September Global Central Bank Divergence: How Will U.S. Stocks and Forex Markets Move?

TradingKey - Despite the divergence in monetary policies among major global central banks in September (with the Federal Reserve cutting rates while the European Central Bank, Bank of England, and Bank of Japan maintain steady rates), we expect the policy directions of the Fed, ECB, and BoE to converge by year-end, with all three continuing to pursue rate cuts. Influenced by a more accommodative monetary policy environment, U.S. stocks are likely to sustain their upward trend. Given the policy convergence, significant changes in policy rate differentials among these three economies are unlikely, suggesting that the EUR/USD and GBP/USD exchange rates will likely remain range-bound. In contrast, Japan’s economic growth is rebounding, and with the BoJ’s monetary policy diverging from the others, the yen is expected to strengthen in the short term.

Source: Mitrade

Main Body

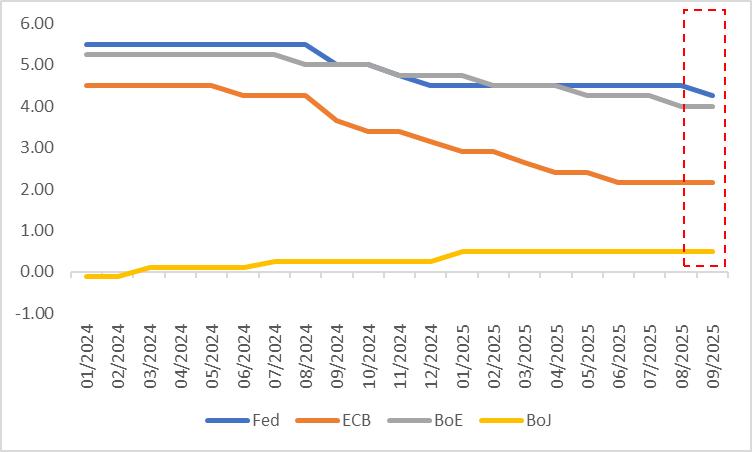

The market widely anticipates that the Federal Reserve (Fed) will cut interest rates by 25 basis points on 17 September 2025, lowering the benchmark rate to 4.25%. On 18 September, the Bank of England (BoE) and the Bank of Japan (BoJ) are expected to keep their rates unchanged at 4% and 0.5%, respectively. Meanwhile, on 11 September, the European Central Bank (ECB) decided to maintain its rate at 2.15%, aligning with market expectations (Figure 1). This indicates a degree of divergence in monetary policies among major global central banks in September (Figure 2). Looking ahead, how will central bank interest rates change starting next month, and what impact will this have on U.S. stocks and forex markets?

Figure 1: Market Consensus Forecasts or Actual Data

Source: Refinitiv, TradingKey

Figure 2: Major Global Central Bank Policy Rates (%)

Source: Refinitiv, TradingKey

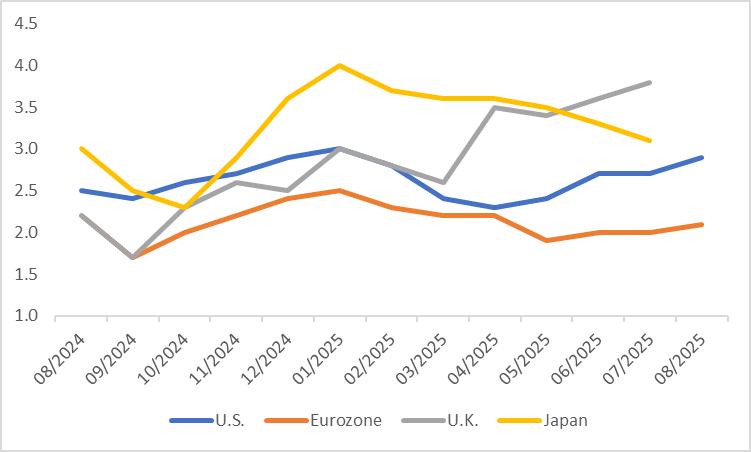

In the U.S., August non-farm payrolls rose by only 22,000, significantly below market expectations, while June’s non-farm data was revised to a negative figure. Despite clear signs of reflation, both CPI and PCE inflation remain within manageable levels. Under these conditions, the Fed is likely to focus more on the weakening labour market. In addition to an expected 25-basis-point rate cut on 17 September, the Fed may implement two further rate cuts within the year.

In the Eurozone, the CPI has remained close to the ECB's target level, with low risks of reflation expected in the short term. Coupled with a pessimistic economic outlook for the region, following the ECB's decision to keep interest rates unchanged on 11 September, the central bank is anticipated to continue pursuing rate cuts. By the first half of 2026, the Eurozone is expected to enter a period of low interest rates.

In the U.K., economic growth stagnated in July. Over both the past three and six months, average growth has remained at a mere 0.1%, indicating a sluggish economy. Additionally, since September of last year, both headline and core CPI have consistently risen. The combination of low growth and high inflation suggests that the UK is gradually entering a phase of stagflation. Following the BoE's expected pause on rate cuts on 18 September, we anticipate the central bank will adopt a gradual approach to lowering interest rates to ease downward economic pressure, though significant rate reductions are unlikely.

In Japan, real GDP grew by 0.5% quarter-on-quarter in the second quarter of this year, surpassing market expectations of 0.3% and the first quarter’s flat growth of 0%. While inflation has gradually eased from its peak, the CPI is expected to remain significantly above the BoJ’s 2% target in the short term. Despite recent instability caused by the prime minister’s resignation, Japan’s economy continues to show strong recovery momentum. With inflation persistently elevated, consequently, we expect the BoJ to maintain current interest rates on 18 September but shift to a hawkish stance, resuming rate hikes in October.

Figure 3: Major Developed Economy CPI (%, y-o-y)

Source: Refinitiv, TradingKey

All in all, despite the divergence in monetary policies among major global central banks in September (with the Federal Reserve cutting rates while the European Central Bank, Bank of England, and Bank of Japan maintain steady rates), we expect the policy directions of the Fed, ECB, and BoE to converge by year-end, with all three continuing to pursue rate cuts. Influenced by a more accommodative monetary policy environment, U.S. stocks are likely to sustain their upward trend. Given the policy convergence, significant changes in policy rate differentials among these three economies are unlikely, suggesting that the EUR/USD and GBP/USD exchange rates will likely remain range-bound. In contrast, Japan’s economic growth is rebounding, and with the BoJ’s monetary policy diverging from the others, the yen is expected to strengthen in the short term.

Get Started

Recommended Articles