OppFi: The Fintech Profit Story You Missed

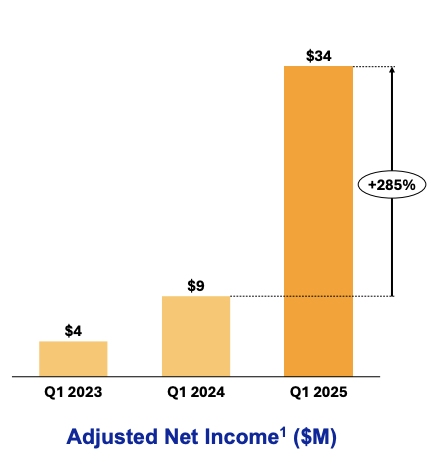

- Adjusted net income rose 285% year-over-year to $33.8 million, with full-year EPS guidance raised to $1.18–1.26.

- Net charge-offs declined from 48% to 34.6% of revenue, driven by Model 6’s AI-based underwriting improvements.

- Operating costs fell 16.6% year-over-year, with G&A down 37.5% and tech expenses reduced by 23.9%.

- OppFi trades at 0.60x forward sales and 10.85x forward earnings, significantly below peers with weaker fundamentals and slower growth.

While most are reassured by the frenzy of fintech hype cycles and software spec multiples, OppFi Inc. (OPFI) is an exception, an undervalued, profitable, and capital-efficient digital lender with record-breaking Q1 2025 results that defy conventional wisdom.

With only a forward P/E of 11.7x and with the revenue base that’s advancing in double digits and year-to-date adjusted net income up by 285%, the valuation of OppFi belies skepticism with respect to sustainability. But underneath the veil, the company’s combination of high-yield lending economics, AI-underwriting with Model 6, and low-cost origination channels betrays a structurally favorable business model built for high-return, disciplined growth.

Source: Q1 2025 Earnings Presentation

At the heart of the contrarian thesis lies a decisive inflection point: OppFi is no longer merely a subprime consumer lender; it’s transforming into a capital-light, data-intensive fintech platform. That transformation is evidenced by a dramatic net charge-off decline (from 48% to 35% of revenue YoY), rising auto-approval percentages (79% now), and 630-bps YoY yield expansion, driving net revenue up 44% despite only 10% topline growth. With a robust balance sheet, cost discipline, and rising ROE trajectory, the market significantly underappreciates OppFi’s operational leverage and long-term free cash flow generation.

.jpg)

Source: Q1 2025 Earnings Presentation

Valuation dislocation is exaggerated by valuation. While fintech peers struggle for break-even and burn funds, OppFi changes hands at 0.60x forward Price/Sales and 10.85x forward earnings. However, the business has promised 2025 adjusted net income of $106–113 million (vs. $34 million in Q1 alone), implying the present market cap misprices earnings visibility and risk management momentum. The gap between headline figures and operational meat is the backdrop for an attractive rerating as the market digests this silent profitability revolution.

Financial Plumbing Meets Algorithmic Discipline: The New OppFi

OppFi’s shift from a high-yield niche lending platform to a precision fintech platform has gone into overdrive during 2025. In Q1 2025, the firm originating net loans amounted to $189 million, 16% YoY growth, with the balance retained by the firm amounting to $169 million. In revenue, the figure amounted to $140.3 million, representing 10.1% growth, the highest ever quarterly revenue recorded by the firm. Better yet, net revenue went up by 43.7% to $91 million, representing both credit quality improvement and stronger underwriting margin through Model 6.

.jpg)

Source: Q1 2025 Earnings Presentation

Model 6, the proprietary credit decisioning engine at OppFi, utilizing machine learning and behavioral data, enabled a remarkable 1,330 basis point net charge-off rate reduction YoY (48% → 34.6%). While maintaining that, auto-approvals rose 600 bps YoY to 79%, reducing underwriting friction, operational cost, and time-to-decision. This confluence of factors has squeezed out cost structures and initiated margin expansion without sacrificing risk-adjusted return.

.jpg)

Source: Q1 2025 Earnings Presentation

Operational leverage becomes even more apparent with the trends in the company’s spending. Total spending declined 16.6% YoY despite reducing G&A by 37.5% and reducing tech and analytics spending by 23.9%, despite modest increases by customer operations and marketing. Even with interest charges reduced to only 7.3% of revenue, due partially to opportunistic deleveraging, Q1 included the payoff of $30.8 million in debt. With cash at hand of $91 million and available capacity of $237 million, OppFi is poised to scale without dilution, something remarkably unusual among high-growth players in finance.

.jpg)

Source: Q1 2025 Earnings Presentation

Algorithmically precise credit models with lean operations and low yields (135.8% average annualized), that's how OppFi compounds adjusted EPS at scale. First-quarter adjusted net income of $33.8 million and increased full-year EPS guidance to $1.18–1.26 put the company on course toward record profitability. Recall that such figures are GAAP-noise-free from changes in warrant liability and fair-value remeasurements, supporting the credibility of the growth indicator.

Fintech Comparable Don't Pass the OppFi Test

Almost all investors have mistakenly analogized OppFi with conventional subprime lenders or unprofitable neo-banks. The improper classification masks what is an unusual, capital-light, vertically integrated business model. While pure originators that rely on expensive third-party capital or marketplaces like Upstart only originate, and Upstart takes economics, OppFi originates with its bank partnerships and retains receivables, taking full yield economics with leverage on capital deployment.

While Upstart and Oportun have seen spreads decrease or losses expand due to model brittleness, Model 6 at OppFi has delivered the opposite: robust credit quality amidst macro ambiguity. The market doesn’t know yet, but OppFi’s forward EV/EBITDA multiple is below 10x, significantly lower than the fintech peers that trade at 12–15x with their weaker fundamentals and GAAP-negative margins.

Price-to-sales ratios are even more revealing. OppFi trades at just 0.60x forward sales versus the sector median of 2.71x, the equivalent of a 78% discount. Even with growth-rate adjustments, OppFi’s PEG multiple is probably worse than 0.5x given its increased full-year EPS estimate of $1.22 midpoint. Its price/book ratio at 15.04x also appears rich, but that’s because of legacy structural issues like dual-share class distortions and warrant-based accounting. When such distortions are reconciled by tangible equity and normalized capital structure, the ROE by adjusted earnings basis for OppFi points towards a sustainable high teens’ return that warrants re-rating towards a more normalized P/B multiple over the long term.

Compared with most high-profile fintechs, most are continuing to rely on equity capital and lag in operating leverage. OppFi, by contrast, now produces sufficient quarterly adjusted net income to self-fund growth, yet accumulates more than $600 million of total funding capacity. Its judicious deployment of capital, inferred by the $28.1 million special dividend paid out during Q1, indicates confidence in cash generation and latitude to return capital without sacrificing reinvestment capacity.

.jpg)

Source: Q1 2025 Earnings Presentation

The Flywheel Is Spinning: Profit Accumulates, Risk Is Contracted

What makes the OppFi model supportable isn’t just earnings growth; it’s the quality growth. The company has deep-seated risk controls, low CAC, and scalable infrastructure. Its subsidiary, Bitty, which provides revenue-based financing for small business, gives a short-duration, revenue-based, high-yield complement to the consumer lending engine. Bitty, small yet, gives diversification of product and optionality with no balance-sheet risk because it’s substantially through equity method investment.

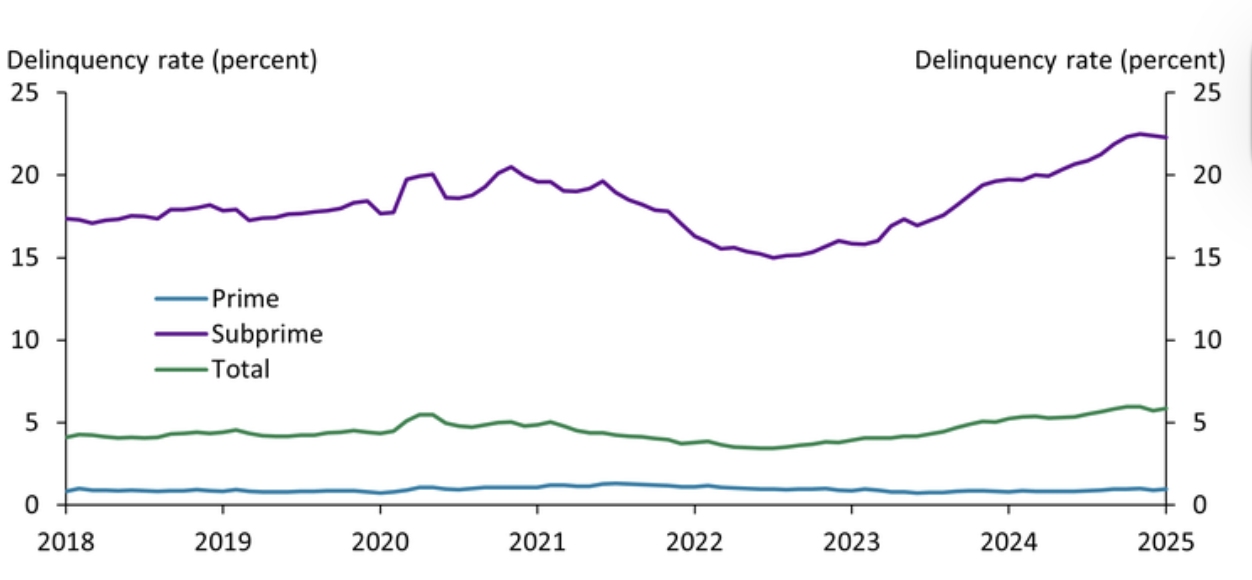

OppFi's underwriting discipline shone brightest during Q1. Despite macro worries, customer acquisition was stable, repayment rates remained stable, and automation approvals went up.

Source: Federal Reserve Bank of Kansas City, US Subprime Lending Delinquency Rates

Analysts at the earnings call wondered about the potential ease of credit, but the management was firm: growth would remain risk-adjusted and disciplined, with a concentration on ROI, not originations. The decision to add more direct sales avenues with unchanged auto-approval percentages leans toward optimism in unit economics over volume desperation.

It keeps $288 million of debt but is ever more secured by cash flows generated by operations. Debt repayment, facility expansion, and rising equity value all suggest greater financial flexibility. Importantly, that provides OppFi the wherewithal to selectively repurchase shares, redeem capital, or execute strategic tuck-in acquisitions, any of which could accrete valuation multiples and EPS with the passage of time.

By far the strongest evidence of this flywheel effect is the stronger 2025 adjusted net income guide: now $106–113 million, compared with previous guidance at $95–97 million. At the midpoint of $109.5 million, this represents a forward P/E of ~11.7x at the current post-market quote of $13.04, a valuation that fails to account for upside optionality or earnings defensibility during stressed credit markets.

Valuation Repricing Ahead: Why OppFi’s Discount Won’t Last Forever

From a valuation perspective, OppFi (NYSE: OPFI) continues to look meaningfully undervalued when stacked against both fintech and traditional subprime lending peers. Now trading at $14.58, and with forward Non-GAAP EPS at $1.24 (midpoint between 11.74x and 12.03x P/E), the company sits at a forward P/E of roughly 11.8x. That’s modest, especially when you consider that other niche consumer lenders with slower EPS growth and thinner margins, like Enova or Oportun, command 12–14x forward earnings multiples.

What’s more, OppFi’s valuation ratios reinforce the disconnect. With a Price/Sales (TTM) of 1.01 and Price/Cash Flow (TTM) at just 1.14, both significantly below sector medians (66–88% lower), it’s clear the market isn’t fully pricing in its cash-generating potential. Yes, Price/Book remains elevated due to its capital-light, tech-enabled model, but that’s a feature, not a bug.

With balance sheet improvements, deleveraging trends, and a self-funded growth strategy firmly in play, there’s ample room for multiple expansion. The real re-rating catalyst? Sustained beat-and-raise quarters, margin expansion, and growing contributions from Bitty. Until then, the market is offering OppFi at a discount that doesn’t match its trajectory.

Risks: Regulation and Concentration

There are risks despite the tempting setup. OppFi’s vulnerability to regulation, viz., California, whose legal judgment could affect the rate export model, constitutes structural risk. Legal approach by management and partnership models are buffers, but persistent ambiguity could dampen valuation growth.

Cyclicality is yet another consideration. While Model 6 has performed well, sustained high inflation, deterioration in job markets, or political measures (e.g., rate caps) could damage risk-adjusted returns or necessitate more stringent underwriting. The concentration of revenues among subprime consumers gives yet another area of vulnerability, although existing data reveals charge-off behavior improvement.

Finally, equity dilution is a hidden risk due to previous Class V share structures, but the earnout units given up in 2024 have eliminated one source of difficulty. In the event that OppFi delivers sustained EPS compounding without needing outside capital, this risk fades naturally.

Conclusion

OppFi isn’t priced like a high-ROE, capital-effective fintech, but that’s exactly what it’s becoming. Its AI-based credit discipline, high-yield receivables engine, and rising operating leverage are delivering record profitability just when most fintechs are still loss-making. When reality catches up with the market for a self-funding, sustainable model of profits, we think re-rating is inevitable. For those eager to peer through line-of-business stigma and GAAP noise, we believe we have here a rare asymmetric opportunity in which risk is going down yet upside potential is mispriced.

Copyleaks Report: https://app.copyleaks.com/report/lhbdvwhkowt64dpy/preview?key=bke8tcjz5sahf3yc&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

.png)

Get Started

Recommended Articles