Intel's Stellar Q3: First Earnings Since CHIPS Act Funding Blow Away Estimates, Stock Surges 8% After Hours

TradingKey - Chip giant Intel released its first quarterly earnings report since the U.S. government became a shareholder, with core financial metrics comprehensively exceeding market expectations and achieving profitability for the first time since the end of 2023, providing strong evidence for its ongoing turnaround strategy.

After years of difficulties, major restructuring, leadership changes, and the U.S. government becoming a significant shareholder (holding approximately 10%), this earnings report initially validates Intel's recovery efforts, boosting market confidence and driving the company's stock up nearly 8% in after-hours trading.

Earnings Beat Expectations

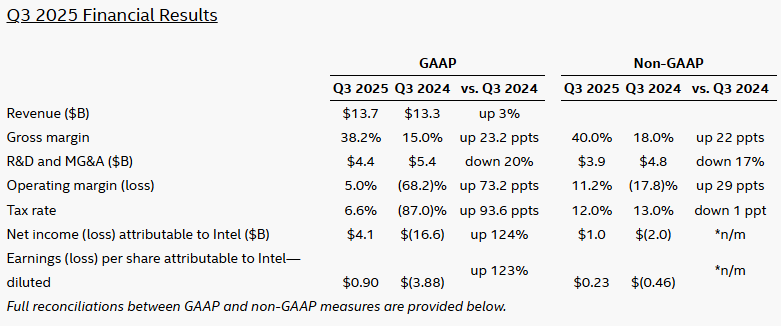

Financial data showed that Intel's third-quarter revenue reached $13.7 billion, not only exceeding the company's previous guidance range upper limit ($12.6 billion to $13.6 billion) but also significantly surpassing analysts' consensus estimates of $13.2 billion. The quarter's revenue grew 3% year-over-year, marking the company's first quarterly revenue growth since Q1 2022 — after a year and a half — and reversing the previous quarter's zero growth trend.

Under non-GAAP (Generally Accepted Accounting Principles) measures, adjusted earnings per share (EPS) came in at $0.23, far exceeding analysts' expectations of $0.01 and showing significant improvement compared to the previous year's loss of $0.46 per share.

Third-quarter net income reported $4.1 billion, with earnings per share of 90 cents, compared to a net loss of $16.6 billion in the same period last year.

On a call with analysts, Intel Chief Executive Lip-Bu Tan highlighted “the steady progress we are making to rebuild the company” and said his priority is keeping up the pace toward making its businesses more efficient.

“While we still have a long way to go, we are taking the right steps,” he said.

Regarding forward guidance, Intel expects fourth-quarter revenue to be between $12.8 billion and $13.8 billion; adjusted gross margin of 36.5%; and adjusted EPS of $0.08, below the market estimate of $0.10.

The company explained that its fourth-quarter outlook is lower than analyst expectations because its forecast does not include revenue from Altera. Considering this situation, Intel's guidance should be better than it appears. Altera is a semiconductor company under Intel that the company partially divested during the third quarter.

PC Business Leads Recovery

Business-level analysis shows that Intel's core PC processor business (CCG division) emerged as the main growth engine, with third-quarter revenue growing 5% year-over-year, driving the overall revenue recovery.

Prior to Intel's earnings release, some analysts had already anticipated that Intel's PC processor sales might outperform expectations.

John Vinh, an analyst at KeyBanc Capital Markets, wrote in a report this week: "We expect Intel to report better results and higher guidance. Intel should benefit from broad-based growth in the server business and customer upgrades to Granite Rapids server processors."

Intel's Chief Financial Officer (CFO) Dave Zinsner emphasized that strong chip demand in the third quarter led to supply constraints at the company. "We are currently supply-constrained, and we expect this trend to continue into 2026."

He noted one reason is that data center operators realize they need to upgrade central processing units (CPUs) to keep pace with advanced AI chips.

Foundry Business

Despite signs of recovery in the core PC business, Intel's foundry manufacturing services (IFS) business remains the focus and primary concern for investors. The division reported an operating loss of $2.3 billion in the third quarter, though improved from the massive $5.8 billion loss in the same period last year, it was still higher than the market-expected $2.2 billion.

Over the past three months, Intel has secured strategic investments from NVIDIA ($5 billion), U.S. federal government CHIPS Act funding ($8.9 billion), and SoftBank ($2 billion), totaling $15.9 billion in external financing, significantly boosting its balance sheet and market confidence.

Nonetheless, analysts and investors say these investments have had minimal impact on changing the situation of Intel's struggling third-party manufacturing division. Wall Street is concerned that massive investments in this relatively new field may not yield returns. So far, the business has failed to attract significant investment from external customers.

Creative Strategies principal analyst Ben Bajarin told, overall, Intel's results Thursday were cause for "cautious optimism," but looking ahead, "all eyes move to foundry."

Recommended Articles