Pop Mart Eyes Western Markets — Can It Challenge Japan’s Bandai?

TradingKey - At the close, Pop Mart (09992.HK) rose 4.25% to HKD 269.8, with multiple sessions hitting new highs this month.

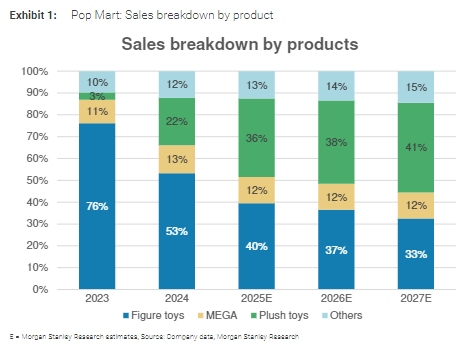

Morgan Stanley pointed out that although the market has largely priced in Pop Mart’s strong growth expectations for 2025, its long-term business expansion potential remains underappreciated. The core rationale is that product strength serves as the key driver behind Pop Mart’s “viral” spread on social media platforms. As long as the company continues to launch attractive new products, it still holds the potential to exceed market expectations.

In addition, Pop Mart’s impressive performance in overseas markets has also helped drive momentum in its domestic market. Morgan Stanley forecasts that by 2028 to 2029 , Pop Mart’s sales in the North American market could reach levels comparable to those in mainland China — marking a phase of substantial returns from its global expansion strategy.

[Pop Mart Sales Breakdown By Product, Source: WallStreet]

The report raised Pop Mart’s target price significantly — by 35% , from HKD 224 to HKD 302 — while maintaining an “Overweight” rating.

In a broader entertainment industry report, Nomura noted that Pop Mart’s international success signals the early emergence of an “Asian designer toy duopoly ” — with the Chinese brand (Pop Mart) now directly competing against the Japanese leader (Bandai) in the European and U.S. markets.

However, whether Pop Mart can win sustained favor from investors depends on whether it can move beyond its reliance on short-cycle blind box models and establish a mature and independent IP identity of its own, according to some analysts.

Recommended Articles