buy stock in Canopy Growth right now?

Before you buy stock in Canopy Growth, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Canopy Growth wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $481,750!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,352,457!*

Now, it’s worth noting Stock Advisor’s total average return is 990% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 21, 2026.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool recommends Tilray Brands. The Motley Fool has a disclosure policy.

Recommended Articles