Intel Q3 Earnings Preview: Surge in Partnerships and Investments — Should You Bet Against a Turnaround?

TradingKey - Semiconductor chip manufacturer Intel (INTC) will report its Q3 2025 earnings after market close on Thursday, October 23, with investors watching closely to see if the company can finally prove it’s on a credible path to profitability. This quarter could mark a turning point, driven by Trump’s political backing, investments from Nvidia and SoftBank, potential new customers like AMD, breakthroughs in process technology, and ongoing cost-cutting initiatives.

According to Seeking Alpha, Wall Street analysts expect:

- Revenue: $13.14 billion, up from $12.86B in Q2, though slightly below last year’s $13.28B

- EPS: A rise to $0.01, up from -$0.10 in Q2 and a massive improvement from -$3.88 in Q3 2024

High-Risk, High-Volatility Earnings History

Per Tipranks, Intel has beaten EPS expectations in 5 of the past 8 quarters. However, only two earnings reports led to stock gains the next day — the other six triggered declines ranging from 2.90% to 26.08%, highlighting the high risk of trading around Intel’s results.

On prediction market Polymarket, odds suggest a 63% chance that Intel’s Q3 performance will exceed market expectations.

A Flood of Partnerships and Investments

Once the dominant force in global chip manufacturing, Intel has seen its market share dwindle — even falling out of the top ten — due to:

- Missing the mobile computing wave

- Failing to capitalize on the AI chip revolution

- Strategic missteps and leadership instability

- Rigid corporate culture

Now, under President Donald Trump’s “Make America Great Again” (MAGA) agenda, the U.S. government is actively backing Intel’s comeback.

In August, the U.S. government finalized an $8.9 billion equity investment in Intel. While controversial, this “national ownership” model provides credibility and may attract more commercial clients.

Additional capital inflows include:

- $2 billion from SoftBank

- $5 billion from Nvidia, including joint chip development efforts

Intel is also pursuing partnerships with Apple and TSMC, and reportedly trying to win over AMD as a foundry customer — a major opportunity for its struggling Intel Foundry business.

For context, Intel Foundry has generated $18 billion in revenue over the past four quarters but incurred at least $13 billion in losses.

Matt Bryson, Wedbush analyst, said that he believed these partnerships strengthen Intel’s balance sheet — but he remains cautious about near-term growth or lasting business impact.

Still, he added that given the current industry environment is better than expected, actual results and guidance should beat consensus.

Bryson maintains a Neutral rating, raising his price target from $19 to $20.

Reports suggest Intel will use its 18A or 18A-P process to manufacture Microsoft’s Maia 3 AI chip (codenamed Griffin) — a significant validation of its advanced node capabilities.

Technical Breakthroughs Signal a Turnaround

Earlier this month, Intel unveiled its next-generation Panther Lake AI PC processor architecture — marking its first successful deployment on the 18A process node. This is part of Intel’s ambitious “four nodes in four years” strategy, originally slated for late 2024 but delayed due to yield and optimization challenges.

Although Intel failed to gain traction in the Nvidia-dominated AI GPU market, the rapid expansion of data centers has created demand for server CPUs that work alongside GPUs — a space where Intel still holds a strong position.

Equity Armor noted that the market is giving Intel a wide pass on its past struggles. With new partnerships and product designs on the horizon, the company has significant room to rebound.

Can Long-Term Trends Be Reversed?

Intel’s core businesses face dual threats:

- AMD continues to gain share in PC and server CPUs

- Arm-based chips are challenging Intel’s long-dominant x86 architecture

Vivek Arya, BofA analyst, said that even with the Nvidia partnership, the impact appears limited. Intel continues to lose ground to AMD and Arm competitors.

He added that recent stock gains reflect improved financials and foundry potential — not proof of meaningful progress in future products.

Wedbush’s Bryson agrees, stating that recent deals boost the balance sheet and investor sentiment — but they don’t change the fundamental narrative.

HSBC analyst Frank Lee downgraded Intel this month, citing the foundry division as the biggest financial drag and repeated execution failures.

Lee warned that after Intel canceled external services on the 18A node, the feasibility of its next 14A node is now in question — especially without outside customers.

Ryuta Mkino, analyst at Gabelli Funds, cautioned that government-related share dilution could pressure Q3 EPS, while the timing of Nvidia and SoftBank deal closures may weigh on Q4 earnings.

After an 84% Rally — Is Intel Still a Buy?

As of October 22, a series of investment and partnership announcements have driven Intel’s stock up 84% year-to-date, raising concerns about whether fundamentals can justify such optimism.

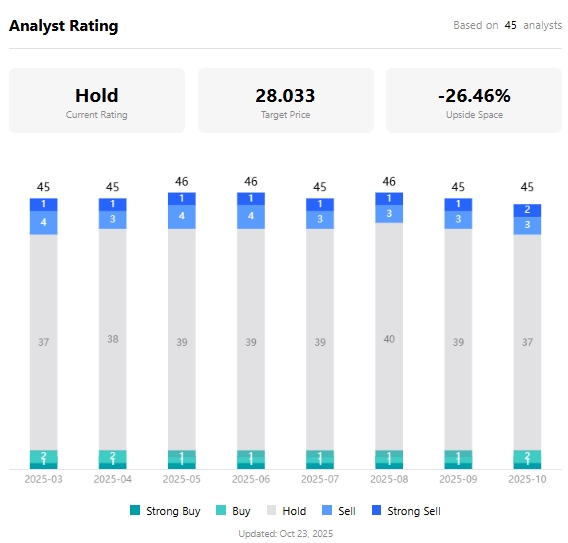

According to TradingKey, the average analyst target price is $28.03 — implying a potential downside of over 26% from current levels — highlighting a stark divergence between analyst caution and investor enthusiasm.

Of the 45 analysts covering the stock, a staggering 93.33% rate it as “Sell” or “Hold.”

Analyst Price Targets for Intel Stock, Source: TradingKey

While Morgan Stanley’s Joseph Moore is bullish with a $36 target, Rosenblatt Securities’ Kevin Cassidy sees just $14 ahead.

Recommended Articles