SoFi's Interest Rate Cut Benefit: Surging Loan Demand and Accelerated FSPL Strategy

Summary

TradingKey - I hold a cautiously optimistic rating on SoFi. Its unique business model drives strong performance. The banking license provides low-cost funding. Rapid growth in light-asset operations adds momentum. SoFi shows long-term value potential.

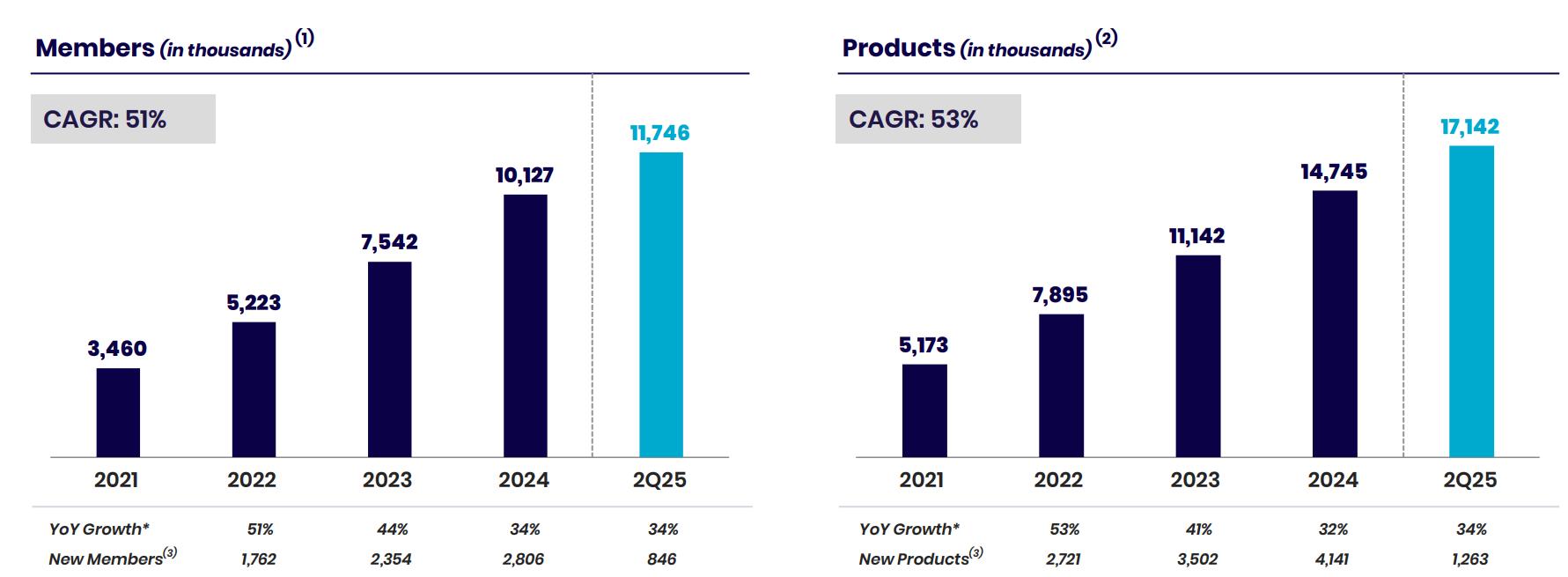

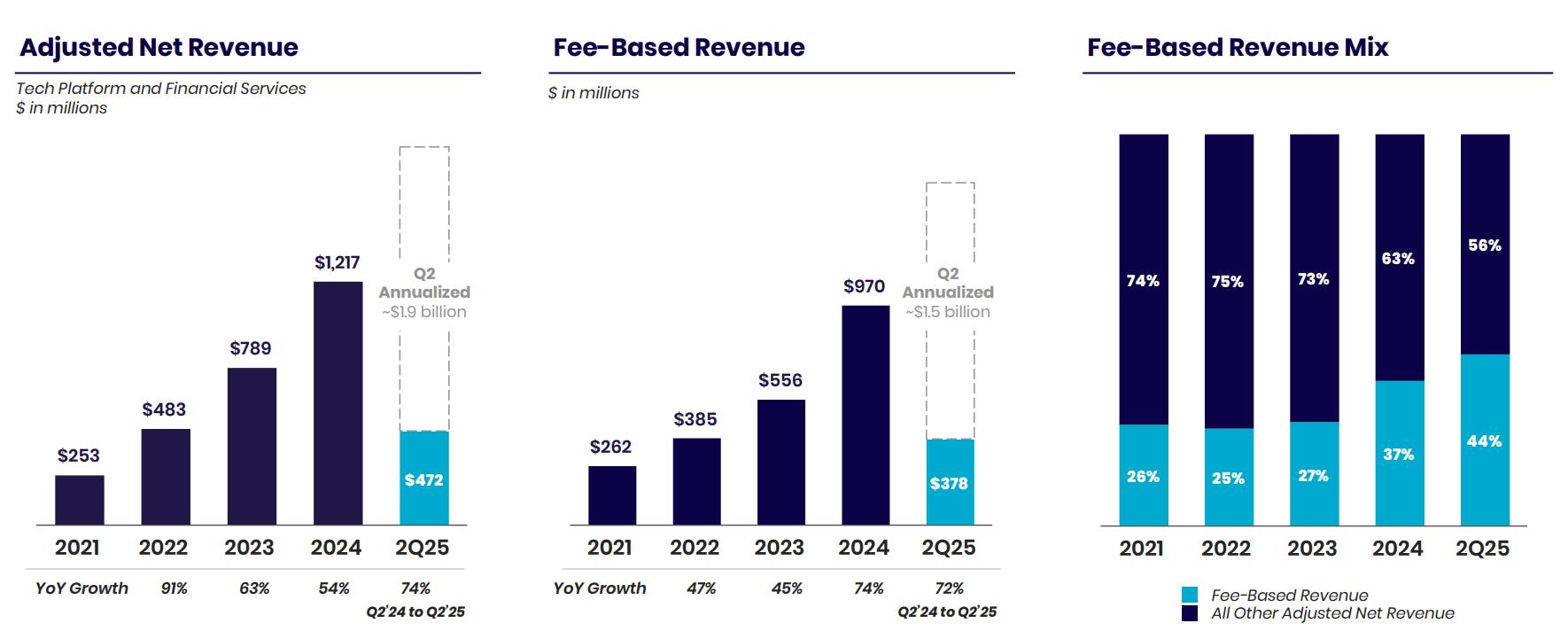

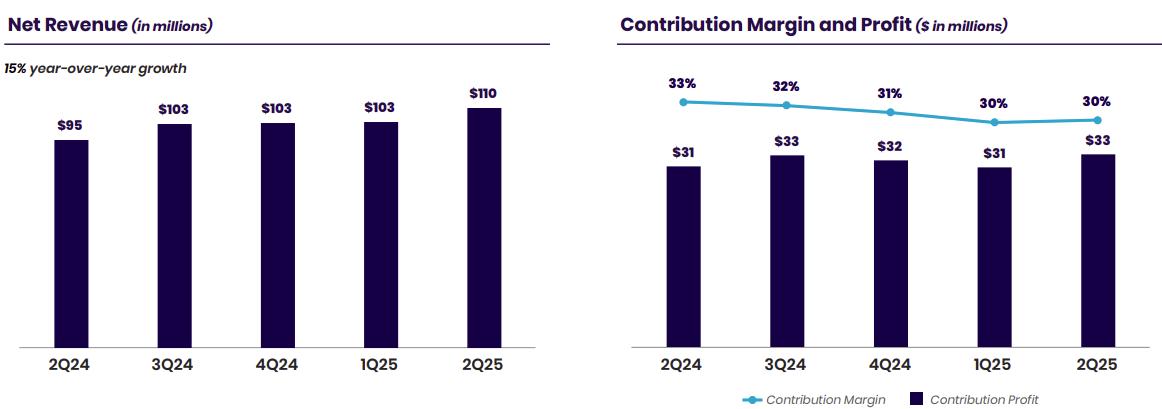

The company reported record revenue and profit in Q2 2025. It raised its full-year guidance, confirming its business model's strength. 1) Earnings Performance: Net revenue reached $858 million, up 44% year-over-year. Net profit was $97 million. The company achieved profitability for seven consecutive quarters, showing strong growth resilience. 2) User and Product: In Q2, total membership reached 11.7 million (up 34% year-over-year), and total products hit 17.1 million (up 34% year-over-year). 35% of new products came from existing members, showing strong cross-selling ability. 3) Business Structure: The light-asset segment (financial services + tech platform) generated $472 million in revenue in Q2 (up 74% year-over-year), with fee-based income at $378 million (up 72% year-over-year). With a banking license advantage, deposit balance reached $29.54 billion (average interest rate of 3.36%), saving approximately $550 million in interest annually. Net interest margin stayed at 5.86%. 4) Future Expectations: Management raised 2025 targets. Adjusted net revenue is expected to reach $3.375 billion, and net profit is projected at $370 million. SoFi plans to add at least 3 million new members (approximately 30% growth).

Source: Company Report

As of September 15, 2025, its stock price of about $27.67 have reflected high growth expectations. The valuation is significantly higher than traditional banks and most fintech peers. Investors should closely monitor macroeconomic changes, credit asset quality, and the regulatory environment. This balances high growth expectations with potential risks.

Investment Thesis

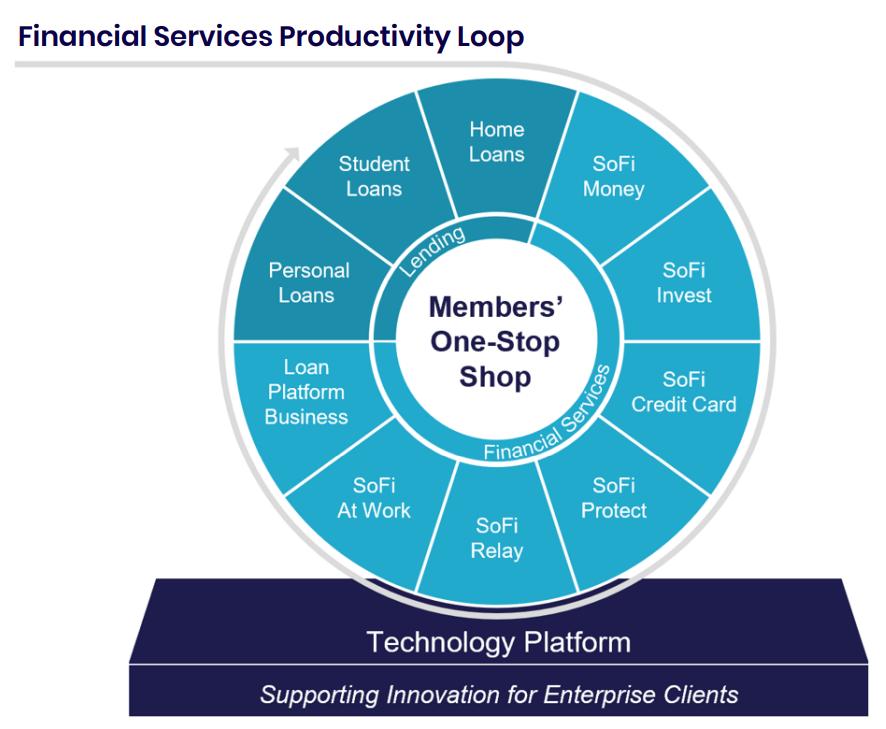

SoFi is a fintech company positioned as a "one-stop digital financial supermarket." It serves individuals and businesses through three segments: Lending, Financial Services, and Technology Platform. Based on its banking license for low-cost deposit funding and an advanced technology platform, SoFi rapidly expands in personal loans, wealth management, payments, brokerage, digital wallets, and B2B banking-as-a-service.

Its core investment logic is as follows: 1) Compounding effect of a closed-loop ecosystem: SoFi uses one product (e.g., personal loans) as an entry point to attract users into its ecosystem. Then, through high-frequency financial service products like SoFi Money, it deepens user relationships and increases per-customer value. The 34% year-over-year growth in members and products in Q2, with over one-third of new products purchased by existing users, demonstrates the success of this strategy. 2) Banking license advantage: Since obtaining a banking license in 2022, SoFi’s funding structure has fundamentally changed. Access to stable, low-cost deposits not only provides ample “ammunition” for its lending business but also significantly boosts profitability, with a net interest margin of 5.86%. 3) Growing contribution from light-asset businesses: The rapid growth of financial services and technology platforms is driving SoFi’s transformation from a capital-heavy lender to a light-asset platform company. These two segments saw combined revenue growth of 74% in Q2, with their share of total revenue steadily increasing. 4) Solid asset quality and capital position: Despite rapid expansion in lending, SoFi maintains strong credit discipline. Its personal loan 90-day delinquency rate remains low at 0.42%, and the Common Equity Tier 1 (CET1) ratio reached 14.9% by the end of 2024, indicating strong capital adequacy.

Source: Company Report

Industry Overview

According to the Digital Banking market research report by Global Industry Analysts, Inc., the global digital banking market size was about $35.3 billion in 2024. The U.S. market accounted for approximately $9.4 billion. The market is expected to grow at a compound annual growth rate of 11-15% in the coming years. As consumer digitization increases and AI technology matures, this trend continues to strengthen. The global digital lending market is projected to reach $507.27 billion in 2025. The U.S. holds a significant share, with its digital lending market expected to reach $303.07 billion in 2025 and $560.97 billion by 2030, with a compound annual growth rate of 13.10%. (Based on Mordor Intelligence data)

Competitive Landscape

SoFi faces diverse competition in the market. Digital banking competitors include pure online banks like Chime and digital sub-brands of traditional banks such as JPMorgan Chase and Goldman Sachs. In the lending sector, SoFi competes with online platforms like LendingClub, Upstart, and Rocket Loans. Large tech companies, such as Apple with Apple Pay and Apple Savings Account, are also capturing the payment and deposit market.

SoFi's Competitive Advantages

- Low-Cost Funding: SoFi's banking license is a key moat. Its deposit rates are 187 basis points lower than warehouse financing. This saves over $550 million in interest annually. It also delivers an industry-leading net interest margin of 5.86%.

- Integrated Product Ecosystem: SoFi offers loans, wealth management, investments, credit cards, and insurance. Points and rewards encourage cross-product usage, boosting ARPU. In Q2, about 35% of new products came from existing members, proving the Financial Services Productivity Loop (FSPL) strategy works.

- Technology Platform Advantage: Through Galileo and Technisys, SoFi provides payment processing and digital banking systems to other banks and fintechs. In 2025, technology platform and financial services revenue grew 74%, showing rapid platform expansion.

- Brand Awareness and Marketing Efficiency: SoFi uses targeted digital marketing and partnerships, like naming SoFi Stadium, celebrity collaborations, and media coverage. This attracts young, high-income customers effectively.

Source: Company Report

Business Model

Lending

The lending segment generates high net interest income by offering products like personal loans, student loan refinancing, and home mortgages. The core strength lies in its banking license. This allows SoFi to fund loans using stable member deposits at costs far below the market average.

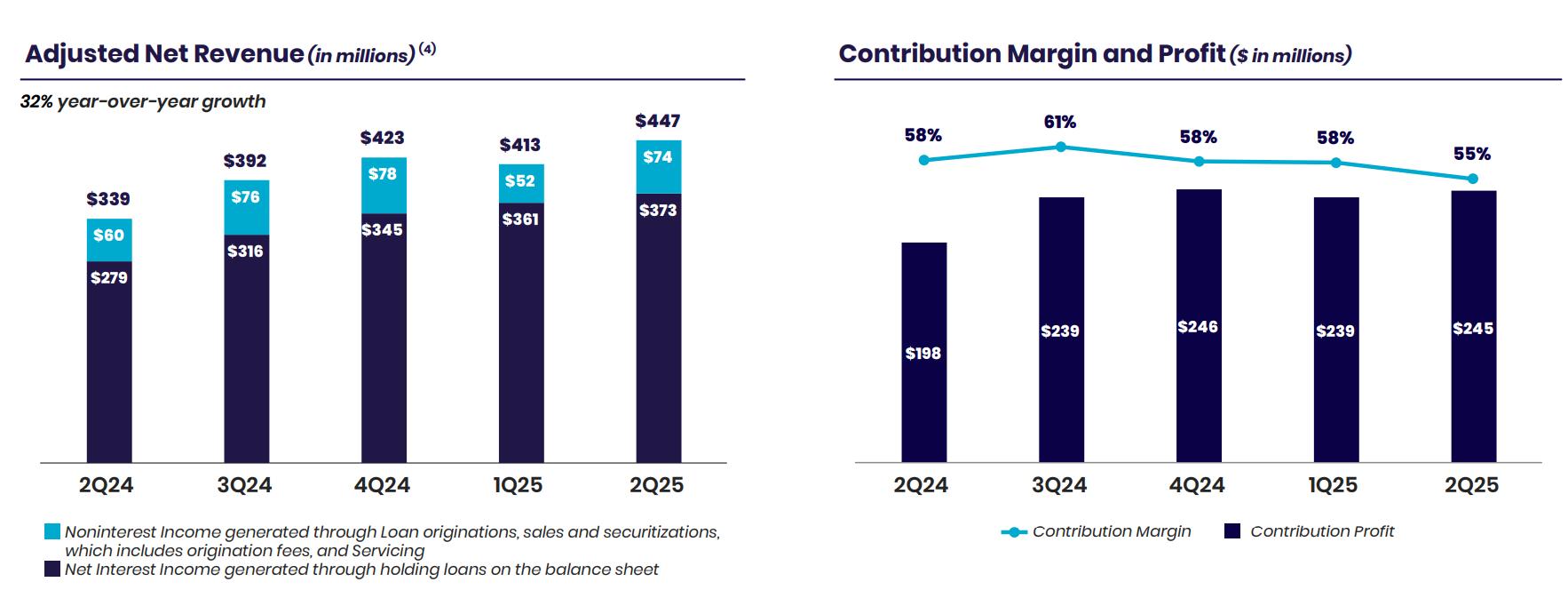

Lending remains the company’s core business. This segment still sees 32% revenue growth. However, profit margins are declining. The main reason is SoFi’s shift to the FSPL strategy. The company is moving from a single lending platform to a diversified digital financial platform. High interest rates have increased demand for student loan refinancing, especially among young, high-credit-score users—SoFi’s core demographic. As a result, SoFi’s loan portfolio is shifting toward lower-yield student loans. The company uses student loans as an entry point for the FSPL strategy, cross-selling other products like SoFi Money, SoFi Invest, and credit cards. This leads to higher customer acquisition costs, squeezing profit margins in the short term.

Source: Company Report

Financial Services

The Financial Services segment drives SoFi’s user growth and ecosystem. It offers high-frequency financial tools like SoFi Money (savings and checking accounts), SoFi Invest (investment and wealth management), and SoFi Credit Card. These attract and retain users. The business model focuses on light-asset, fee-based revenue. This includes payment interchange fees, account management fees, and brokerage commissions.

Technology Platform

This segment is SoFi’s B2B growth pillar. Through its subsidiaries, Galileo and Technisys, it provides payment processing and digital banking core systems to other banks, fintechs, and businesses. This operates on a Software-as-a-Service (SaaS) model, generating stable recurring revenue. The business is still in its expansion phase. SoFi continues to invest in technology development, maintenance, customer acquisition, and product innovation. These costs are currently high, leading to lower profit margins. However, this is a necessary step for SoFi’s transformation from a lending platform to a comprehensive fintech giant.

Source: Company Report

Financial and Valuation Analysis

Financial Analysis

SoFi remained unprofitable in 2023. In 2024, it turned profitable with a net income of $499 million. Adjusted net income, excluding one-time deferred tax benefits, was $227 million. For 2025, the company expects a net income of about $370 million. Revenue continues to grow rapidly: 2024 revenue increased by 26%, with an expected 30% growth in 2025. Sustained growth in members and products drives business expansion. Q2 deposits reached $29.54 billion, up 35% from the end of 2024, supporting lending capacity. Q2 personal loan originations were $8.8 billion, up 66% year-over-year. Student loans and home loans grew by 35% and 92%, respectively. Additionally, the company launched innovative products like home equity loans and flexible student loans, further diversifying revenue streams.

The market expects the Federal Reserve to cut interest rates 2–3 times in 2025, likely boosting loan demand and SoFi’s related revenue in the short term. With a significant portion of personal loans, SoFi may benefit quickly from declining short-term yields, improving net interest margin and interest income. Due to rising fee-based income and deposit cost advantages, net interest margin is expected to remain above 5% in the coming years.

Source: SoFi, TradingKey

Valuation Analysis

As of the closing price of $27.67 on September 15, 2025, SoFi’s dynamic P/E ratio is about 89, based on management’s expected earnings per share of approximately $0.31. The P/S ratio, calculated with $3.375 billion in revenue and 1.183 billion diluted shares, is around 9.7. Compared to traditional banks (P/E typically 10-12) and established fintech companies (P/S 3-5), SoFi’s valuation is significantly high. The market is pricing in its strong growth and long-term potential. If SoFi maintains around 30% revenue growth in the coming years, improves EBITDA margin to above 29%, and continues expanding its light-asset business, its long-term investment value remains strong. However, if the macro environment worsens or competition intensifies, slowing growth, the valuation could be corrected.

Risk

- Macroeconomic Risk: SoFi’s lending business is sensitive to employment and consumer credit demand. High interest rates may reduce borrowing demand and increase default rates. A recession or sudden rate hike could significantly pressure profitability.

- Credit Risk: Although the personal loan delinquency rate has dropped to 0.42%, deteriorating customer credit quality or overly rapid balance sheet expansion could raise bad debt rates, eroding profits.

- Regulatory Risk: As a bank holding company and broker-dealer, SoFi faces complex regulatory requirements. Policy changes, such as interest rate controls, bank capital rules, or fintech regulations, could impact its business model and capital usage.

- Competition and Technology Risk: The market is highly competitive, with traditional banks accelerating digital transformation and large tech firms entering payments and deposit services. The technology platform requires ongoing investment to stay ahead. Technological lag or system security issues could harm the company’s reputation and lead to customer loss.

- High Valuation Risk: The market’s high growth expectations for SoFi are reflected in elevated price-to-earnings and price-to-sales ratios. If growth or profit improvements fall short of expectations, the stock price could fluctuate significantly.

Conclusion

SoFi has grown from a single loan company into a fintech platform integrating lending, payments, investing, and core banking technology. It leverages its banking license for low-cost funding. The FSPL strategy enhances customer stickiness. Its tech platform expands light-asset revenue. This showcases a unique business model and long-term potential. SoFi achieved profitability in 2024. Q2 2025 revenue and profits hit new highs. Management raised full-year guidance, indicating further growth potential. However, its valuation is high compared to peers. All in all, SoFi’s got a unique business model with serious long-term potential. If investors are thinking about investing, a cautiously optimistic approach makes sense, but should monitor macroeconomic conditions, credit quality, and regulatory risks.

Get Started

Recommended Articles