Prediction Markets Now Behave Like Stock Trading Platforms

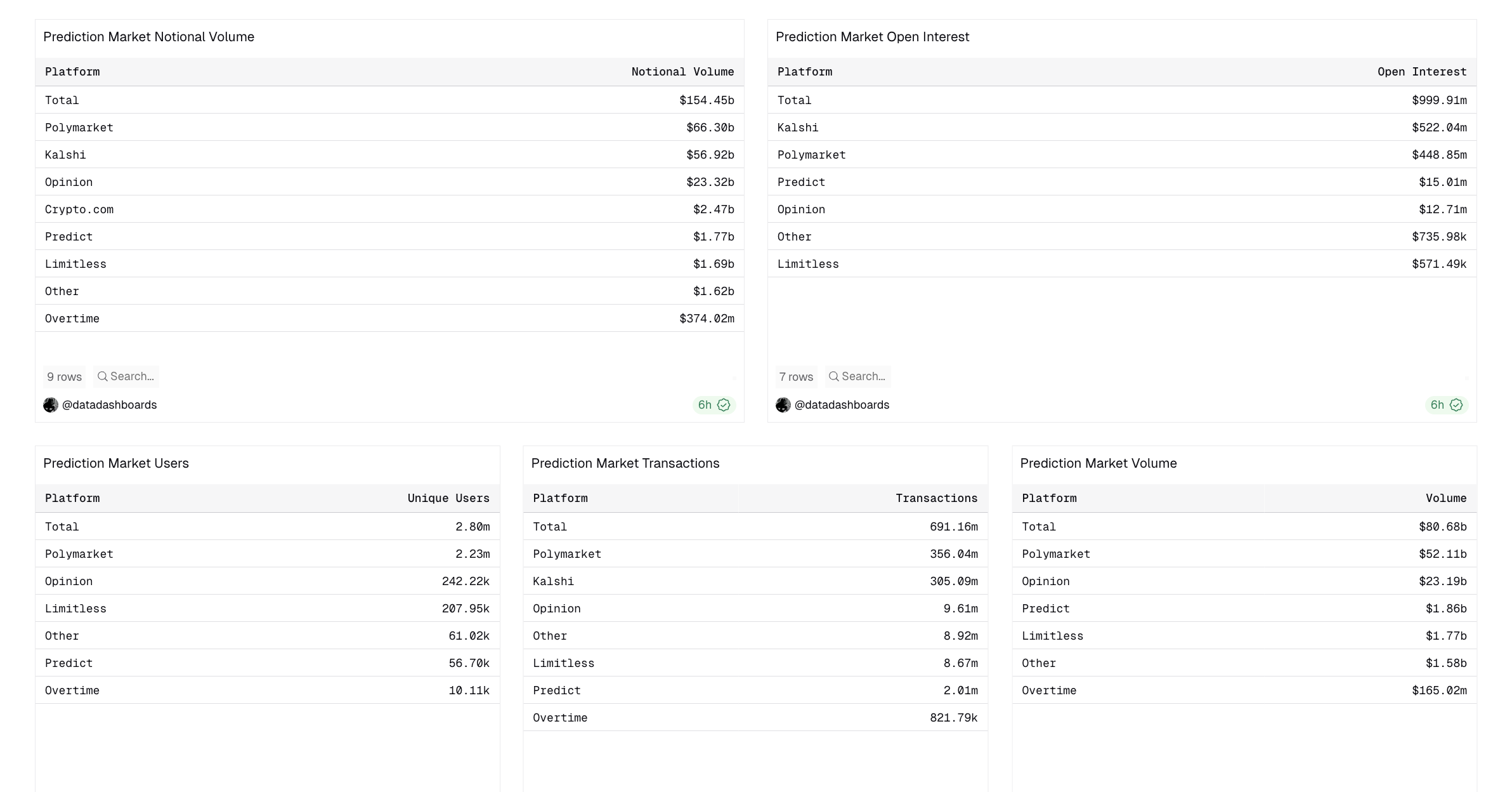

Prediction markets have processed more than $154 billion in total volume, with daily trading on Polymarket alone often exceeding $300 million.

That scale forces a more important question. These platforms no longer look like niche betting venues. They increasingly resemble something closer to retail trading.

This analysis uses on-chain data, primarily from Polymarket—the largest platform by users and transactions in a market dominated by a Polymarket–Kalshi duopoly—to test that shift directly.

Current Notional Volume Spread: Dune

Current Notional Volume Spread: Dune

$10 Trades Are Defining the Market

Across four dimensions, who participates, how they behave, how capital moves, and at what scale, the volume growth pattern tells a consistent story.

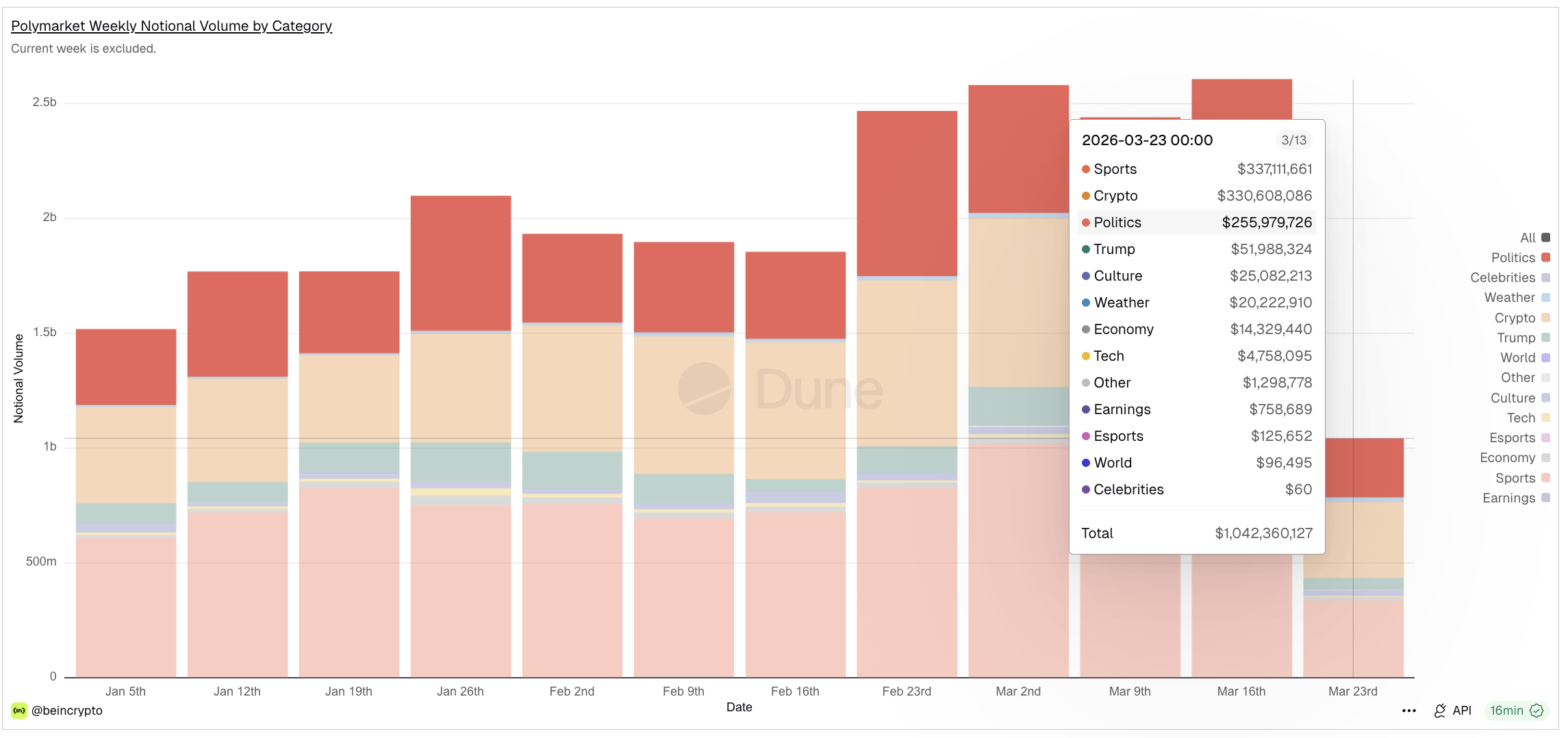

And the category mix reinforces the framing: crypto and politics (excluding sports) now lead weekly volume on Polymarket, with the economy and earnings categories growing alongside them. These are not traditional gambling categories. They are finance-adjacent verticals.

Notably, sports event contracts are already being offered as CFTC-regulated financial products by Kalshi and distributed through Robinhood’s Predictions Hub, placing them alongside stocks, options, and crypto within the same brokerage interface.

Prediction Markets’ Growing Categories: Dune

Prediction Markets’ Growing Categories: Dune

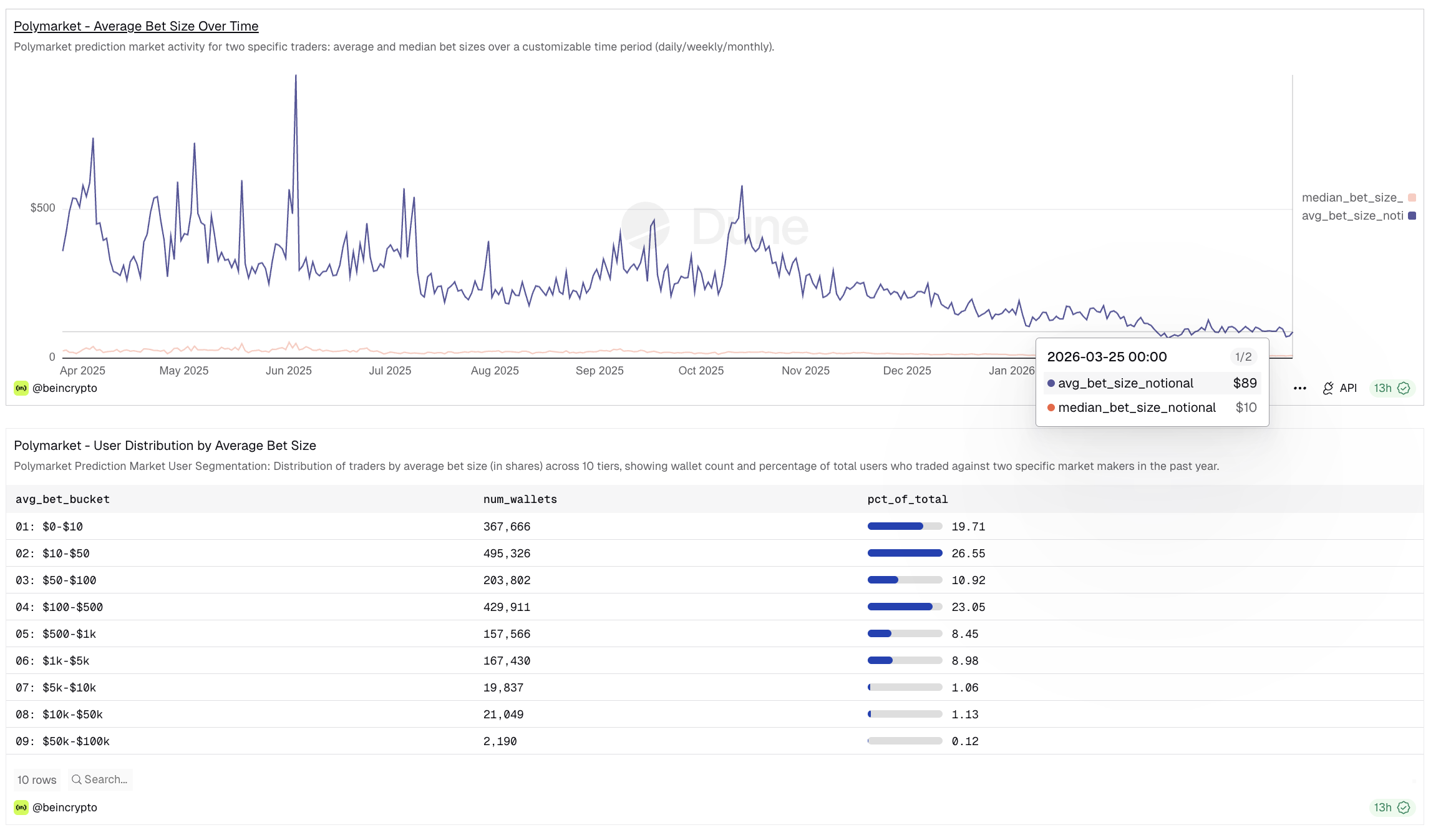

The most revealing signal is not how much money flows through prediction markets. It is who is placing the trades.

On Polymarket, the median bet size is $10, according to BeInCrypto’s exclusive dashboard. The average sits at $89, but that figure is pulled upward by a thin tail of large participants.

The underlying distribution paints a clearer picture: roughly 20% of all wallets trade in the $0 to $10 range, another 27% fall between $10 and $50, and about 11% sit in the $50 to $100 bracket.

In total, over 57% of users trade for less than $100, and more than 80% trade for less than $500.

Polymarket User Distribution by Average Bet Size: Dune

Polymarket User Distribution by Average Bet Size: Dune

This is not a market shaped by whales. It is a market built on small, individual participants deploying modest amounts. The pattern mirrors what defined the rise of retail stock trading.

Robinhood, for comparison, reported a median account size of $240, with the average around $5,000, according to CEO Vlad Tenev in 2021. The structural similarity is hard to miss: prediction markets are attracting the same class of small participants that reshaped equities over the past five years.

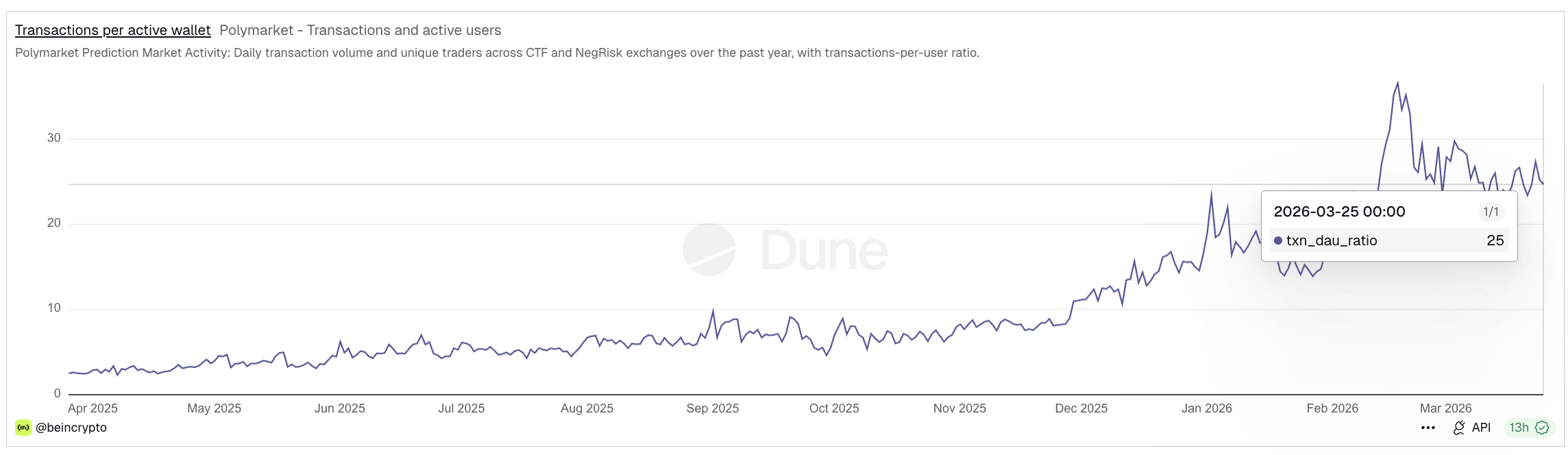

Users are Acting Like Traders, Not Bettors

Participation alone does not distinguish a financial platform from a betting one. Frequency of interaction does.

A bettor places a wager and waits. A trader enters positions, adjusts exposure, exits, and re-enters. The transactions-per-active-user ratio captures this distinction directly.

On Polymarket, this ratio currently stands at approximately 25 transactions per daily active user, meaning the average active participant executes 25 trades per day. Earlier this year, the figure peaked near 37.

Polymarket Transactions Per Active Wallet: Dune

Polymarket Transactions Per Active Wallet: Dune

For context, through most of mid-2025, the ratio hovered between 3 and 5. The structural jump beginning in late 2025 represents a clear behavioral shift: users are no longer placing single predictions and walking away. They are actively managing positions across multiple markets.

This pattern has a direct parallel in crypto markets. A Kaiko research report on Binance found that the exchange processed 61.9 million trades against $20 billion in spot volume on a single snapshot day in December 2025, implying small average trade sizes and frequent execution across its 300 million registered accounts.

High-frequency, small-size trading is the behavioral signature of retail finance, whether the underlying asset is a stock, a token, or a prediction contract.

Capital Is Constantly in Motion

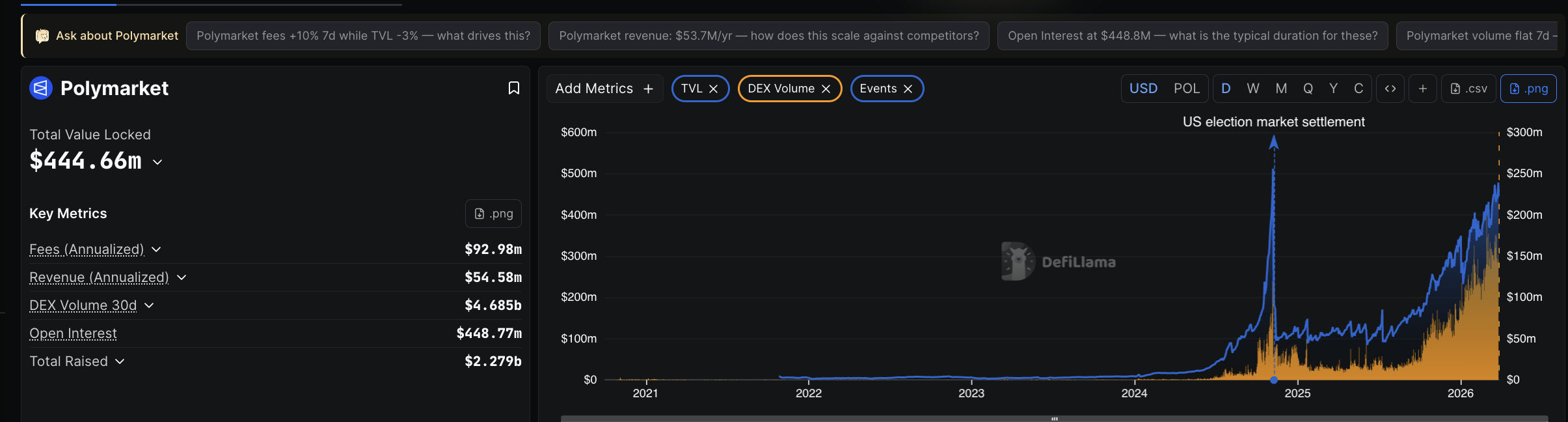

If users behave like traders, the capital dynamics should confirm it. They do. Polymarket currently holds approximately $445 million in total value locked, while open interest stands at roughly $477 million.

The near-parity between these two figures carries a specific implication: virtually all deposited capital is actively deployed in live positions rather than sitting idle. This is not passive liquidity. It is working capital.

Polymarket TVL; DeFillama

Polymarket TVL; DeFillama

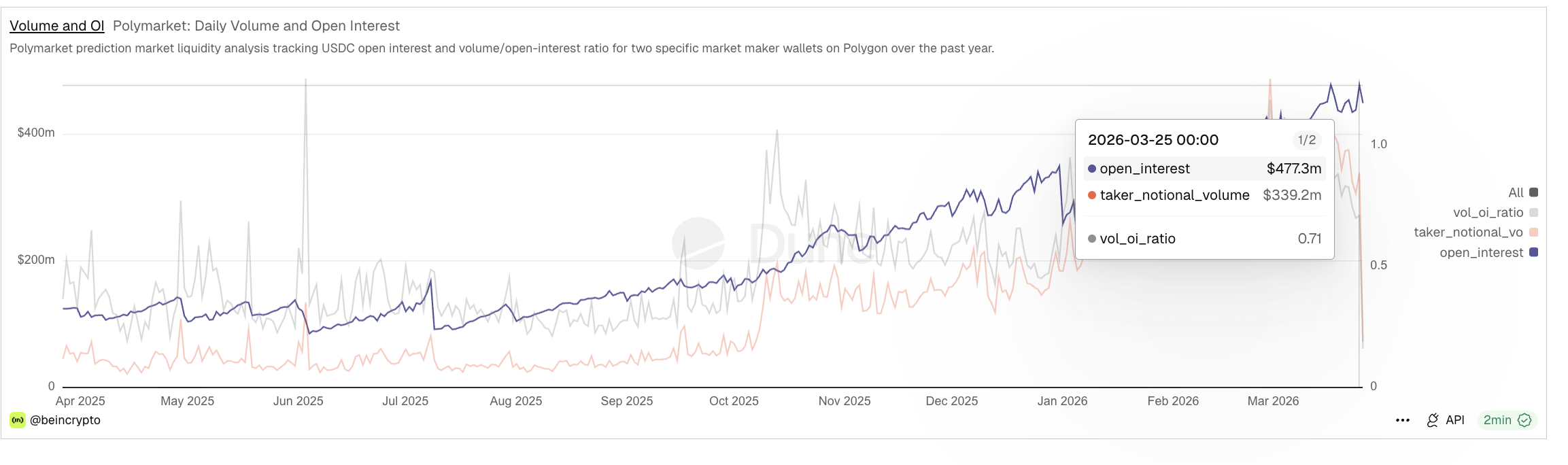

The volume-to-open-interest ratio reinforces the point. With daily taker volume around $339 million and open interest at $477 million, the ratio is 0.71. Capital is not just deployed. It is rotating.

Positions are being opened, closed, and re-entered at a pace that suggests continuous portfolio management rather than static, event-dependent exposure. A low vol-OI ratio would have suggested more betting-like activity.

Volume And OI: Dune

Volume And OI: Dune

In a traditional betting market, capital tends to lock in and wait for resolution. Here, it circulates. That distinction is material: it signals a system in which participants treat capital as a tool for ongoing risk adjustment, not a one-time stake in a single outcome.

This Is No Longer Event-Driven Growth

The behavioral and capital patterns described above would be noteworthy even at modest volumes. But they are not operating at modest volumes.

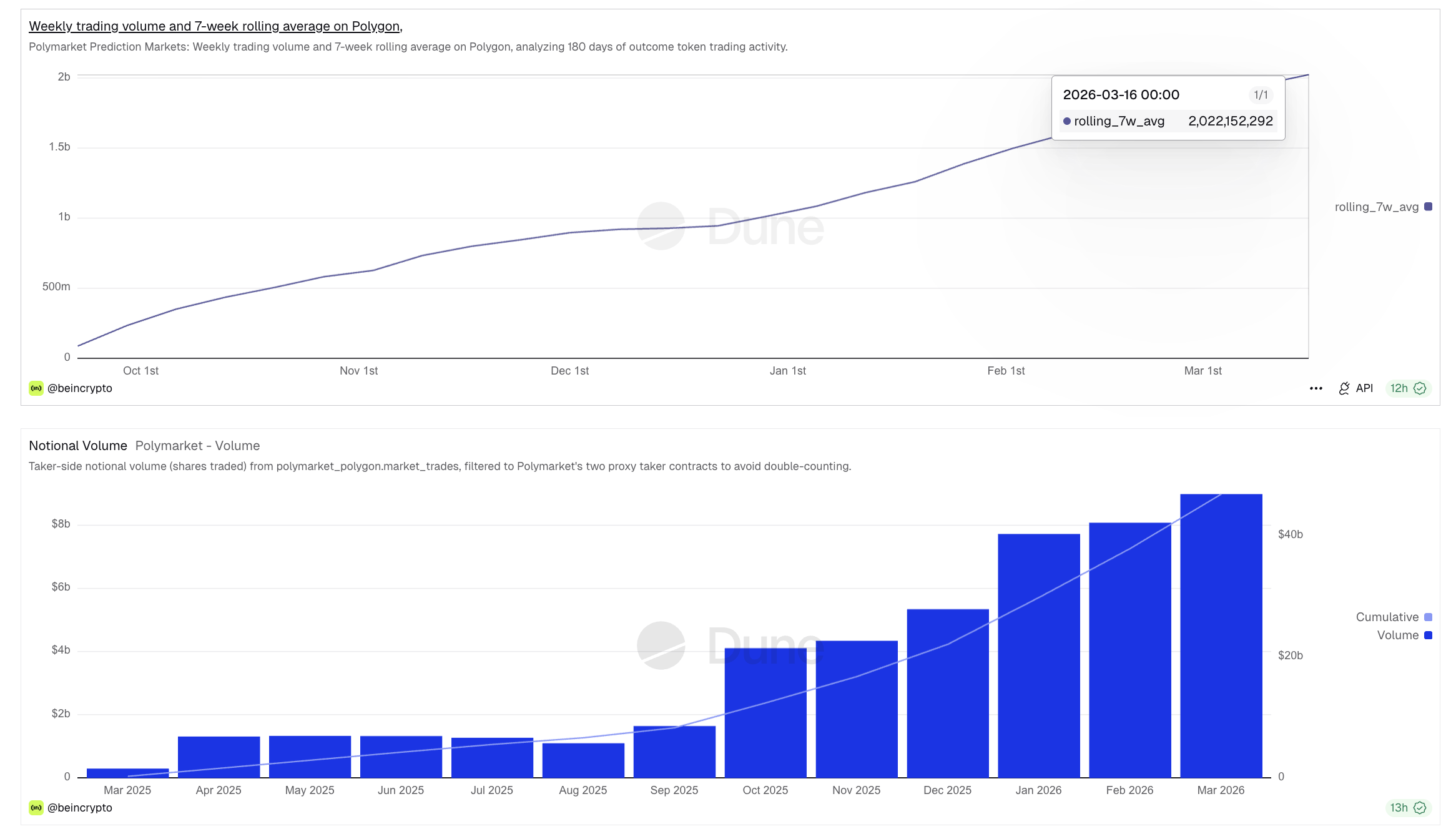

Polymarket’s weekly notional volume has consistently exceeded $1 billion through Q1 2026, with recent weeks surpassing $2.5 billion. The 7-week rolling average has crossed $2 billion.

Monthly volumes have climbed from around $1 billion in mid-2025 to over $8 billion by March 2026. The growth trajectory is not driven by any single event cycle.

Rolling Average: Dune

Rolling Average: Dune

Volume is diversifying across categories: sports, crypto, and politics. Each contributed substantially in the most recent weekly data, with economy, weather, and culture adding further breadth.

This diversification is what separates structural growth from event-driven spikes. A presidential election creates a temporary surge.

Sustained, multi-category volume growth across sports, crypto, macro, and culture points to a user base that engages with prediction markets regularly, not just occasionally, as a typical retail habit.

What the Prediction Markets’ Data Says

Each dimension reinforces the next in a single causal chain. The majority of participants are small, retail-sized users. Those users trade frequently, not once, but dozens of times per session.

The capital they deploy is almost entirely active, rotating through positions rather than sitting idle. And this behavior is occurring at billions of dollars in monthly volume, across a broadening set of categories.

When small users dominate participation, execute frequent trades, and keep capital constantly in play at scale, the system begins to resemble a retail financial market rather than a betting platform.

Prediction markets are no longer just mechanisms for forecasting outcomes. They are changing into retail trading systems for real-world events, platforms where participants express views, manage risk, and deploy capital with a frequency and discipline that mirrors stock markets.

Recommended Articles